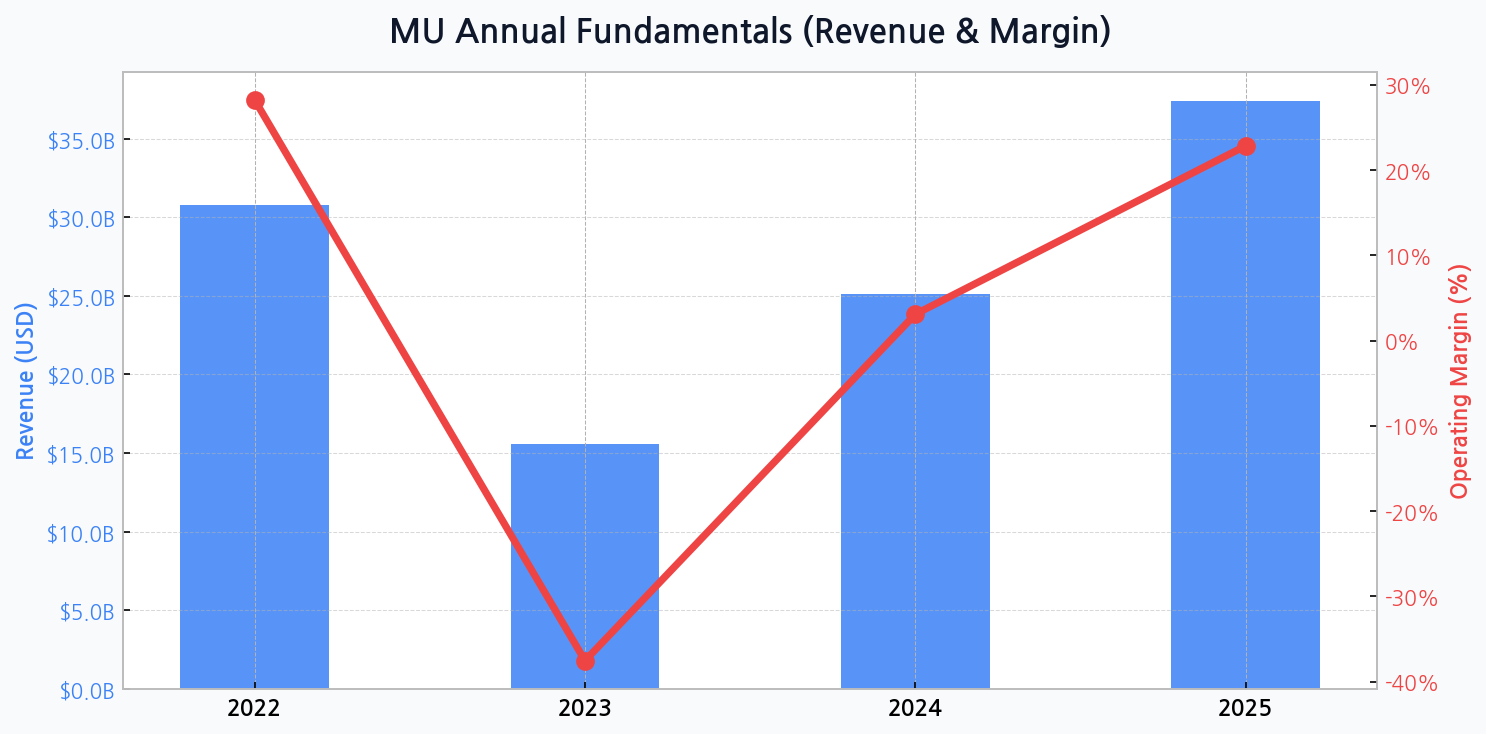

The Echo of a Cyclical Collapse

The memory industry's cyclical nature was on full display as Micron's fortunes plummeted. After a robust 2022 with $30.8B in revenue and a healthy 28.2% operating margin, the company faced a stark reality in 2023. Revenue was slashed nearly in half to $15.5B, while margins inverted to a staggering -37.5%, signifying a truly brutal memory downcycle.

