A Legacy Navigating a Turbulent Air Pocket

The Boeing Company is confronting one of its most challenging periods, defined by a confluence of production slowdowns, intense regulatory scrutiny, and significant financial strain. The path forward is clouded by operational headwinds that question its ability to meet soaring commercial jet demand.

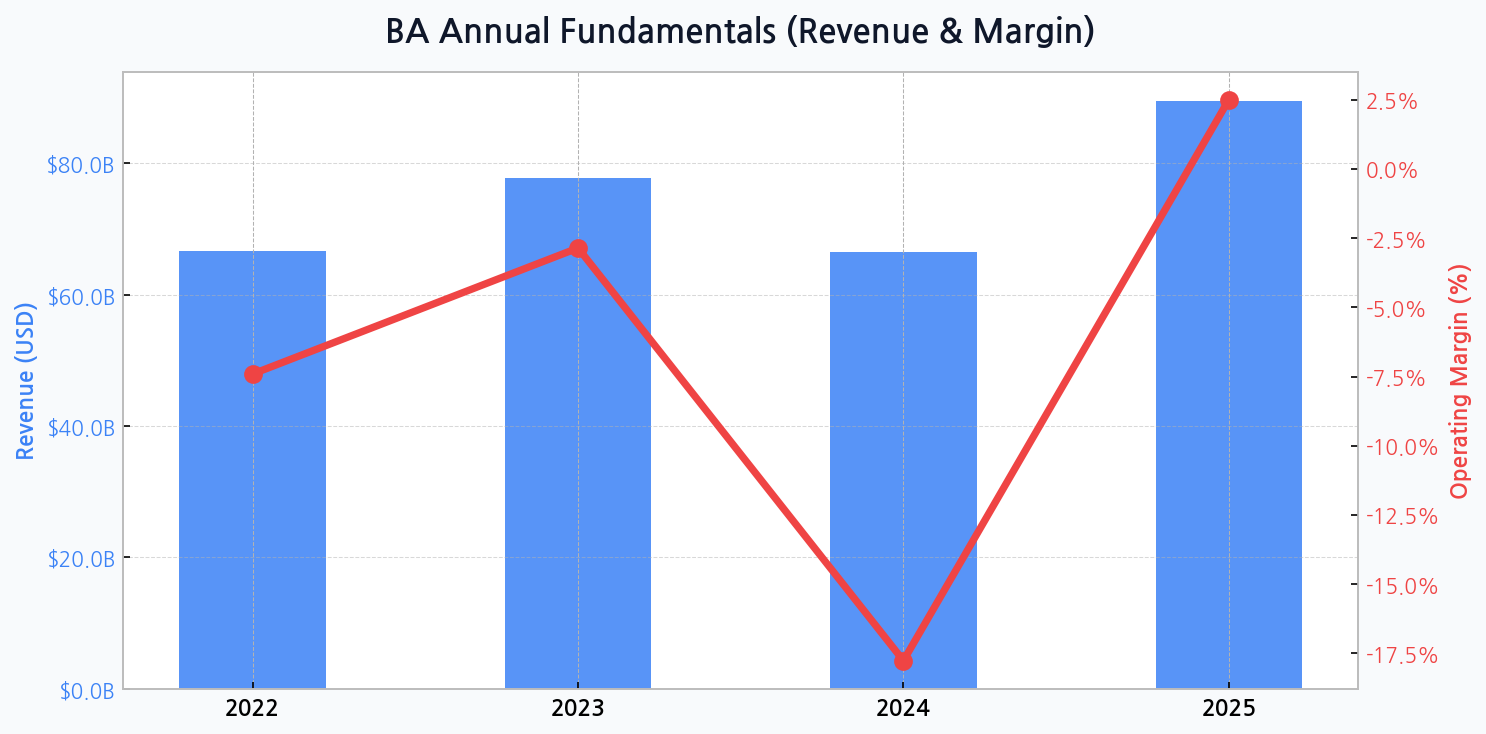

The Revenue Rollercoaster and Margin Collapse

Recent financial projections paint a volatile picture. After a revenue increase from $66.6B in 2022 to $77.8B in 2023, a sharp contraction to $66.5B is anticipated for 2024. More alarmingly, the operating margin is expected to collapse to a staggering -17.8% in 2024, a stark deterioration from -2.9% in 2023, signaling deep-seated operational and cost structure issues.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for BA

