The Volatility Paradox: A Foundation Built on Shifting Sands

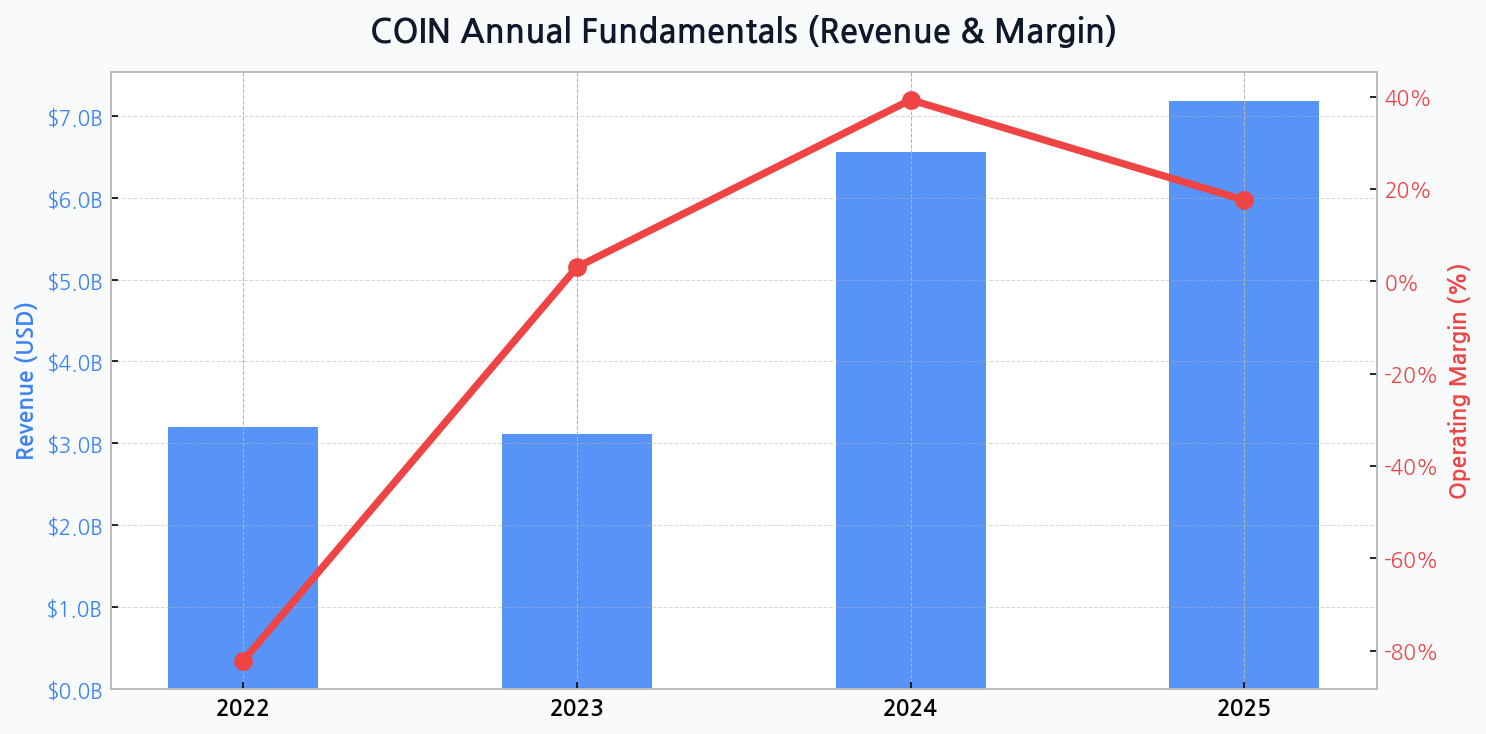

Coinbase's financial narrative is intrinsically tied to the tumultuous cycles of the cryptocurrency market. The firm's 2022 performance serves as a stark reminder, where revenue stood at $3.2 billion but was overshadowed by a staggering operating margin of -82.2%. This illustrates a core vulnerability: a business model heavily reliant on transaction volumes that evaporate during market downturns, exposing a rigid cost structure.

