The Strategic Pivot from Mobile Saturation

ARM's historical dominance in mobile processors is a double-edged sword, providing a stable cash flow but facing market maturity. The company is now forcefully redirecting its focus toward the high-growth arenas of AI-enabled PCs and cloud data centers, where its low-power architecture presents a compelling value proposition against incumbent players.

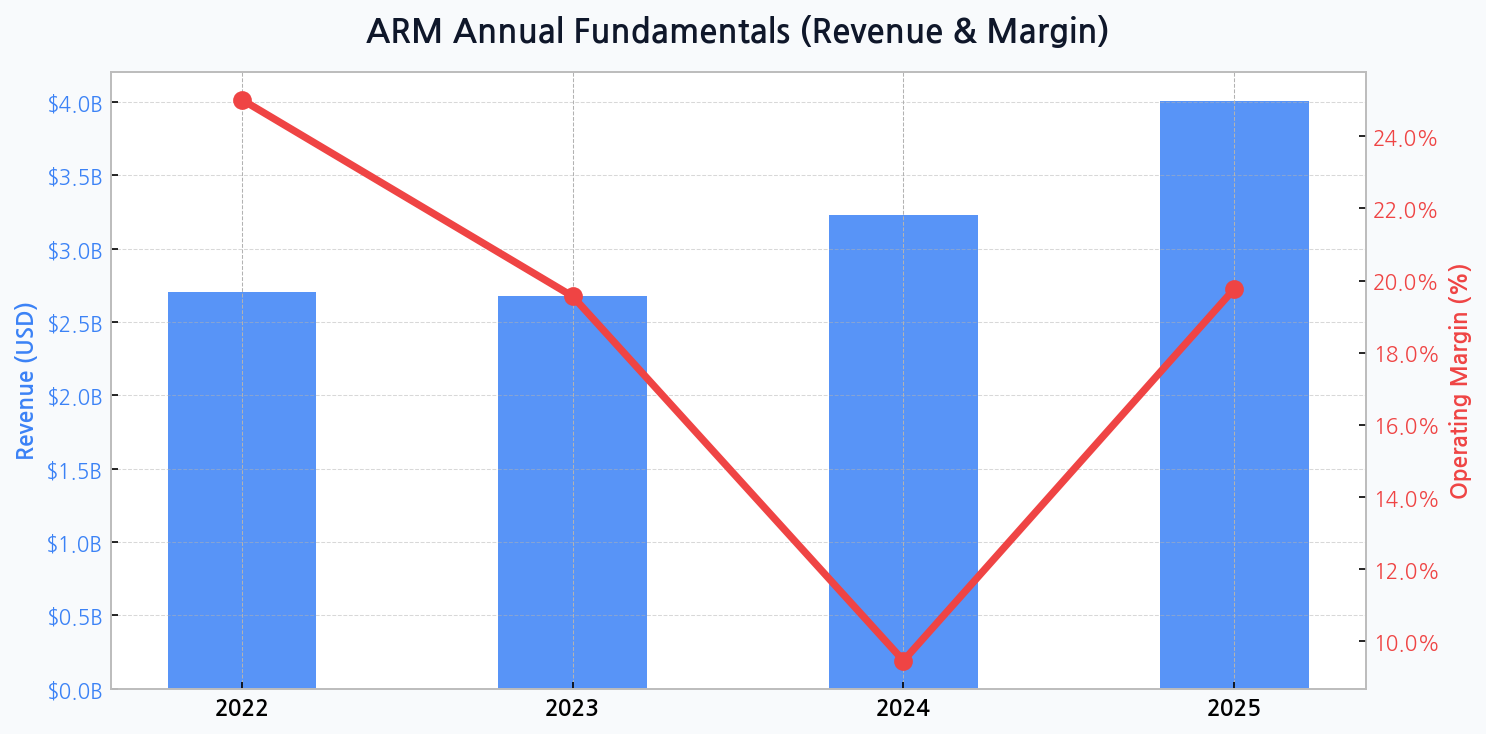

Deconstructing the New Revenue Engine

This strategic shift is already reflected in revenue forecasts, which show a jump from a stagnant $2.7 billion in 2023 to $3.2 billion in 2024, and a further leap to $4.0 billion by 2025. The core driver is the anticipated higher royalty rates from the more complex v9 architecture, essential for AI and server-grade performance.

