The Unstoppable Revenue Engine Confronts a Profitability Crisis

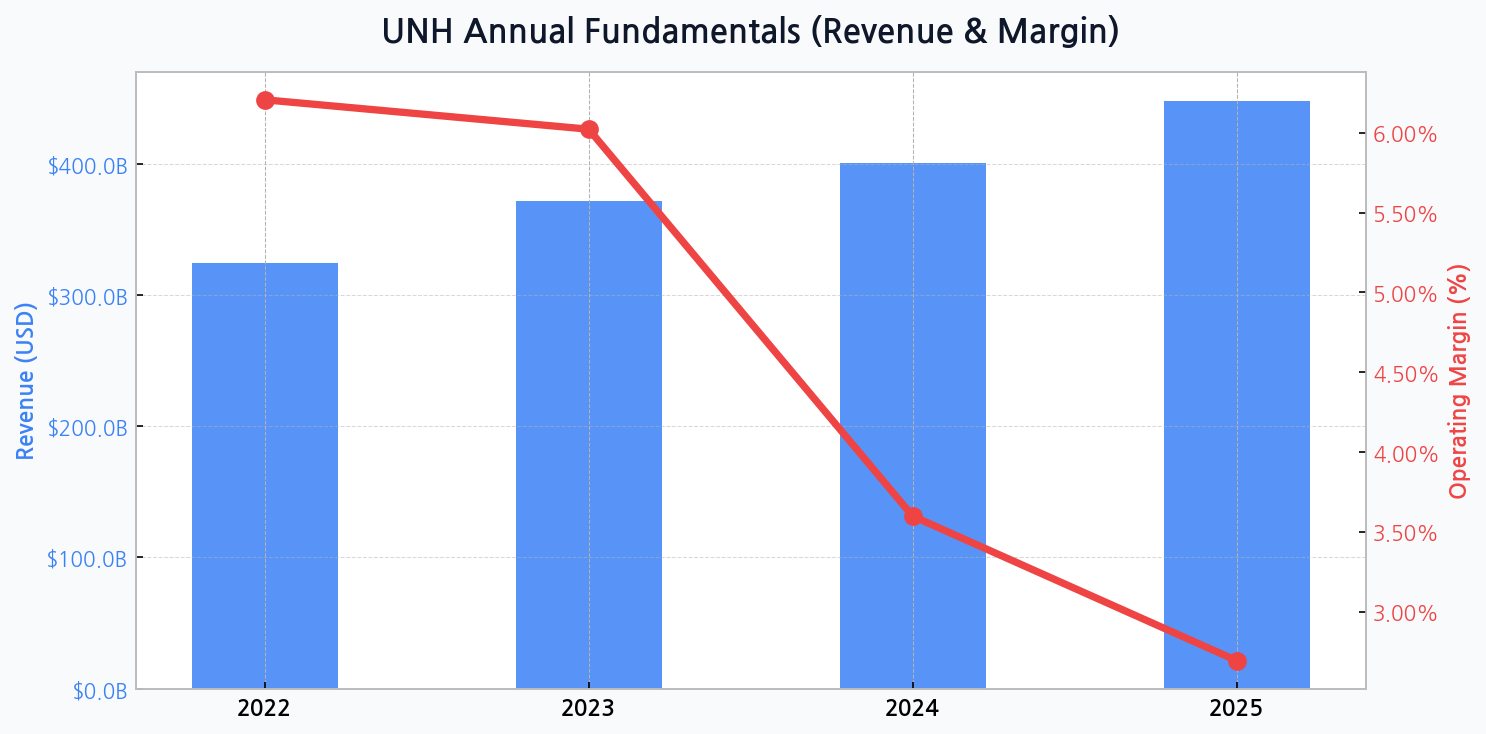

UnitedHealth Group presents a fascinating paradox. The company's revenue growth is nothing short of formidable, projected to surge from $324.2 billion in 2022 to an estimated $447.6 billion by 2025. This expansion underscores its dominant market position and successful scaling.

However, this top-line success masks a troubling trend. The operating margin is on a sharp downward slide, contracting from a healthy 6.2% in 2022 to a forecasted 2.7% by 2025. This compression signals significant headwinds that challenge the sustainability of its current business model.