The AI Lifeline in High-Bandwidth Memory

The narrative is now shifting dramatically towards recovery, driven almost entirely by demand from the AI sector. The forecast for 2025 projects a powerful rebound to $37.4B in revenue and a 22.8% margin, pinning hopes on Micron's competitiveness in high-bandwidth memory (HBM), a critical component for AI accelerators.

| Competitor | Est. HBM3/3E M/S | Key Advantage | Strategic Challenge |

|---|---|---|---|

| SK Hynix | ~ 50-55% | First-mover in HBM3 | Maintaining technology lead |

| Micron | ~ 20-25% | Power efficiency (HBM3E) | Scaling production capacity |

| Samsung | ~ 20-25% | Vast production scale | Catching up on latest tech |

DIFF Insight: This table highlights the intense oligopolistic competition in the HBM space. While SK Hynix currently leads, Micron's focus on power-efficient designs for its HBM3E products could be a key differentiator for power-hungry AI data centers. Micron's ability to execute on its production roadmap will be the ultimate determinant of its success against giants like Samsung.

A Market Structure Forged in Fire

The memory market is not for the faint of heart. It is a consolidated game of chicken where only those with the deepest pockets and the most advanced technology survive the downturns to reap the rewards of the upswing.

This industry structure, an oligopoly, means that while downturns are severe, the survivors are positioned for outsized gains during recovery. Pricing power can return swiftly once supply and demand dynamics rebalance, a trend anticipated through 2024 and 2025.

Navigating a Treacherous Balance Sheet

The cost of staying competitive is steep. Micron's financial health reflects this, with its debt ratio climbing from a manageable 24.7% in 2022 to a projected 35.0% by 2024. This increased leverage is necessary to fund the immense capital expenditures for next-generation technology but introduces significant financial risk.

- Rising Leverage: Debt ratio is expected to peak in 2024 as CAPEX for HBM ramps up.

- Asset Fluctuation: Total assets dipped to $64.3B in 2023 before a planned expansion to $82.8B by 2025.

- Cash Flow Pressure: Negative margins in 2023 put immense pressure on operating cash flow, necessitating borrowing.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for MU

[Chart] The chart illustrates Micron's volatile journey, showing the deep trough in revenue and operating margin in 2023 followed by a strong projected recovery into 2025.

The High Stakes of Technological Leadership

In the semiconductor industry, being a technology leader is not optional; it is a prerequisite for survival. The transition to advanced nodes and new memory architectures like HBM3E requires flawless execution and immense investment. Any misstep can result in a loss of market share that is difficult to reclaim, demanding sharp capital allocation discipline.

An Unforgiving Risk Environment

Beyond market cycles, Micron operates within a complex web of external threats. Geopolitical tensions, supply chain vulnerabilities, and macroeconomic headwinds can disrupt operations and demand forecasts with little warning.

| Risk Factor | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Memory Cycle Downturn | High | Severe Margin Erosion | Focus on high-value products (HBM) |

| Geopolitical Tensions | Medium | Supply Chain Disruption | Geographic diversification of manufacturing |

| Technology Execution | Medium | Loss of Market Share | Aggressive R&D investment |

DIFF Insight: The risk matrix clarifies that while cyclicality is a known and ever-present danger, the execution risk in technology transitions is just as critical. A failure to deliver HBM3E at scale and on schedule would not only impact revenue but could permanently damage its relationship with key AI customers, ceding ground to competitors.

The Bull and Bear Dichotomy

Investor sentiment is torn between two powerful narratives. The bull case sees Micron as a primary beneficiary of the AI revolution, transforming it from a simple cyclical stock into a secular growth story. The bear case, however, warns that the current optimism is overblown and that the fundamental, volatile nature of the memory market remains unchanged.

| Scenario | Core Trigger | Implied Valuation |

|---|---|---|

| Bull Case | Sustained AI demand; HBM market share gain | Significant multiple expansion |

| Base Case | Typical cyclical recovery; modest AI contribution | Valuation aligned with historical averages |

| Bear Case | AI demand falters; China tensions escalate | Return to trough-level multiples |

DIFF Insight: This table frames the investment thesis not as a single outcome but as a distribution of possibilities. The key variable is the persistence of AI-driven demand. If this demand is truly a long-term paradigm shift, historical valuation multiples for Micron may no longer be relevant, justifying the bull case. If it's a bubble, the downside is substantial.