| Segment Focus | 2023 Contribution | 2025 Target | Growth Driver |

|---|---|---|---|

| Mobile & IoT | ~ 70% | ~ 50% | Mature Market |

| AI PC & Automotive | ~ 20% | ~ 30% | ARMv9 Adoption |

| Cloud & Data Center | ~ 10% | ~ 20% | Total Cost of Ownership |

DIFF Insight: The table illustrates a deliberate cannibalization of mobile's dominance in the revenue mix, replaced by higher-margin segments. This isn't a sign of weakness in the core business but a calculated strategy to capture future value. Success hinges on convincing data center operators that ARM's power efficiency translates to superior total cost of ownership at scale.

The Margin Paradox: Investing for Future Dominance

The transition comes at a steep price. The operating margin plummeted from 19.6% in 2023 to a startling 9.5% in 2024, a clear indicator of massive upfront R&D and market-entry investments. However, the projected rebound to 19.8% in 2025 suggests management expects this strategic spending surge to yield rapid returns as new licensing and royalty agreements kick in.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for ARM

Wall Street's Verdict on the v9 Architecture

The market is not valuing ARM based on its mobile legacy; it's placing a high-stakes bet on the v9 instruction set becoming the new industry standard for inference at the edge and in the cloud. The current valuation is a reflection of this 'tollbooth' potential on future AI data traffic.

Valuation Under a Microscope: Justifying the Premium

ARM's valuation multiples are undeniably stretched, trading at a significant premium to the broader semiconductor industry. This is not justified by current earnings but by its unique, high-margin IP licensing model, which resembles a software company more than a traditional chip maker. The market is pricing in near-perfect execution of its expansion strategy.

| Company/Standard | Model | Forward P/E Ratio | Key Moat |

|---|---|---|---|

| Arm Holdings (ARM) | IP Licensing | > 70x | Ecosystem Lock-in |

| Semiconductor Average | Design & Fab | ~ 25x | Manufacturing Scale |

| RISC-V (Concept) | Open Standard | N/A | Customizability & No Fees |

DIFF Insight: The stark contrast in valuation highlights ARM's unique position as an IP gatekeeper. Unlike its peers who sell physical chips, ARM sells the blueprints, creating a highly scalable and profitable model. However, this also makes it vulnerable to disruption from open-source alternatives like RISC-V, which threatens to commoditize its core offering.

Key Pillars of ARM's Expanding Moat

- Ecosystem Inertia: Decades of development have created a vast ecosystem of software, tools, and engineering talent optimized for ARM architecture, making a switch costly and complex for partners.

- Power Efficiency DNA: ARM's foundational expertise in low-power design, honed in the mobile era, is now a critical differentiator in energy-conscious data centers and battery-powered AI devices.

- ARMv9 Security & AI Features: The latest architecture introduces specialized instructions for AI/ML workloads and enhanced security features, directly addressing the core needs of its target growth markets.

A Healthier Balance Sheet Fuels Ambition

Underpinning this aggressive expansion is a rapidly improving financial foundation. The company's debt ratio is on a clear downward trajectory, falling from 45.5% in 2022 to a projected 23.4% in 2025, while total assets are set to grow from $6.5 billion to $8.9 billion in the same period. This deleveraging provides critical flexibility to fund R&D without relying on costly external financing.

Navigating the Geopolitical and Competitive Minefield

Despite its strong position, ARM faces significant external threats that could derail its growth story. The geopolitical fragmentation between the US and China directly impacts its relationship with Arm China, a major revenue source. Concurrently, the rise of open standards like RISC-V presents a long-term architectural challenge.

| Risk Factor | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| US-China Tech War | High | Severe | Regional IP Fencing |

| RISC-V Adoption | Medium | High | Ecosystem & Software Moat |

| Execution on Cloud | Medium | Severe | Strategic Partnerships |

DIFF Insight: This matrix clarifies that ARM's biggest challenges are not purely technical but geopolitical and structural. While it can innovate to stay ahead of RISC-V, it has far less control over regulatory decisions from Washington or Beijing. Investors must price in this high degree of macro uncertainty, which is not always reflected in financial models.