The Post-Pandemic Reality Check Has Arrived

Pfizer is navigating a profound strategic reset. The windfall from its COVID-19 franchise has evaporated, forcing a return to the fundamentals of pharmaceutical growth: pipeline development and strategic acquisition. The transition is proving to be a turbulent one for the healthcare giant.

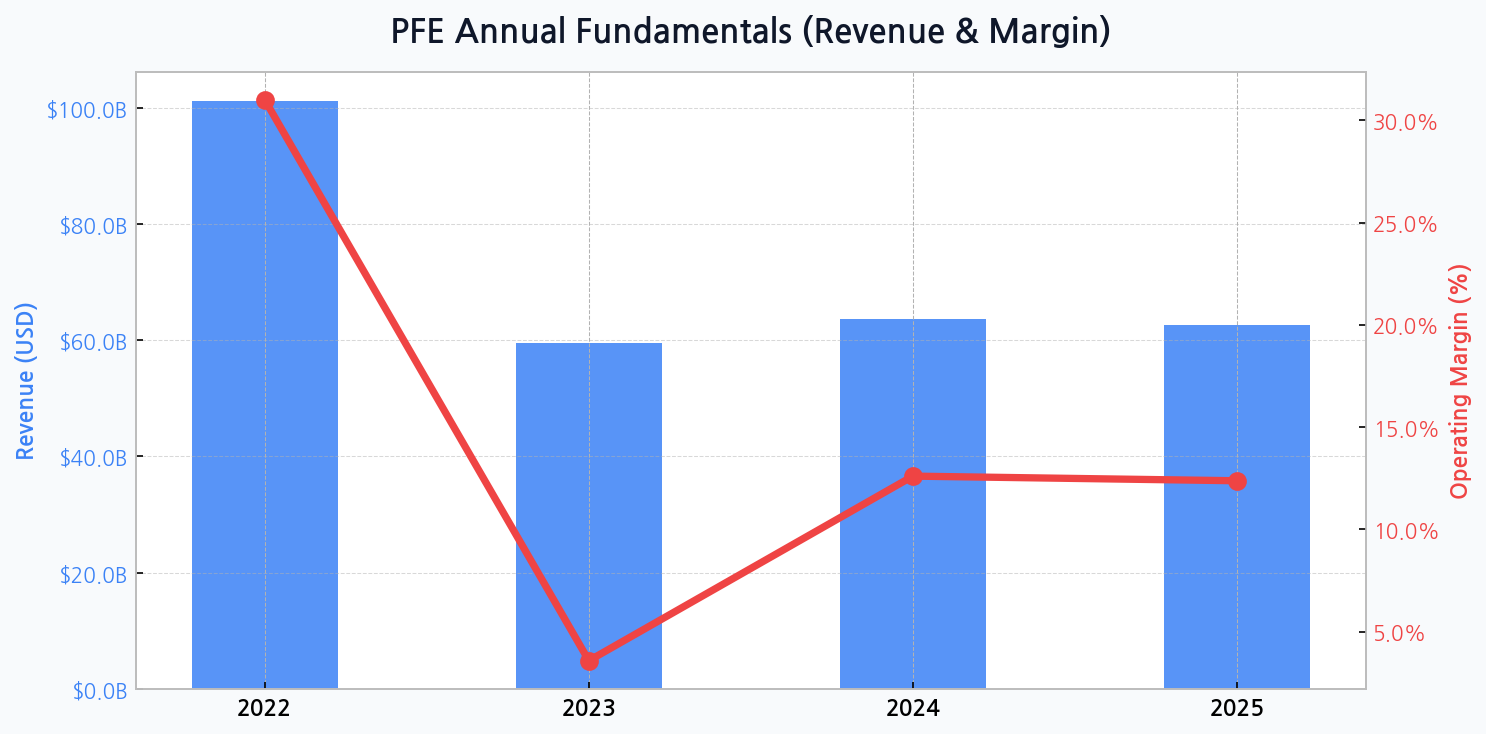

Deconstructing the Unprecedented Revenue Cliff

The scale of the revenue normalization is stark. After reaching a monumental peak of $101.2 billion in 2022, revenue fell sharply to a projected $59.6 billion in 2023. This isn't a cyclical downturn but a structural shift away from pandemic-level demand, establishing a new, more modest baseline for the company's top-line performance.

