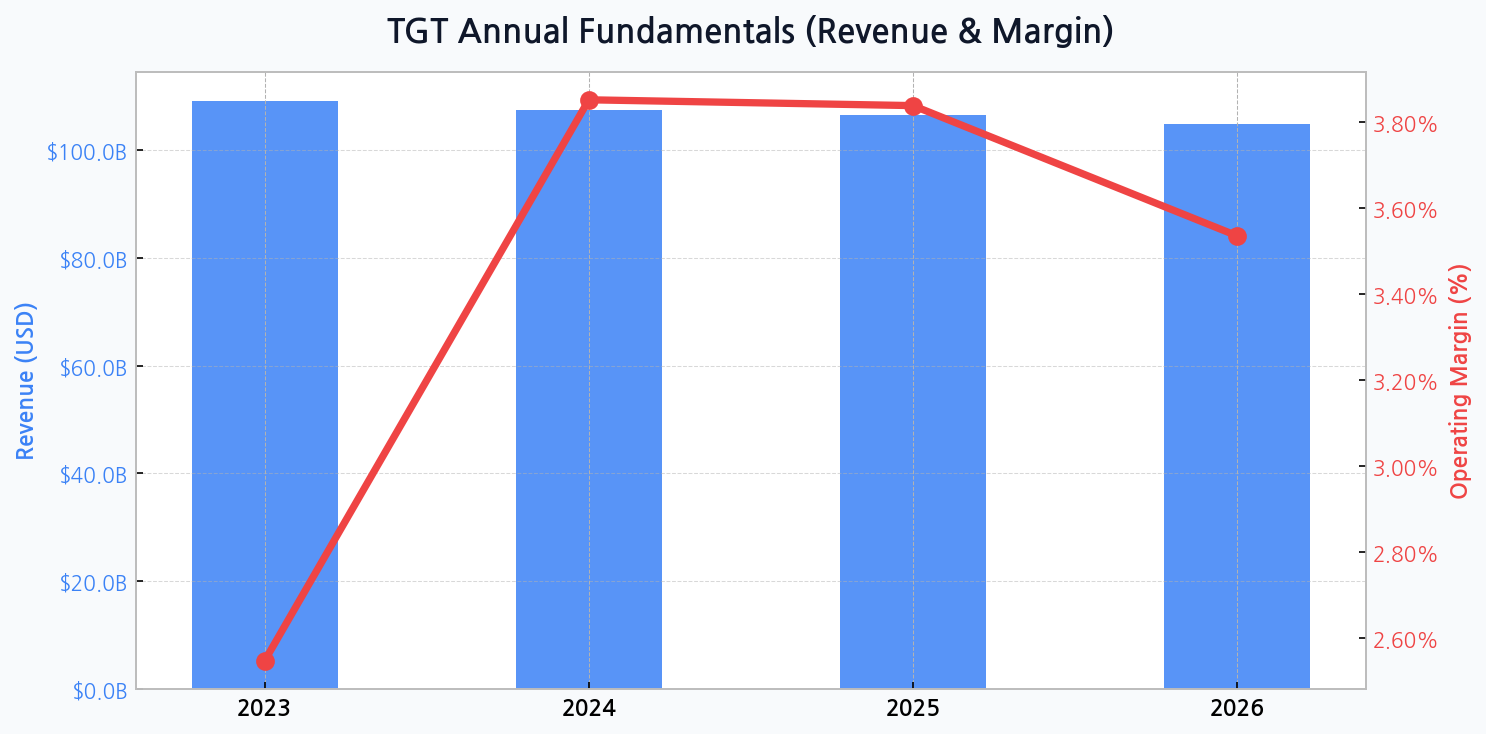

The Revenue Plateau Signals a Wary Consumer

Target's top-line trajectory tells a story of market saturation and shifting consumer priorities. The projected revenue decline from $109.1 billion in 2023 to $104.8 billion by 2026 is not a collapse, but a clear signal that the post-pandemic spending boom has ended. This plateau indicates significant discretionary spending headwinds as households prioritize essentials over wants.

