The Unshakable Foundation of a Real Estate Juggernaut

McDonald's core strength lies not in its menu, but in its vast real estate holdings. The company strategically owns the land and buildings at many of its franchised locations, creating a stable, high-margin revenue stream from rent that insulates it from the volatility of the fast-food industry. This model provides a powerful economic moat.

Franchise Royalty Streams Define the Revenue Landscape

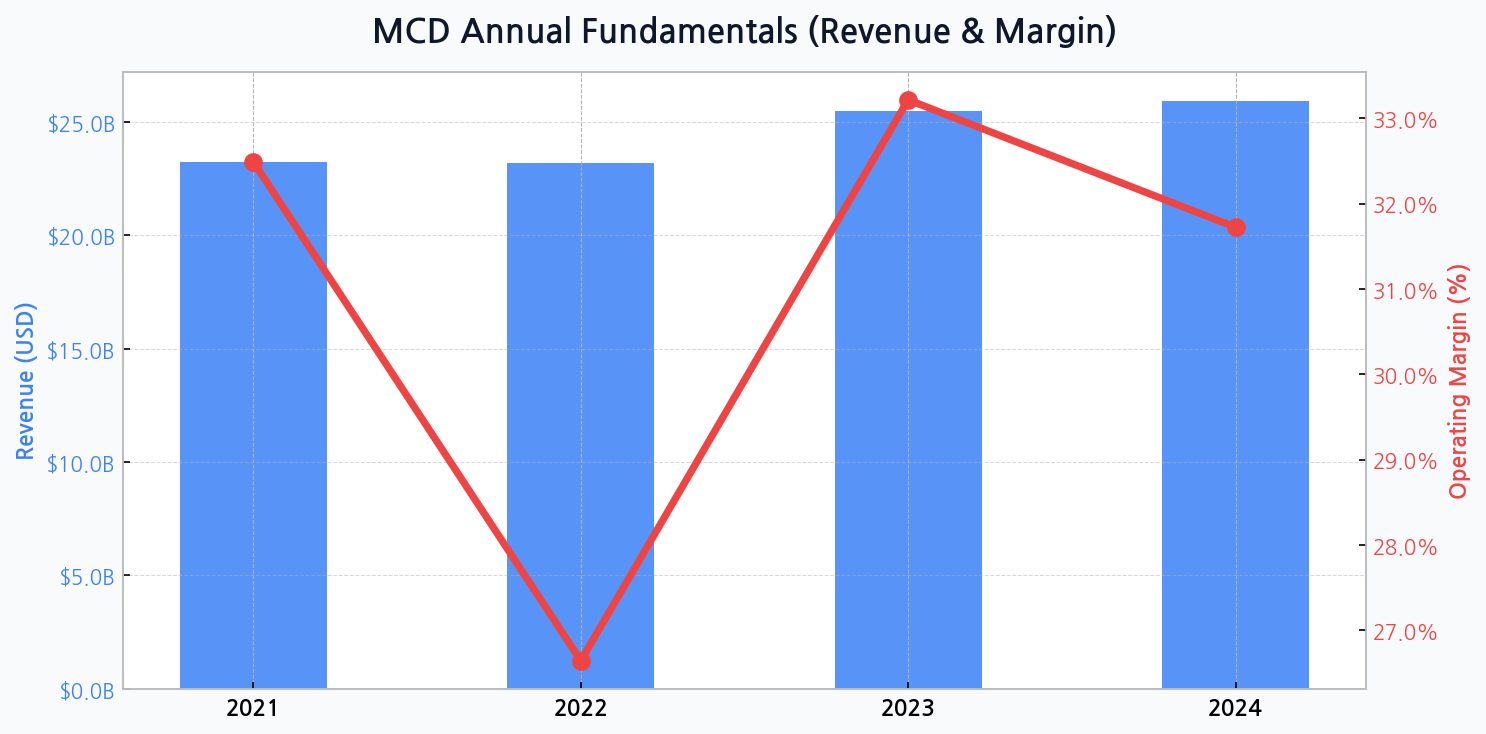

The company's revenue consistently hovers in the mid-$20 billion range, hitting $25.5B in 2023. However, the true story is the composition. A significant portion comes from high-margin franchise royalties and rent, a far more predictable source than direct restaurant sales, which are subject to fluctuating commodity and labor costs.

