The Unrivaled Architect of the Silicon Age

ASML is not merely a participant in the semiconductor industry; it is the foundational enabler. The company's extreme ultraviolet (EUV) lithography machines are the sole technology capable of producing the world's most advanced microchips, granting it a structural monopoly that is nearly impossible to replicate.

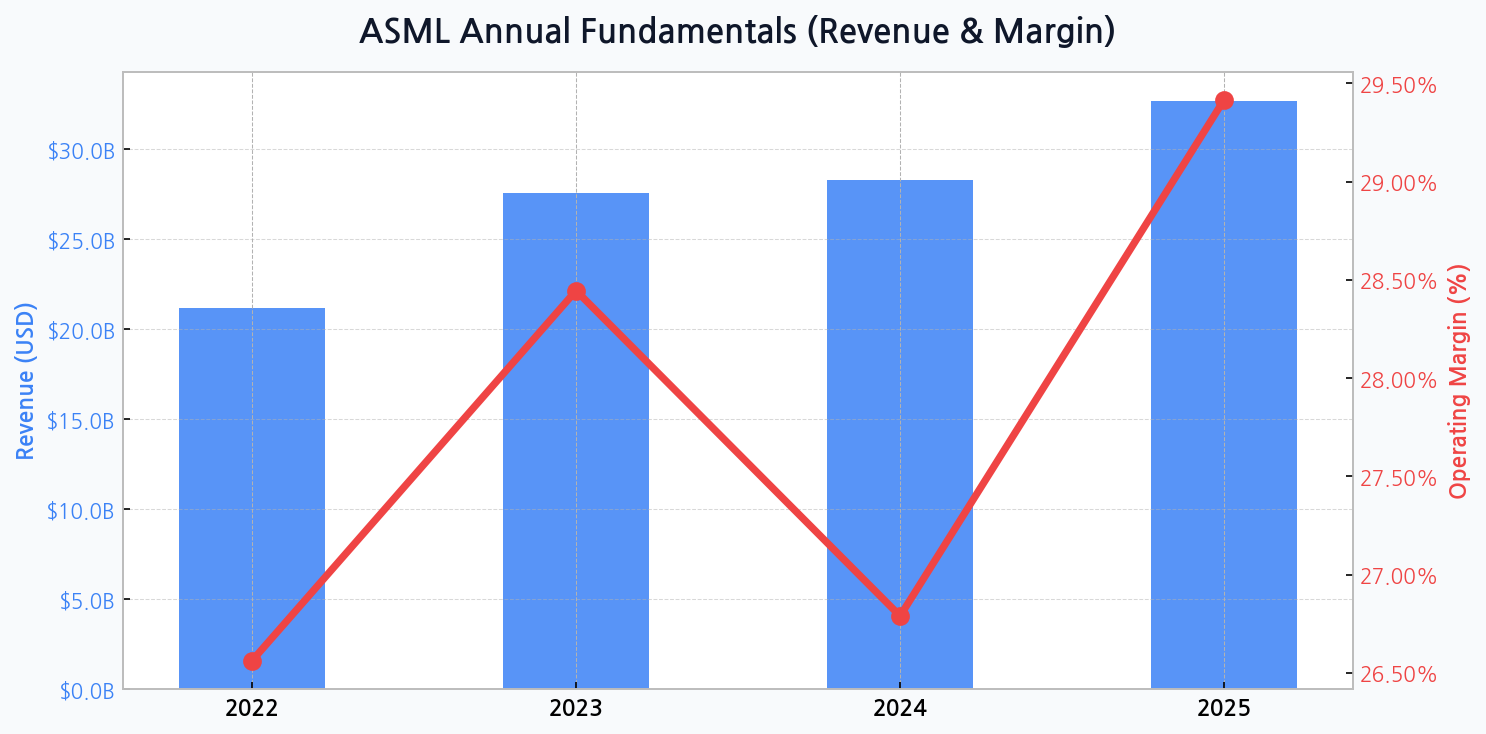

Navigating the Peaks and Valleys of Profitability

The company's financial trajectory reflects both its growth and the industry's cyclicality. Revenue surged from $21.2B in 2022 to $27.6B in 2023, with operating margin expanding to 28.4%. A temporary softening is anticipated in 2024, with revenue at $28.3B and margins contracting to 26.8%, before a powerful rebound projected for 2025 to $32.7B in revenue and a robust 29.4% margin.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for ASML