From Deep Freeze to Thaw: The 2023 Profitability Pivot

The subsequent year marked a dramatic operational turnaround. While 2023 revenue of $3.1 billion was marginally lower, the company achieved a positive 3.1% operating margin. This reversal was not driven by market euphoria but by stringent internal discipline, signaling a strategic shift from growth-at-all-costs to sustainable operations, a crucial step in maturing as a public entity.

| Metric | Coinbase (COIN) | Financial Tech Average | Exchange Average |

|---|---|---|---|

| P/E (Forward) | ~ 45x | ~ 22x | ~ 18x |

| P/S (TTM) | ~ 15x | ~ 5x | ~ 7x |

| EV/EBITDA | ~ 38x | ~ 14x | ~ 11x |

DIFF Insight: The premium valuation multiples for Coinbase reflect the market's pricing-in of crypto's high-beta growth potential, viewing it more as a disruptive technology play than a traditional financial exchange. This premium is both a vote of confidence and a significant risk, as any failure to meet lofty growth expectations could trigger a severe correction. The disparity underscores the market's struggle to categorize and value a company at the intersection of finance and nascent technology.

Beyond the Retail Frenzy: The Institutional Custody Gambit

Recognizing the fickle nature of retail trading, Coinbase is aggressively building out its institutional offerings. Services like Prime and Custody aim to create stickier, more predictable revenue streams from hedge funds, asset managers, and corporations entering the digital asset space. This strategic pivot is fundamental to reducing the company's correlation with spot price volatility and building a more resilient financial base.

"The goal is not to predict the crypto market, but to build the foundational infrastructure that serves it, regardless of price direction. We are building the rails for the future of finance."

Quantifying the Crypto Beta: A High-Stakes Correlation

Despite diversification efforts, Coinbase's performance remains a high-beta play on the crypto ecosystem. Projections for 2024 anticipate a revenue surge to $6.6 billion with a robust 39.3% margin, clearly tied to renewed market optimism. The more tempered 2025 forecast of $7.2 billion in revenue and a 17.6% margin suggests an expected market cooling. Success depends on building institutional-grade infrastructure that can capture value even as market fervor wanes, thereby mitigating its inherent cyclical dependency and creating more diversified revenue streams.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for COIN

The Regulatory Gauntlet and Its Double-Edged Sword

The evolving regulatory landscape in the United States and globally is the single largest external factor influencing Coinbase's trajectory. While clear regulations could unlock enormous institutional investment and legitimize the asset class, an adversarial stance from bodies like the SEC poses a persistent existential threat. The company's future is as much a legal and political battle as it is a technological or financial one.

Navigating the Headwinds: A Forward-Looking Risk Assessment

| Risk Factor | Probability | Impact Severity | Mitigation Strategy |

|---|---|---|---|

| Adverse SEC Ruling | Medium | High | Geographic Diversification, Product Scoping |

| Sustained Crypto Bear Market | High | High | Subscription & Service Revenue Growth |

| Platform Hack / Security Breach | Low | Critical | Cold Storage, Insurance Fund, Audits |

| Fee Compression from Competition | High | Medium | Value-Add Services (Staking, Custody) |

DIFF Insight: This matrix highlights that Coinbase's most severe risks are largely outside its direct control, stemming from market cycles and regulatory whims. The key to long-term viability lies in executing mitigation strategies that build a defensive moat. Success in growing subscription and service-based revenue is the most critical internal lever to counteract external market pressures and de-risk the investment thesis.

Deleveraging the Balance Sheet for a Sustainable Future

A bright spot in the company's narrative is its improving financial health. The debt ratio is on a clear downward trajectory, falling from a precarious 93.9% in 2022 to a projected 50.1% by 2025. This deleveraging, coupled with a growing asset base forecasted to reach $29.7 billion in 2025, provides the stability needed to weather market downturns and invest in strategic growth areas without excessive financial strain.

The Path to Becoming an Apex Financial Predator

- Diversification Imperative: Reduce reliance on retail transaction fees by expanding staking, custody, and subscription services.

- Regulatory Moat: Leverage its compliance-first approach as a competitive advantage to attract institutional capital wary of unregulated platforms.

- Global Expansion: Target markets with clearer regulatory frameworks to de-risk from U.S.-centric policy shifts.

- Technological Edge: Continue to invest in core infrastructure, including its Layer-2 solution, Base, to build an integrated ecosystem.