| Segment | Typical Revenue % | Margin Profile | Strategic Importance |

|---|---|---|---|

| Franchised Restaurants | ~ 60% | High | Stable Cash Flow, Low Capex |

| Company-Operated | ~ 40% | Lower | Innovation Hub, Brand Standard |

DIFF Insight: The franchise-heavy model is a masterstroke of capital efficiency. While company-operated stores are crucial for testing new concepts, the royalty-based income from franchisees provides the financial bedrock, allowing for consistent shareholder returns even when top-line growth appears modest.

Navigating the Tightrope of Profitability and Inflation

The true test of a global brand isn't just growth, but the ability to defend its margins against unrelenting macroeconomic pressures. McDonald's performance reveals both resilience and vulnerability.

After a margin compression in 2022, where operating margin fell to 26.6%, the company demonstrated significant pricing power and operational efficiency, rebounding to 33.2% in 2023. This recovery underscores the strength of its brand, but the challenge from a value-conscious consumer base remains a constant balancing act.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for MCD

Debt as a Tool, Not a Weakness

The company's debt ratio, consistently over 100% (peaking at 111.9% in 2022 before settling to 106.9% in 2024), appears alarming at first glance. However, this is a deliberate strategy. The debt is primarily used to finance its real estate portfolio, making it a form of strategic leverage rather than a sign of operational distress. The stability of rental income comfortably services this debt.

Capital Returns: A Beacon for Dividend Investors

McDonald's commitment to shareholders is unwavering, cementing its reputation as a reliable dividend payer. This is not an afterthought but a core component of its value proposition, enabled by the predictable cash flows from its franchise model. The company supplements dividends with opportunistic share buybacks.

| Year | Dividend Per Share (Est.) | Dividend Yield (Approx.) | Share Repurchases |

|---|---|---|---|

| 2022 | $5.66 | 2.2% | Substantial |

| 2023 | $6.28 | 2.1% | Consistent |

| 2024 (Proj.) | $6.68 | 2.3% | Ongoing |

DIFF Insight: The steady increase in dividends per share, even through periods of economic uncertainty, signals management's confidence in the long-term stability of the business model. For income-focused investors, this consistency is arguably more important than explosive growth.

Core Strengths in a Volatile Market

In an environment of shifting consumer preferences and economic headwinds, McDonald's relies on a triad of foundational strengths to maintain its market leadership. These pillars provide a defensive buffer that few competitors can replicate on a global scale.

- Unmatched Brand Recognition: The Golden Arches are one of the most recognized symbols globally, creating an instant consumer trust that lowers marketing barriers.

- Real Estate Arbitrage: The ability to generate two forms of income—food sales and rent—from a single location is a unique and powerful advantage.

- Scale and Supply Chain Mastery: Its global logistics network allows for immense purchasing power, helping to mitigate the impact of inflation on input costs better than smaller rivals.

Valuation in the Lens of Market Peers

While McDonald's trades at a premium compared to some peers, this is often justified by its superior profitability, lower risk profile, and consistent capital returns. The market rewards the stability inherent in its real estate and franchise-centric business model.

| Ticker | Company | Forward P/E (Approx.) | Dividend Yield |

|---|---|---|---|

| MCD | McDonald's | 23x | 2.3% |

| YUM | Yum! Brands | 22x | 1.9% |

| QSR | Restaurant Brands Int'l | 18x | 3.2% |

DIFF Insight: McDonald's P/E ratio reflects investor confidence in its earnings quality and stability. While Restaurant Brands (QSR) offers a higher yield, its lower valuation multiple suggests the market perceives greater operational risk compared to MCD's fortress-like model.