The Painful Pivot from Global Sprawl to Corporate Focus

Citigroup's strategic retreat from its sprawling global consumer franchise marks a pivotal, albeit costly, chapter. The stated goal is to transform into a leaner, more profitable institution centered on its crown jewel, the Treasury and Trade Solutions (TTS) business. This shift is reflected in its recent financial performance.

Navigating the Choppy Waters of Restructuring

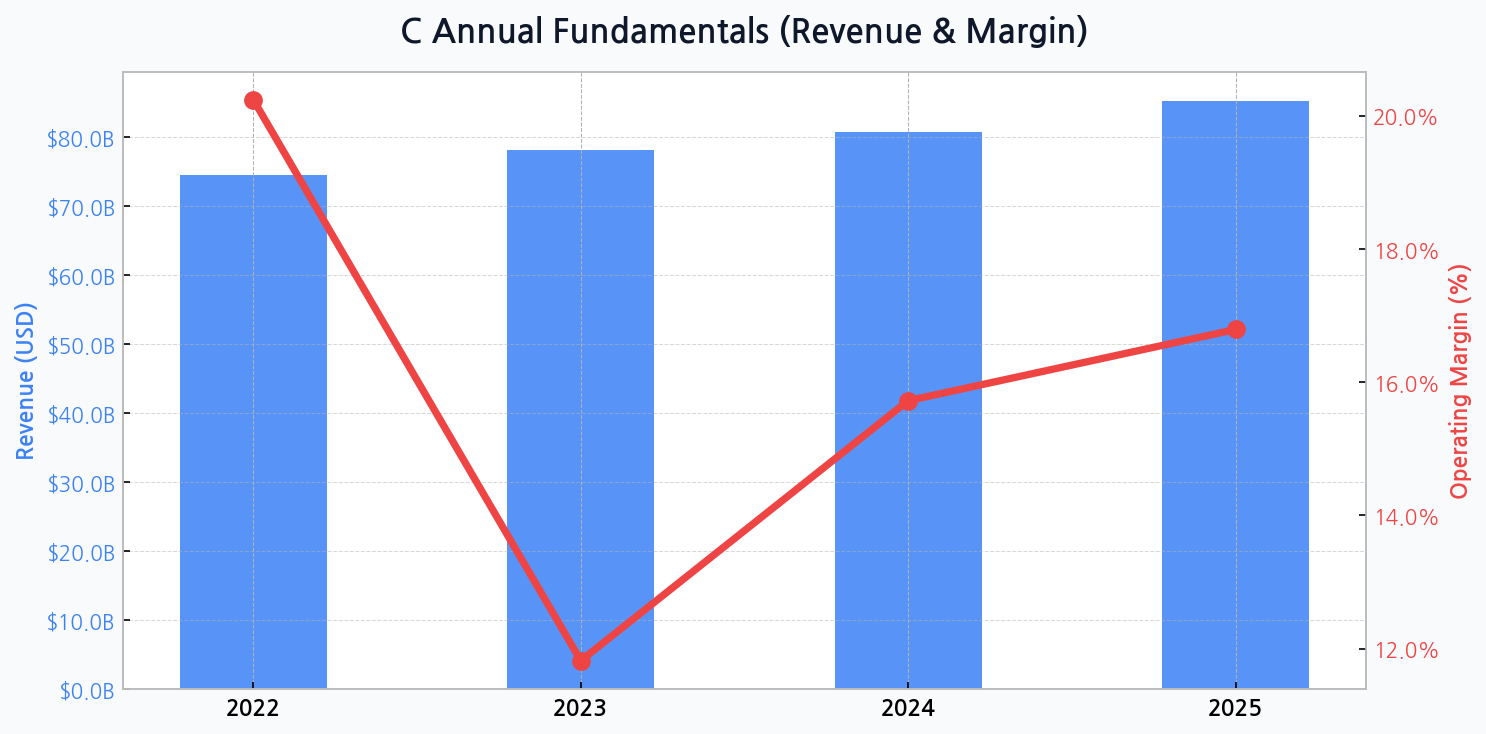

The financial narrative shows a company in transition. While revenue grew from $74.5B in 2022 and is projected to reach $85.2B by 2025, the journey has been turbulent. The operating margin saw a dramatic plunge from 20.2% in 2022 to just 11.8% in 2023, a direct consequence of hefty restructuring charges and divestiture costs. The recovery to a forecasted 16.8% by 2025 signals optimism but underscores the operational hurdles ahead.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for C

[Chart] Citigroup's revenue shows a consistent upward trend, while operating margin experiences a significant dip in 2023 before projecting a gradual recovery, illustrating the short-term costs of its long-term strategic pivot.

