The Unbreachable Moat of Brand Loyalty

Marriott's primary competitive advantage is not its physical properties but its intangible ecosystem. The Bonvoy loyalty program acts as a powerful moat, capturing travelers and creating a high barrier to entry for competitors. This network effect fuels consistent fee generation from its vast portfolio of franchised and managed hotels.

Gauging the Competitive Landscape

| Metric | Marriott (MAR) | Hilton (HLT) | Hyatt (H) |

|---|---|---|---|

| Loyalty Members | ~ 200 Million+ | ~ 180 Million+ | ~ 40 Million+ |

| Property Count | ~ 8,700+ | ~ 7,400+ | ~ 1,300+ |

| Market Cap (Approx) | $94B | $65B | $16B |

DIFF Insight: While Marriott leads in scale, the sheer size of its loyalty program is the true differentiator. This massive user base provides invaluable data for personalized marketing and ensures a steady stream of high-margin, direct bookings, insulating it partially from the commission fees of online travel agencies (OTAs).

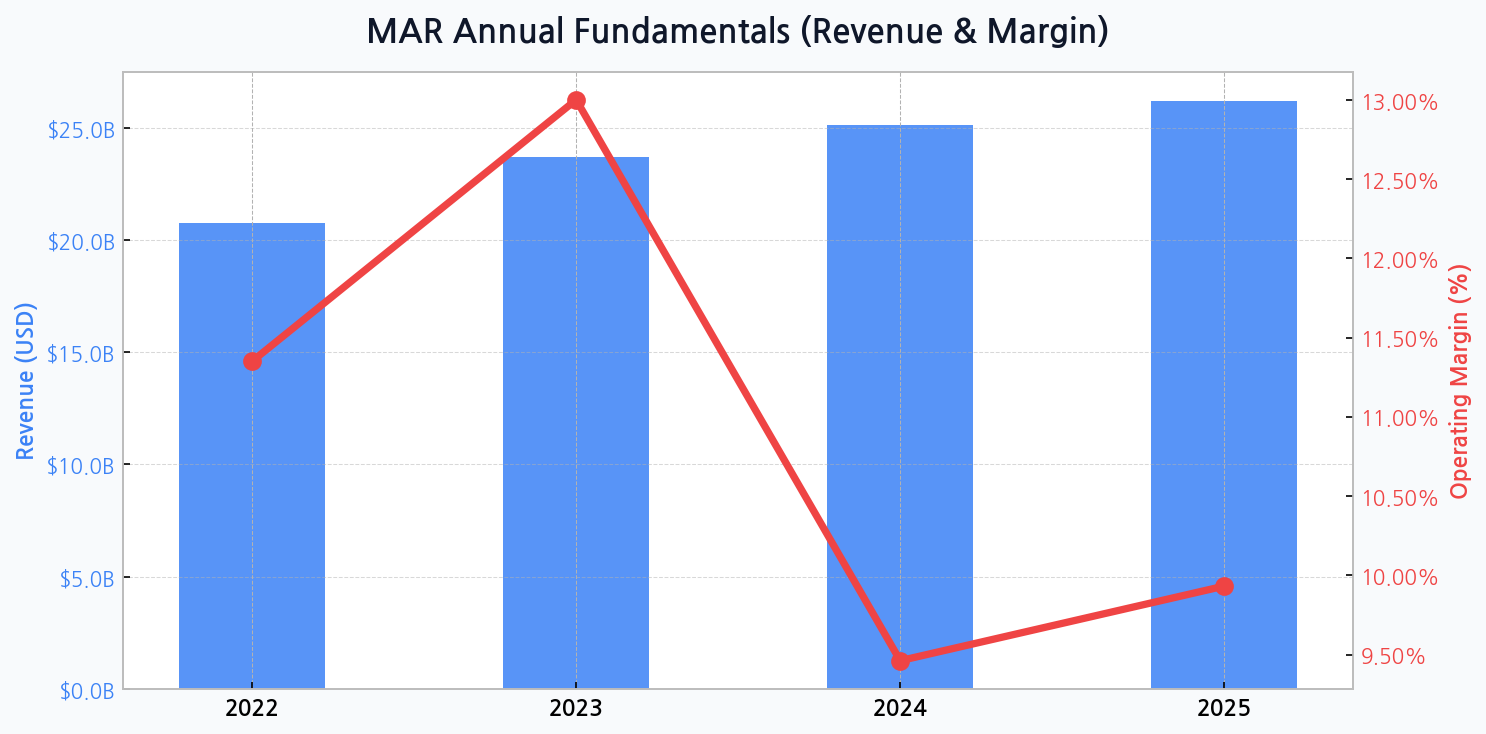

The Asset-Light Paradox: Growth vs. Profitability

The company's asset-light business model is designed for high-margin, scalable growth. Revenue figures support this, with a steady climb from $20.8B in 2022 to a projected $26.2B by 2025. Yet, this growth story is complicated by margin volatility. After peaking at 13.0% in 2023, the operating margin is expected to contract sharply to 9.5% in 2024 before a modest recovery.

"Growth for growth's sake is the ideology of the cancer cell. For Marriott, the 2024 margin compression signals that top-line expansion is coming at a significant cost, forcing investors to question the efficiency of its current capital allocation strategy."

The Specter of Rising Leverage

Beneath the surface of revenue growth lies a concerning trend in financial health. While total assets are forecast to grow from $24.8B in 2022 to $27.5B in 2025, debt is growing faster. This is reflected in an escalating debt-to-asset ratio, which is projected to climb from an already high 97.7% in 2022 to a precarious 113.7% by 2025, indicating that liabilities will exceed assets.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for MAR

[Chart] Marriott's revenue shows a consistent upward trend from 2022 to 2025, while its operating margin peaks in 2023 before experiencing a significant decline in 2024 and a slight recovery in 2025.

A Critical Look at Emerging Threats

| Threat Category | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Macroeconomic Downturn | Medium | High | Focus on budget-friendly brands |

| OTA Disruption | Medium | Medium | Enhance Bonvoy member perks |

| Debt Overhang | High | High | Aggressive deleveraging, asset sales |

| Geopolitical Instability | Low | High | Geographic diversification |

DIFF Insight: The most immediate and controllable threat is the internal 'Debt Overhang.' While external factors like a recession are significant, the company's own balance sheet management is the critical variable. Failure to address this could lead to credit rating downgrades and increased borrowing costs, strangling future growth.

Strategic Imperatives for Sustained Dominance

- Deleveraging the Balance Sheet: Prioritize debt reduction to restore financial flexibility and investor confidence before pursuing further large-scale expansion.

- Margin Fortification: Implement rigorous cost-control measures and leverage technology to offset the operational cost pressures that are causing margin erosion.

- Deepening the Moat: Continue to invest heavily in the Bonvoy ecosystem, transforming it from a simple rewards program into an indispensable travel platform.

Valuation Under the Microscope

| Company | Forward P/E Ratio | EV/EBITDA | Commentary |

|---|---|---|---|

| Marriott (MAR) | ~ 24x | ~ 17x | Premium valuation reflects brand strength |

| Hilton (HLT) | ~ 25x | ~ 18x | Slightly higher premium, strong execution |

| Hyatt (H) | ~ 22x | ~ 16x | Lower multiple due to smaller scale |

DIFF Insight: Marriott trades at a premium multiple, which is justified by its scale and powerful loyalty program. However, this valuation leaves little room for error. Any failure to manage the looming debt crisis or stabilize margins could trigger a significant market correction for its stock.