The Economic Moat Carved by Light

ASML's competitive advantage is rooted in decades of R&D and a complex supply chain that competitors cannot feasibly recreate. This unrivaled technological dominance ensures that every major chipmaker, from TSMC to Samsung and Intel, is a dependent customer, creating a predictable and powerful revenue stream tied directly to the advancement of Moore's Law.

| Company | Ticker | Forward P/E Ratio | Price/Sales (TTM) |

|---|---|---|---|

| ASML Holding N.V. | ASML | ~ 45x | ~ 17.1x |

| Applied Materials | AMAT | ~ 24x | ~ 7.5x |

| Lam Research | LRCX | ~ 28x | ~ 8.2x |

| KLA Corporation | KLAC | ~ 26x | ~ 9.0x |

DIFF Insight: The significant premium in ASML's valuation multiples is not speculative; it's a direct reflection of its monopoly status in the most critical segment of chip production. While peers compete in deposition and etch, ASML stands alone in advanced lithography. This premium is the market's price for a near-absolute technological barrier to entry and long-term pricing power.

The Double-Edged Sword of Geopolitics

The greatest challenge for ASML is not competition, but the weaponization of its supply chain. Export restrictions to regions like China represent a direct cap on its Total Addressable Market, a variable dictated by policymakers, not engineers.

Strengthening the Financial Foundation

Despite heavy capital expenditures, ASML's balance sheet is improving. The company's total assets are projected to grow from $36.3B in 2022 to $50.6B by 2025, while its debt ratio demonstrates a healthy decline from 75.7% to a more manageable 61.2% over the same period. This deleveraging showcases disciplined capital management and enhances its resilience against the cyclical nature of the semiconductor industry.

| Risk Factor | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Geopolitical Trade Curbs | High | High | Geographic Revenue Diversification |

| Semiconductor Cycle Downturn | Medium | High | Long-term Order Backlog |

| Supply Chain Disruption | Medium | Medium | Strategic Supplier Partnerships |

| R&D Execution Failure | Low | Very High | Massive & Sustained R&D Investment |

DIFF Insight: The risk matrix highlights that ASML's primary threats are external and political, rather than internal or competitive. The high probability of further trade restrictions necessitates a strategic focus on supporting foundry build-outs in the US, Europe, and Japan. Its substantial order backlog provides a crucial buffer against short-term market downturns, a key differentiator from peers.

The Engine Room of Growth: Logic vs. Memory

| Segment | 2023 Est. % | 2025 Est. % | Primary Driver |

|---|---|---|---|

| Logic | ~ 65% | ~ 70% | AI, HPC, Advanced Nodes |

| Memory (DRAM/NAND) | ~ 35% | ~ 30% | Data Center, Consumer Electronics |

DIFF Insight: The increasing revenue concentration in the Logic segment underscores ASML's role as a primary beneficiary of the AI revolution. While the memory market is more volatile, the relentless demand for more powerful computing processors for AI models provides a secular growth trend. This positions ASML's fate closely with the capital expenditure plans of leading-edge foundries.

Core Investment Thesis Summarized

- Absolute monopoly in the critical EUV lithography market.

- Direct beneficiary of global AI and high-performance computing trends.

- Improving financial health with a decreasing debt burden.

- Strong long-term visibility due to a massive order backlog.

The Dawn of a New Era with High-NA

The future growth trajectory is already being written by the next-generation High-NA EUV systems. These machines, costing over $350 million each, are essential for producing chips beyond the 2-nanometer node. As the sole supplier, ASML is not just selling equipment; it is selling the very roadmap for the future of the entire digital economy.