The Closed-Loop Fortress: A Moat Built on Data and Trust

American Express operates a fundamentally different model than its peers. By acting as both the card issuer and the network operator, it maintains direct relationships with cardholders and merchants. This creates a powerful, self-reinforcing ecosystem.

This structure grants a proprietary data advantage, allowing for superior credit risk assessment and highly targeted marketing. It's a key differentiator that competitors find nearly impossible to replicate, solidifying its market position among affluent consumers.

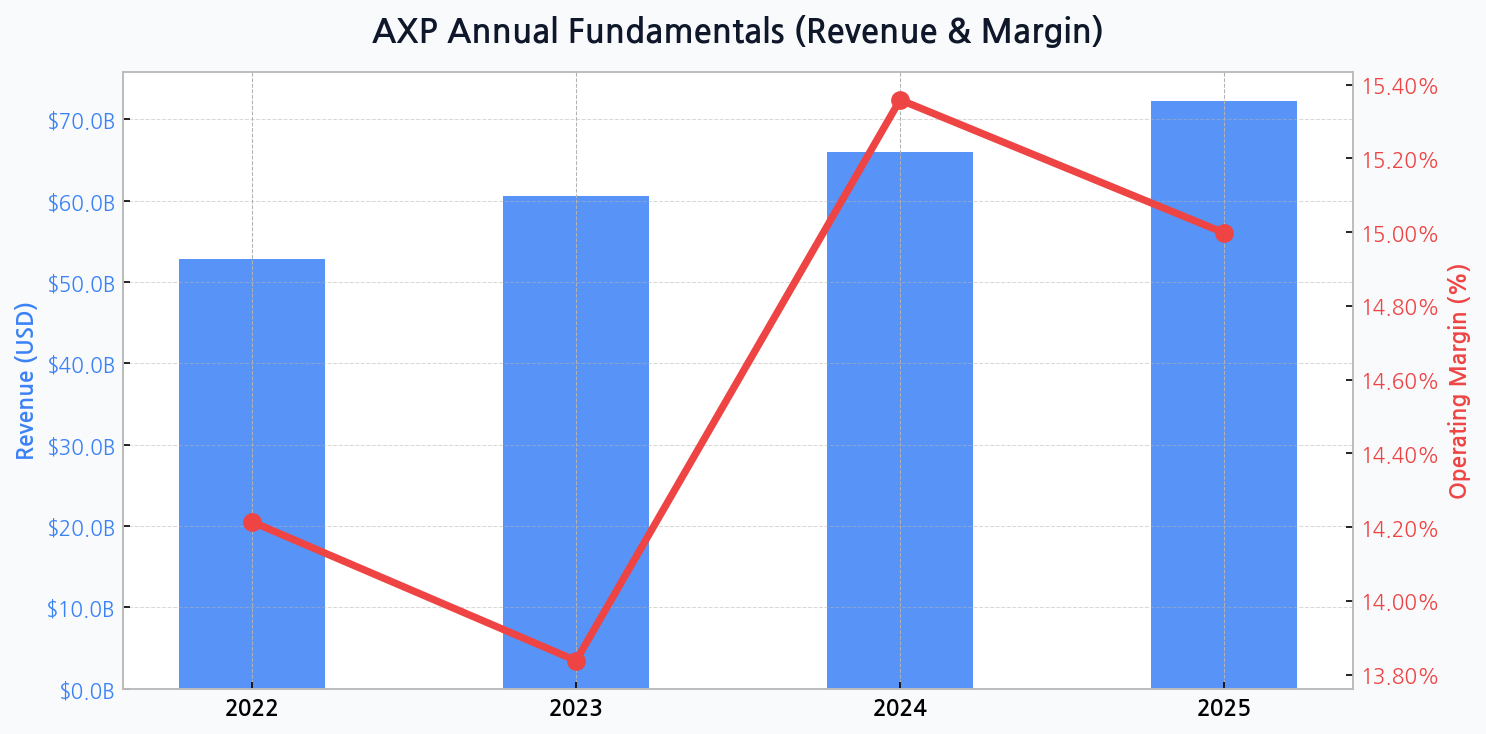

Decoding the Revenue and Margin Trajectory

The company's top-line performance demonstrates consistent strength. Revenue grew from $52.9 billion in 2022 to $60.5 billion in 2023 and is projected to reach $65.9 billion in 2024. This upward march reflects the resilience of its target demographic.

However, profitability has been more dynamic. The operating margin saw a dip from 14.2% in 2022 to 13.8% in 2023, likely due to increased investment in rewards and services, before rebounding sharply to an expected 15.4% in 2024.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for AXP

[Chart] American Express's projected revenue growth continues its steady climb, while operating margins are expected to stabilize around the 15% mark after a volatile period.

The High-Stakes Game of Premium Clientele

AXP's strategy is laser-focused on the premium segment, a cohort less susceptible to minor economic fluctuations. This focus on premium consumer spending underpins the stability of its revenue streams and allows for higher discount rates charged to merchants.

| Company | Business Model | Primary Moat | Target Audience |

|---|---|---|---|

| American Express | Closed-Loop | Data & Brand | High-Net-Worth |

| Visa Inc. | Open-Loop | Network Scale | Mass Market |

| Mastercard | Open-Loop | Network Scale | Mass Market |

DIFF Insight: While Visa and Mastercard dominate through sheer transaction volume, Amex's closed-loop model creates a 'quality over quantity' moat. This allows for higher per-transaction revenue and deeper customer insights, but also concentrates its risk within a specific economic segment. This strategic trade-off is central to understanding its valuation and performance.

A Balance Sheet Walking a Tightrope

As a financial services institution, AXP's balance sheet carries significant leverage. Total assets are projected to grow to $300.1 billion by 2025, but the debt ratio remains consistently high, hovering around 89%. While typical for the sector, this high leverage demands disciplined risk management, especially in a rising interest rate environment.

"Our focus on premium customers is not just a marketing strategy; it's a core risk management principle. Their financial resilience provides a buffer during periods of economic uncertainty, allowing us to invest for the long term." - Wall Street Analyst Commentary

Capital Allocation: Rewarding the Patient Shareholder

American Express has a long history of returning capital to shareholders through dividends and buybacks. This reflects a mature business model with strong, predictable cash flows and confidence from management in the company's long-term earnings power. This capital return discipline is a key attraction for long-term investors.

| Metric | American Express (AXP) | Visa (V) | Mastercard (MA) |

|---|---|---|---|

| Forward P/E Ratio | ~ 19x | ~ 28x | ~ 32x |

| Price/Book Ratio | ~ 6.2x | ~ 12.5x | ~ 50x |

| Dividend Yield | ~ 1.0% | ~ 0.7% | ~ 0.6% |

DIFF Insight: AXP trades at a notable valuation discount to its open-loop peers. This reflects the market's pricing of its higher credit risk exposure and slower overall transaction growth potential. However, for investors who believe in the durability of the premium consumer, this discount could represent a significant opportunity.

Looming Macroeconomic Headwinds

Despite its strengths, AXP is not immune to systemic shocks. A severe global recession could eventually impact even high-income spending, leading to slower growth and increased loan-loss provisions. The company's future success hinges on its ability to navigate these external pressures.

- Regulatory Scrutiny: Increased oversight on credit card fees could pressure a key revenue source.

- Competitive Landscape: Fintech innovators and 'Buy Now, Pay Later' services continue to challenge traditional payment models.

- Recessionary Risk: A prolonged economic downturn could impact travel and entertainment spending, a core AXP category.