The Paradox of Growth: Revenue Climbs as Profitability Retreats

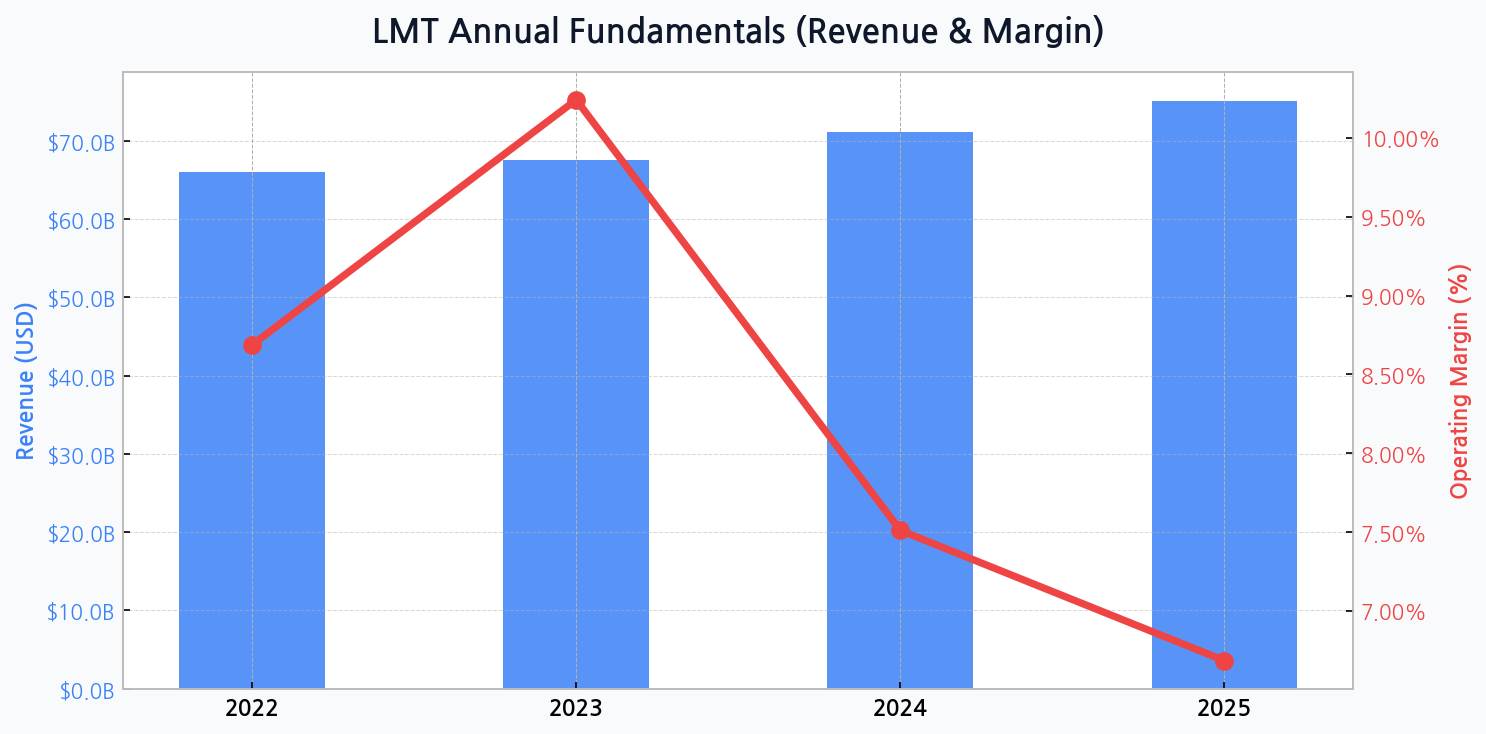

Lockheed Martin presents a compelling but complex financial narrative. On one hand, the revenue stream is expanding impressively, projected to swell from $66.0B in 2022 to a formidable $75.0B by 2025. This growth is a direct reflection of a world re-arming in the face of geopolitical instability.

However, this top-line strength is shadowed by a concerning trend in profitability. The operating margin, after peaking at a healthy 10.2% in 2023, is forecasted to compress significantly to 6.7% by 2025. This margin erosion signals intense pressure from fixed-price contracts, supply chain inflation, and escalating R&D costs for next-generation platforms.