The Widening Competitive Chasm with Airbus

Boeing's internal struggles have created a significant opening for its primary rival, Airbus. As Boeing grapples with persistent production bottlenecks, Airbus has been capitalizing on the situation by ramping up its output and securing a larger share of new aircraft orders, creating a difficult competitive dynamic for the American manufacturer.

| Metric | Boeing (BA) | Airbus (EADSY) | Strategic Implication |

|---|---|---|---|

| Commercial Deliveries | ~ 528 Aircraft | ~ 735 Aircraft | Airbus leads in production output |

| Net Orders | ~ 1,314 | ~ 2,094 | Demand favors competitor significantly |

| Order Backlog | ~ 5,600+ | ~ 8,500+ | Airbus has a larger future revenue base |

DIFF Insight: The disparity in deliveries and net orders is not merely a cyclical trend; it reflects a deeper crisis of confidence among airlines. Boeing's inability to maintain a stable production rhythm has directly translated into lost market share. Rebuilding this trust is paramount and will require a prolonged period of flawless execution, which currently seems distant.

Supply Chain Paralysis Remains the Core Threat

The root of Boeing's predicament lies in a fragile and disrupted supply chain. Key suppliers for fuselages, engines, and avionics are struggling to meet revised production schedules. This systemic weakness not only delays deliveries but also inflates costs, directly contributing to the catastrophic margin decline and has eroded consumer trust.

"The challenge for Boeing is no longer about engineering or design innovation; it's about the fundamental ability to manufacture at scale reliably. Every quality escape and production halt sends ripples of uncertainty through the entire aviation ecosystem, from airlines to passengers."

Navigating a Mountain of Debt and Financial Risk

The company's financial health remains a significant concern. The debt ratio peaked at a precarious 112.6% in 2023, indicating that liabilities exceeded assets. While forecasts suggest an improvement to 96.8% by 2025, this deleveraging path is entirely dependent on achieving ambitious and uncertain cash flow targets.

| Risk Category | Threat Description | Probability | Impact Severity |

|---|---|---|---|

| Operational | Failure to stabilize 737 MAX production rates | High | High |

| Financial | Inability to generate cash flow to reduce debt | Medium | High |

| Regulatory | Increased FAA oversight leading to further delays/fines | High | Medium |

| Reputational | Further quality control incidents damaging brand trust | Medium | High |

DIFF Insight: This risk matrix highlights the interconnected nature of Boeing's challenges. A single operational failure can trigger regulatory action, which in turn hurts financial performance and brand reputation. This vicious cycle makes the company highly vulnerable to shocks and complicates any straightforward recovery narrative, impacting its long-term financial stability.

The 2025 Turnaround: A Credible Flight Path?

The forecast for 2025 presents a dramatic turnaround, with revenue projected to surge to $89.5B and operating margin returning to a positive 2.5%. While encouraging, this outlook appears highly optimistic. It presupposes a near-perfect resolution of supply chain issues and a flawless ramp-up in production that has eluded the company for years.

- Production Stability: Achieving consistent delivery schedules for the 737 MAX and 787 is the primary catalyst for recovery.

- Debt Management: Aggressive debt reduction is crucial to restore balance sheet health and investor confidence.

- Regulatory Compliance: Navigating intense FAA scrutiny without further setbacks is a non-negotiable prerequisite for a turnaround.

- Restoring Trust: Rebuilding the confidence of airlines and the flying public is essential for securing future orders.

Investment Scenarios and Core Triggers

The stock's future trajectory is dependent on a few key variables. The base case assumes a slow, gradual recovery, but both bull and bear scenarios remain highly plausible given the current volatility.

| Scenario | Core Trigger | Potential Outcome |

|---|---|---|

| Bull Case | Exceeds production targets; rapid debt reduction | Significant multiple expansion |

| Base Case | Gradual stabilization of production and supply chain | Modest, volatile appreciation |

| Bear Case | New major quality issue; further FAA penalties | Re-test of historical lows |

DIFF Insight: The extreme divergence between the bull and bear cases underscores the binary nature of the investment thesis. Unlike mature industrial peers, Boeing's valuation is less about incremental growth and more about its ability to overcome existential operational crises. Investors are not just buying earnings; they are betting on the company's capacity for systemic reform.