Margin Compression and the Search for a New Equilibrium

This revenue shock directly impacted profitability. Operating margin plummeted from a robust 31.0% in 2022 to a mere 3.6% in 2023, reflecting lower-margin products and restructuring costs. While forecasts show a recovery to around 12.5%, this new level is far from the pandemic-era highs, signaling a permanent change in its earnings profile.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for PFE

[Chart] Pfizer's annual revenue and operating margin from 2022 to 2025, illustrating the sharp decline from pandemic peaks and a subsequent stabilization at lower levels.

The Strategic Pivot: Growth Through Acquisition

In response, management has executed a strategic M&A pivot, most notably with the acquisition of Seagen. This move is designed to build a new growth engine in oncology. However, this strategy has come at a cost, significantly altering the company's financial health and risk profile.

The market is no longer valuing Pfizer on its past glories but on its ability to execute one of the largest post-merger integrations in recent pharma history. The debt taken on is a necessary gamble to avoid a decade of stagnation.

A Balance Sheet Under New Pressure

The aggressive acquisition strategy is clearly visible on the balance sheet. Total assets swelled in 2023, but so did liabilities. The company's debt ratio jumped from a manageable 51.4% in 2022 to a more concerning 60.6% in 2023, before stabilizing around 58%. This increased leverage restricts financial flexibility and magnifies risks if new products underperform.

| Year | Dividend per Share (Annual) | Earnings Payout Ratio | Share Buybacks |

|---|---|---|---|

| 2022 | $1.60 | ~ 26% | $2.0B |

| 2023 (Est.) | $1.64 | >100% | Suspended |

| 2024 (Proj.) | $1.68 | ~ 75% | Minimal |

DIFF Insight: The payout ratio spiking above 100% in 2023 is a major red flag, indicating the dividend was paid from sources other than current earnings, such as cash reserves or debt. The suspension of buybacks further underscores the capital constraints Pfizer faces. The projected 75% ratio in 2024, while an improvement, remains high and leaves little room for error or reinvestment.

The Looming Dividend Sustainability Test

For income-focused investors, the dividend is paramount. While management has reaffirmed its commitment, the financial cushion has thinned considerably. The company's ability to cover and grow its dividend now depends entirely on generating substantial cash flow from its newly acquired assets and existing non-COVID portfolio, making this the ultimate dividend sustainability test.

- Revenue Concentration: Over-reliance on a few blockbuster drugs remains a key risk.

- Integration Risk: Failure to smoothly integrate Seagen could destroy shareholder value.

- Patent Cliffs: Key drugs like Eliquis and Ibrance face loss of exclusivity later this decade.

- Debt Burden: High leverage could limit future strategic options and R&D spending.

| Metric | Pfizer (PFE) Forward | Peer Average (MRK, JNJ) | Sector Median |

|---|---|---|---|

| P/E Ratio | ~ 12.5x | ~ 15.0x | ~ 17.0x |

| Price/Sales | ~ 2.6x | ~ 3.8x | ~ 4.2x |

| Dividend Yield | ~ 5.8% | ~ 3.1% | ~ 2.5% |

DIFF Insight: Pfizer trades at a significant discount to its peers on both P/E and P/S multiples, reflecting market skepticism about its growth prospects and integration risks. The high dividend yield is a direct result of the depressed stock price and serves as compensation for the elevated uncertainty investors must accept.

Navigating a Future Beyond the Pandemic Windfall

The path forward is clear but challenging. Success is no longer guaranteed by a single, dominant product line. It will be defined by disciplined execution, successful R&D in high-growth areas like oncology, and careful management of a heavily leveraged balance sheet. The market is watching to see if this old giant can create a new, sustainable growth story from the ashes of its pandemic-era success, especially in a world of eroding pricing power.