Deconstructing the Revenue Engine

To understand the 'why' behind this strategic overhaul, one must look at the composition of its revenue streams. The institutional businesses, particularly TTS, consistently deliver higher returns on capital compared to the more capital-intensive and fragmented consumer markets the bank is now exiting.

| Business Segment | Est. Revenue Share | Margin Profile | Strategic Importance |

|---|---|---|---|

| Institutional Clients Group (ICG) | ~ 60% | High | Core Growth Engine |

| Personal Banking & Wealth | ~ 35% | Moderate | Refocusing on U.S. |

| Legacy Franchises | ~ 5% | Low / Negative | Divestment Priority |

DIFF Insight: This breakdown reveals the strategic imperative behind the divestitures. The Legacy Franchises, while once symbols of global reach, have become a drag on profitability. By reallocating capital to the ICG, particularly the high-margin TTS and securities services, Citigroup is making a concentrated bet on its most potent institutional-focused powerhouse.

A Fortress Balance Sheet or a Leveraged Bet?

A core promise of this simplification was a healthier balance sheet. However, the data presents a more complex picture. While total assets are projected to fluctuate, the debt ratio remains stubbornly high, moving from 91.6% in 2022 to a projected 92.0% in 2025. This indicates that balance sheet simplification is not yet a reality and that the firm remains highly leveraged, posing risks in a volatile interest rate environment.

The market is rewarding clarity. Citi's sprawling, unfocused model was a relic of a bygone era. The question isn't whether the strategy is correct, but whether management can execute it without further value destruction.

The Valuation Question: A Turnaround Story in the Making?

Citigroup has long traded at a discount to its peers, a reflection of its lower returns and complex structure. The current strategy is a direct attempt to close this valuation gap. A successful execution could lead to a significant re-rating as the market begins to price it more like a focused corporate bank rather than a struggling universal one.

| Metric | Citigroup (C) | JPMorgan Chase (JPM) | Bank of America (BAC) |

|---|---|---|---|

| Price / Book (P/B) | ~ 0.6x | ~ 1.8x | ~ 1.1x |

| Forward P/E | ~ 9x | ~ 12x | ~ 12x |

| Return on Equity (ROE) | ~ 8% | ~ 17% | ~ 11% |

DIFF Insight: The stark valuation discount, particularly in the Price-to-Book ratio, highlights the market's skepticism. Peers with higher and more stable Returns on Equity command significant premiums. Closing this gap is the ultimate benchmark for the success of Citigroup's strategy, but it requires years of consistent performance, not just a compelling narrative.

The Bull Case for a Streamlined Citi

Investors optimistic about the bank's future are betting on a few key outcomes:

- Margin Expansion: A greater revenue mix from high-return businesses like TTS should naturally lift overall profitability.

- Capital Efficiency: Exiting capital-intensive consumer businesses frees up capital for higher-return investments and shareholder returns (buybacks, dividends).

- Reduced Complexity: A simpler business model should lower operating costs and reduce the risk of regulatory penalties.

- Strategic Clarity: A focused mission allows for better resource allocation and a clearer story for investors to buy into.

The Gauntlet of Risks Ahead

The path forward is not without peril. The primary concern is execution risk; divesting assets across numerous jurisdictions is complex and can lead to unforeseen writedowns. Furthermore, a concentrated bet on institutional clients makes the bank more sensitive to global economic cycles and capital market volatility.

| Risk Factor | Probability | Potential Impact |

|---|---|---|

| Macroeconomic Downturn | Medium | High |

| Divestiture Complications | Medium | Medium |

| Regulatory Scrutiny | High | Medium |

| Competitive Pressure | High | High |

DIFF Insight: While macroeconomic risks affect all banks, the 'Divestiture Complications' are unique to Citigroup's current situation. A botched exit from a key market could not only impact the bottom line but also damage management's credibility, undoing much of the goodwill generated by the strategic pivot. The high competitive pressure from more stable rivals like JPM remains a constant threat.