Aeronautics Remains the Undisputed Crown Jewel

| Business Segment | Primary Driver | Strategic Importance |

|---|---|---|

| Aeronautics | F-35 Program | Core revenue and cash flow engine |

| Missiles & Fire Control | Hypersonics, PAC-3 | High-growth, high-tech frontier |

| Rotary & Mission Systems | Sikorsky, Aegis Combat System | Diverse and stable contracts |

| Space | GPS, Satellites | Long-term strategic growth area |

DIFF Insight: The F-35 program within the Aeronautics division is not just a product; it's a multi-decade ecosystem that locks in allies and generates a continuous stream of revenue through production, sustainment, and upgrades. While this segment is the primary growth driver, its sheer scale also makes it the most significant source of risk related to cost overruns and political scrutiny. The diversification into high-margin areas like hypersonics is a crucial hedge against the maturation of its core aviation platform.

Fortifying the Balance Sheet Comes at a Cost

The company's asset base is on a clear expansion path, expected to reach nearly $59.8B by 2025 from $52.9B in 2022. This expansion supports a growing backlog and investments in future capabilities. Yet, this growth is heavily financed by debt, creating an alarming debt ratio that is set to climb from 82.5% to a very high 88.8% over the same period.

This aggressive leveraging strategy enables robust capital returns to shareholders but introduces significant financial risk, making the company more vulnerable to interest rate fluctuations and credit market tightening. Managing this delicate balance between growth investment and financial prudence is a key challenge for leadership.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for LMT

The Geopolitical Tailwinds Fueling the Order Books

The current global security environment acts as a powerful, non-cyclical demand driver for Lockheed Martin's portfolio. Rising defense budgets among NATO allies and in the Indo-Pacific are not a temporary spike but a structural shift, translating directly into a fortified and long-duration backlog that provides unparalleled revenue visibility for the next decade.

Valuation Reflects a Premium for Unwavering Demand

| Company | Ticker | Forward P/E Ratio | Dividend Yield |

|---|---|---|---|

| Lockheed Martin | LMT | ~ 17x | ~ 2.9% |

| RTX Corporation | RTX | ~ 19x | ~ 2.3% |

| Northrop Grumman | NOC | ~ 15x | ~ 1.8% |

| Boeing (Defense) | BA | N/A | N/A |

DIFF Insight: Lockheed Martin trades at a premium valuation compared to some peers like Northrop Grumman, which the market justifies based on the sheer dominance of the F-35 platform and its predictable, long-term cash flow. Investors are rewarding LMT for its stability and direct exposure to rising global defense spending. However, this premium also means the stock is priced for near-perfect execution, leaving little room for error on major programs or unexpected margin compression.

The Three Pillars of LMT's Strategic Moat

- Unmatched Backlog: A multi-year order book exceeding $150 billion provides exceptional revenue visibility and insulates the company from short-term economic downturns.

- Technological Supremacy: Decades of investment have created a deep technological moat in stealth, hypersonics, and integrated warfare systems that is nearly impossible for new entrants to replicate.

- Entrenched Government Relationships: A deep, politically insulated network of contracts and lobbying efforts across the globe forms a formidable barrier to entry and ensures its role as a prime contractor.

Navigating a Minefield of Execution and Political Risk

While demand is secure, the primary operational challenge lies in execution. The F-35 program, a cornerstone of revenue, is perpetually under a microscope for cost controls and delivery timelines. Any significant delays or performance issues can have an outsized impact on financial results and political support.

Furthermore, the company's fate is inextricably linked to government budget cycles. A future political shift towards domestic priorities or a period of fiscal austerity could challenge the predictable budget allocations that form the bedrock of LMT's financial planning.

Mapping the Primary Threats to Continued Dominance

| Risk Factor | Probability | Potential Impact |

|---|---|---|

| Defense Budget Cuts | Medium | High |

| Supply Chain Disruption | High | Medium |

| Key Program Delays | Medium | High |

| Technological Obsolescence | Low | Critical |

DIFF Insight: While a major technological disruption from a competitor is a low-probability event, its impact would be existential. The most immediate and probable threats are operational: supply chain bottlenecks for critical components and the ever-present risk of delays on complex, fixed-price development programs. These operational frictions are the primary culprits behind the forecasted margin decline and represent the biggest challenge for management to overcome.