The Unwavering Growth Trajectory Fueled by AI

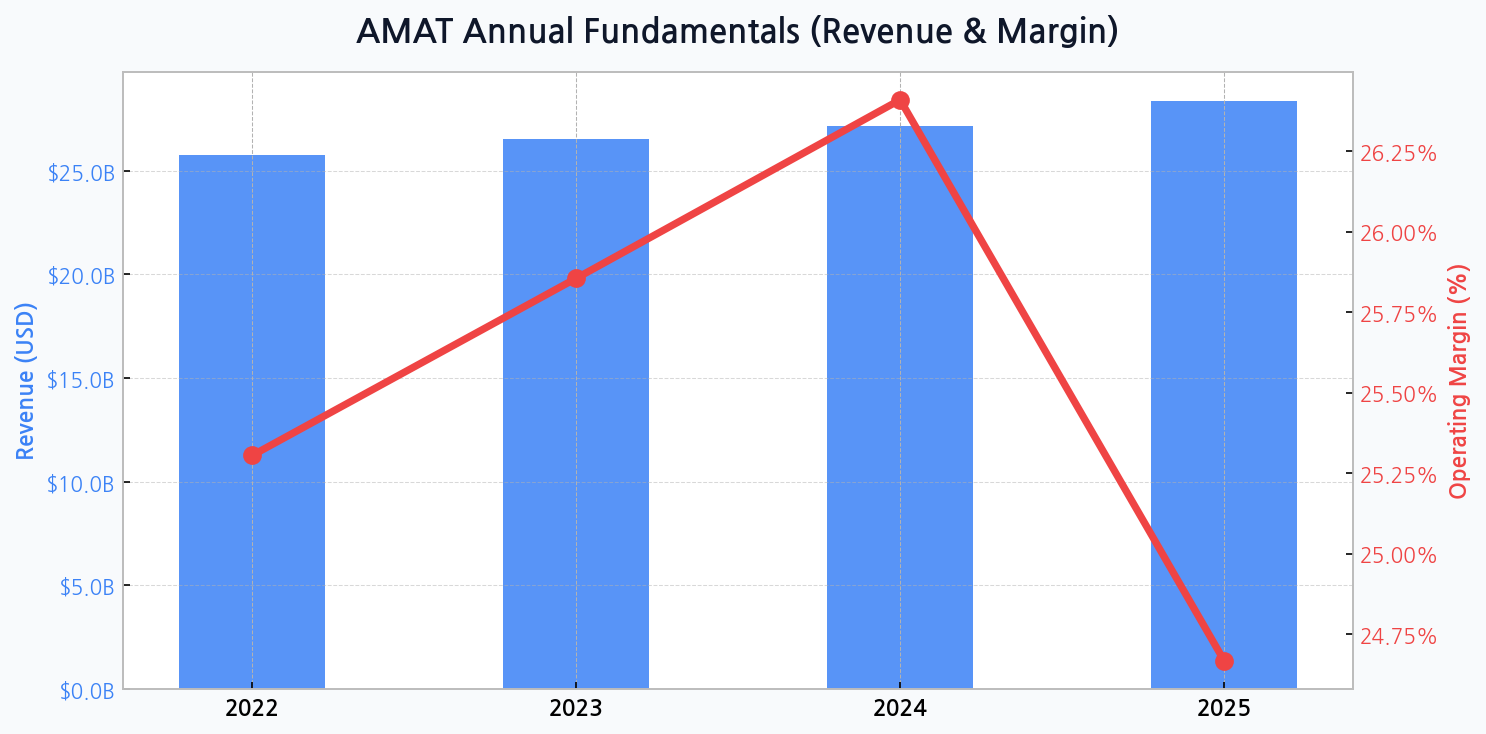

Applied Materials stands at the epicenter of the global AI infrastructure build-out. The company's revenue trajectory reflects this, with a steady climb from $25.8 billion in 2022 to a projected $28.4 billion by 2025. This momentum is directly fueled by the aggressive, capital-intensive fab expansions of semiconductor giants who are racing to meet insatiable demand for next-generation chips.

Valuation in the Face of Semiconductor Supercycles

Despite its critical role, AMAT's valuation must be viewed through the lens of a notoriously cyclical industry. Investors reward its market leadership but remain cautious of potential downturns, which can swiftly impact equipment spending. Comparing its multiples against peers provides a clearer picture of market sentiment.

| Company | Ticker | Forward P/E | EV/Sales |

|---|---|---|---|

| Applied Materials | AMAT | 24.5x | 7.8x |

| Lam Research | LRCX | 26.1x | 8.2x |

| KLA Corporation | KLAC | 28.3x | 10.5x |

| ASML Holding | ASML | 45.2x | 14.1x |

DIFF Insight: AMAT's valuation appears more conservative compared to ASML, which holds a monopoly in EUV lithography, and slightly below its direct competitors. This suggests the market may be pricing in the risks associated with its broad exposure to various equipment segments, unlike ASML's single-point dominance. The discount could represent an opportunity if AMAT successfully capitalizes on emerging technologies like Gate-All-Around (GAA) transistors.