Margin Recovery is a Double-Edged Sword

The most dramatic element of Target's recent performance is its margin rebound. After a difficult 2023 with a 2.5% margin, the company's improved inventory discipline drove a sharp recovery to 3.9% in 2024. However, the forecast shows a slight erosion back to 3.5% by 2026, suggesting that competitive pressures and promotional activity remain a constant threat to profitability.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for TGT

Decoding the Balance Sheet's Quiet Strength

While revenue grabs headlines, Target's management is executing a quiet but effective strategy of financial fortification. The consistent reduction in the debt ratio, from a high of 78.9% in 2023 to a more manageable 72.8% by 2026, is a testament to this focus. This strategic deleveraging, coupled with steady asset growth, enhances the company's resilience against economic shocks.

| Metric | Target (TGT) | Walmart (WMT) | Costco (COST) |

|---|---|---|---|

| Forward P/E Ratio | ~ 14.5x | ~ 25.0x | ~ 48.0x |

| Price/Sales (P/S) | ~ 0.6x | ~ 0.7x | ~ 1.5x |

| Dividend Yield | ~ 3.0% | ~ 1.4% | ~ 0.7% |

DIFF Insight: Target's valuation appears modest compared to its primary competitors, particularly Costco's premium multiple. This reflects market skepticism about its growth prospects in a discretionary-focused model. However, its attractive dividend yield suggests a strategy geared towards providing shareholder returns in a low-growth environment, positioning it as a value and income play rather than a growth story.

The Omnichannel Tightrope Walk

Target's success heavily relies on blending its physical and digital presence. Its store-fulfilled delivery services are highly efficient but place immense pressure on in-store operations and margins. The key challenge is optimizing this model without sacrificing the customer experience or profitability.

- Drive-Up & Order Pickup: High convenience, but strains store labor.

- Shipt (Same-Day Delivery): Key differentiator, yet costly to scale and operate.

- Digital Sales Growth: Essential for relevance, but often carries lower margins than in-store purchases.

- Inventory Accuracy: The backbone of the entire system, requiring significant tech investment.

'The American consumer is bifurcating. While high-income shoppers continue to spend, the middle-income demographic that forms Target's core is increasingly price-sensitive. Their ability to manage this value perception will define the next two years.' - Wall Street Retail Analyst

The Unseen Risks Lurking in the Aisles

Beyond macroeconomic trends, specific operational risks could derail Target's stability. These threats range from competitive encroachment to internal execution missteps, requiring vigilant management and strategic foresight to mitigate.

| Risk Category | Probability | Potential Impact |

|---|---|---|

| Consumer Shift to Essentials | High | Moderate |

| Inventory Mismanagement | Medium | High |

| Digital Competition (Amazon/Shein) | High | Medium |

| Supply Chain Disruption | Low | High |

DIFF Insight: The highest probability risk remains the consumer trade-down, but the most severe risk is a repeat of inventory mismanagement. The 2022 inventory glut severely damaged profitability, and while lessons have been learned, a miscalculation on seasonal or discretionary trends could quickly erase margin gains. This highlights the fragility of the recent recovery and the critical importance of predictive analytics in their merchandising strategy.

Can Private Labels Propel Future Growth?

With consumers tightening their belts, Target's extensive portfolio of owned brands like Good & Gather and Cat & Jack becomes a crucial strategic asset. These brands offer higher margins and build store loyalty, providing a partial shield against the downturn in national brand sales. Expanding these exclusive offerings is one of the clearest paths to defending profitability.

| Fiscal Year | Dividends Paid (Approx.) | Share Repurchases (Est.) | Strategic Capex |

|---|---|---|---|

| 2024 | ~ $2.0B | ~ $2.5B | Store Remodels |

| 2025 (Proj.) | ~ $2.1B | ~ $2.0B | Supply Chain Tech |

| 2026 (Proj.) | ~ $2.2B | ~ $2.0B | Digital Experience |

DIFF Insight: Target's capital allocation clearly prioritizes direct shareholder returns through consistent dividends and buybacks. While capex is present, it's focused on maintenance and optimization (remodels, tech) rather than aggressive expansion. This signals a mature company focused on efficiency and rewarding investors, acknowledging the reality of a slower-growth phase.