Dissecting the Core Pressure Points on Profitability

The primary driver behind this margin erosion appears to be escalating medical cost trends, where utilization rates are rising faster than premium adjustments. This issue is compounded by the costs associated with integrating numerous acquisitions and navigating an increasingly complex healthcare landscape.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for UNH

A Fortress Balance Sheet Under Increasing Leverage

While total assets are expanding robustly, from $245.7 billion to a projected $309.6 billion over the same period, the company's financial health requires scrutiny. The debt ratio is simultaneously creeping upwards, from 64.9% in 2022 to an anticipated 67.1% in 2025, indicating a greater reliance on leverage to fuel growth.

Ecosystem Dominance: An Unassailable Moat?

UNH's primary strategic advantage lies in its powerful, vertically integrated structure. The synergy between its insurance arm (UnitedHealthcare) and its health services segment (Optum) creates a formidable competitive barrier. This allows for data-driven insights and cost controls that smaller rivals cannot match.

The true power of UNH lies not in its scale alone, but in its data flywheel. Optum's analytics inform UnitedHealthcare's underwriting, while the insurance arm provides a vast patient network for Optum's services. This creates a self-reinforcing ecosystem that suffocates competition.

| Company | Market Share (Medical) | Key Strength | Primary Weakness |

|---|---|---|---|

| UnitedHealth (UNH) | ~ 15% | Integrated Model (Optum) | Regulatory Scrutiny |

| Elevance Health (ELV) | ~ 11% | Strong Blue Cross Brand | Less Diversified |

| CVS Health (CVS) | ~ 9% | Retail + Pharmacy + PBM | Integration Complexity |

DIFF Insight: The table highlights that while UNH holds a leading market share, its true moat is structural. Competitors like CVS are attempting to replicate this integrated model, but UNH's decade-long head start with Optum provides a significant data and operational advantage. The key threat is not from a direct competitor matching its model, but from regulators seeking to dismantle it.

Optum Remains the Undisputed Crown Jewel

The Optum segment is the engine of diversification and future growth. Its suite of services, from pharmacy benefit management (PBM) to data analytics and direct patient care, offers higher-margin revenue streams that are crucial for offsetting the pressures within the traditional insurance business.

| Segment | Revenue Contribution | Growth Driver |

|---|---|---|

| UnitedHealthcare | ~ 65% | Membership Growth |

| Optum Health | ~ 15% | Value-Based Care |

| Optum Insight | ~ 5% | Data & Analytics |

| Optum Rx | ~ 15% | PBM Scale |

DIFF Insight: While UnitedHealthcare still constitutes the bulk of revenue, the strategic importance of the three Optum sub-segments cannot be overstated. Optum Health's expansion into direct care delivery is a direct attempt to control the medical cost curve, which is the primary source of margin pressure. The success of this vertical integration will determine UNH's long-term profitability.

Navigating the Treacherous Regulatory Gauntlet

With great market power comes great regulatory scrutiny. UNH faces persistent threats from potential policy changes related to medical loss ratios, PBM practices, and antitrust concerns over its acquisitions. A single adverse ruling could have a material impact on its operations and profitability.

| Risk Factor | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Adverse Policy Change | Medium | High | Lobbying & Diversification |

| Antitrust Action | Medium | High | Focus on Organic Growth |

| Medical Cost Inflation | High | High | Optum Health Expansion |

| Cybersecurity Breach | Low | Medium | Technology Investment |

DIFF Insight: The matrix clearly shows that regulatory and cost-related risks pose the most significant threats to UNH. The company's strategy is inherently defensive, using its scale and diversified Optum assets to mitigate these external pressures. Investors must watch for shifts in the political climate, as this remains the biggest 'black swan' risk for the company.

The Strategic Crossroads Ahead

UnitedHealth Group's future hinges on its ability to navigate a delicate balancing act. It must continue its growth trajectory while fundamentally addressing the margin compression that threatens its financial narrative. The performance of its integrated care delivery model will be the ultimate test.

- Margin Stabilization: The top priority must be to control medical costs through the expansion of value-based care via Optum.

- Capital Allocation: Management must justify its rising debt levels with clear ROI from acquisitions and strategic investments.

- Regulatory Defense: Proactively demonstrating the consumer benefits of its integrated model is crucial to fending off political headwinds.