The Looming Specter of Margin Compression

The most significant warning sign in AMAT's financial outlook is the forecasted drop in operating margin to 24.7% in 2025, a sharp decline from the 26.4% peak in 2024. This contraction, despite rising revenues, points to potential pricing pressure from major customers, escalating R&D costs for sub-3nm technologies, or shifts in product mix toward lower-margin equipment. It is a critical metric for investors to monitor.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for AMAT

[Chart] AMAT's annual revenue shows consistent growth, while its operating margin is projected to peak in 2024 before a notable decline in 2025.

Fortifying the Fortress: A Look at Financial Health

While margins present a concern, AMAT's balance sheet is becoming demonstrably stronger. The company has methodically reduced its debt ratio from a high of 54.4% in 2022 to a projected 43.8% in 2025. This deleveraging, coupled with asset growth to an estimated $36.3 billion, provides significant operational flexibility and resilience to navigate potential market downturns or fund strategic acquisitions.

Navigating the Geopolitical Chip War Battlefield

Operating at the apex of the semiconductor value chain places AMAT squarely in the middle of geopolitical crossfire, particularly between the U.S. and China. Export controls and trade restrictions represent a persistent threat to a significant portion of its revenue, while supply chain disruptions remain a constant operational risk. The company's ability to navigate this complex landscape is paramount.

Without Applied Materials' deposition and etch technologies, scaling to sub-3nm nodes is not just difficult, it's economically unviable. They are a linchpin in the roadmaps of both TSMC and Intel, making their strategic technology portfolio indispensable.

The Critical Risks on the Horizon

A systematic assessment of threats reveals that market cyclicality and geopolitical tensions are the most potent risks. While the company's leadership position is strong, it is not immune to macroeconomic shocks or sudden shifts in government policy that could halt customer investments overnight.

| Risk Factor | Probability | Impact Severity | Mitigation Strategy |

|---|---|---|---|

| Geopolitical Trade Curbs | High | High | Geographic Revenue Diversification |

| Semiconductor Downturn | Medium | High | Long-Term Service Agreements |

| Supply Chain Disruption | Medium | Medium | Multi-sourcing of Key Components |

| Competitor Innovation | Low | High | Aggressive R&D Investment |

DIFF Insight: The table highlights that the most probable and severe risks are external factors beyond AMAT's direct control. The company's primary defense is its deep integration with clients and diversification of its product lines. However, a severe, coordinated downturn in spending from its top three customers could still override these mitigating efforts, posing an existential threat to short-term profitability.

Dissecting the Competitive Moat

AMAT's competitive advantage, or 'moat', is built on decades of R&D, a vast patent portfolio, and an entrenched global service network. Its leadership is particularly pronounced in deposition and etch, two of the most critical steps in chip manufacturing. This technological dominance creates high switching costs for customers, solidifying its market position against rivals.

| Segment | Applied Materials (AMAT) | Lam Research (LRCX) | Tokyo Electron (TEL) |

|---|---|---|---|

| Deposition (CVD/PVD) | Market Leader | Strong Competitor | Strong Competitor |

| Etch | Strong No. 2 | Market Leader | Strong Competitor |

| Ion Implant | Market Leader | N/A | N/A |

| Process Control | Competitor | Competitor | Competitor (KLA Dominates) |

DIFF Insight: This breakdown reveals that while AMAT is a dominant force, it does not hold a monopoly in its key markets, particularly in Etch where it trails Lam Research. This intense competition is a likely contributor to the margin pressures seen in the forecast. AMAT's strength lies in its comprehensive portfolio, offering clients a 'one-stop-shop' advantage that individual competitors struggle to match.

Strategic Imperatives for Sustained Leadership

To secure its future, Applied Materials must focus on several key areas. The path forward is not merely about maintaining market share but about anticipating the next technological inflection point and navigating the ever-present risk of cyclical industry downturns. Success will be defined by strategic discipline and relentless innovation.

- Margin Defense: Prioritize high-margin services and advanced packaging solutions to offset potential commoditization in mature equipment lines.

- R&D Focus: Double down on R&D for next-generation technologies like Gate-All-Around (GAA) and advanced materials to create a definitive technology gap.

- Client Diversification: While servicing giants is key, expanding its footprint with emerging memory and specialty chip manufacturers could reduce concentration risk.

- Supply Chain Resilience: Continue building a robust, geographically diversified supply chain to insulate operations from geopolitical shocks.