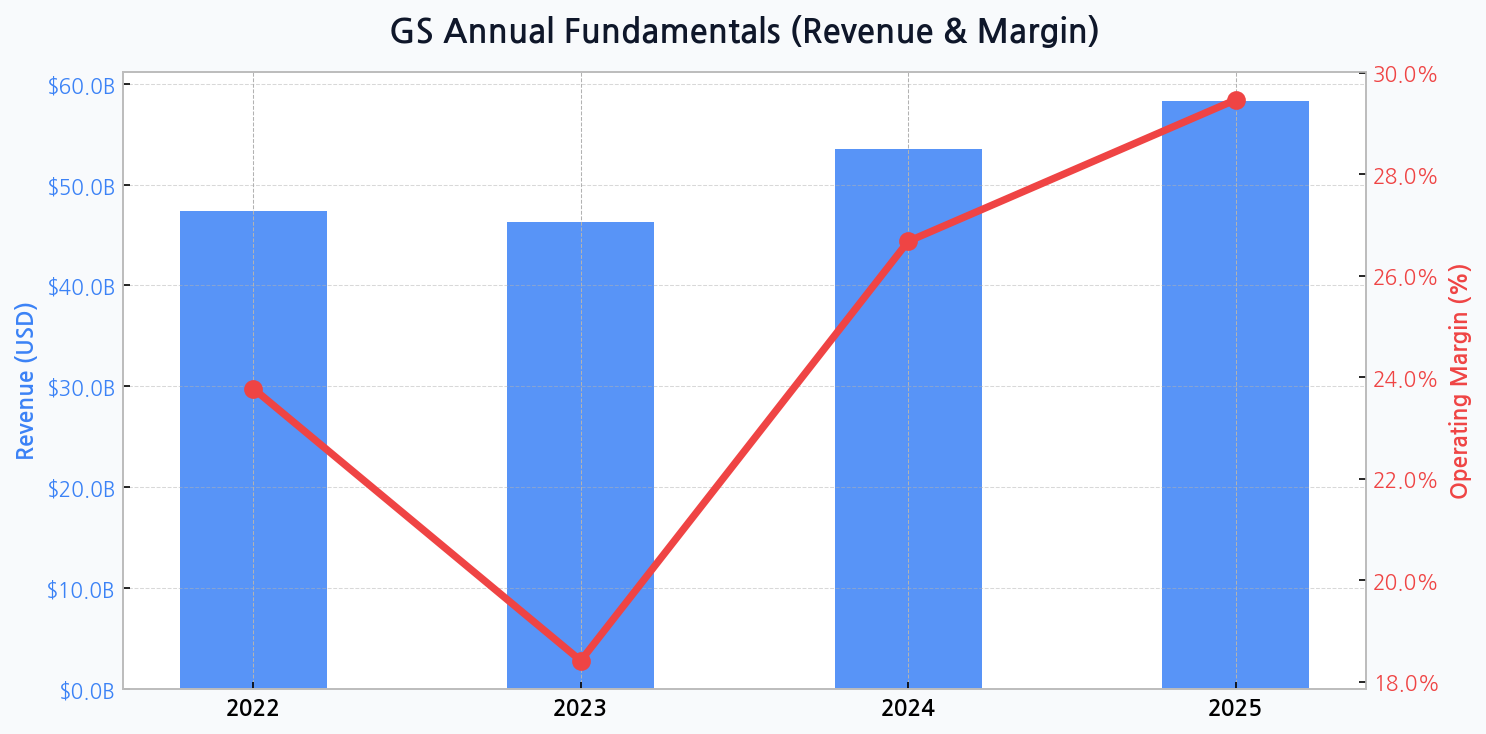

Profitability's V-Shaped Rebound from the 2023 Trough

After a challenging 2023 that saw revenue dip to $46.3 billion and operating margins compress to 18.4%, Goldman Sachs is poised for a formidable recovery. Projections indicate a powerful resurgence, with revenue expected to climb to $58.3 billion and margins expanding to a robust 29.5% by 2025, signaling a return to peak operational efficiency.

The Engine of Recovery: Capital Markets Unleashed

The firm's fortunes are a direct reflection of capital market vibrancy. The anticipated upswing in M&A advisory and underwriting services is the primary catalyst for this optimistic forecast. As global economies stabilize, the pent-up demand for deal-making is set to unlock significant fee-based revenue streams for the bank.

The cyclicality of investment banking is its defining feature. While downturns are painful, the subsequent rebounds are often swift and powerful, rewarding firms that have maintained their core franchise strength. GS is a textbook example of this dynamic.

Leveraging a Recovering Market: The Double-Edged Sword

While poised for growth, the firm's balance sheet warrants scrutiny. Total assets are projected to grow to $1.81 trillion by 2025, but the debt ratio remains consistently high, hovering around 93%. This high leverage amplifies returns in a bull market but represents a substantial risk if macroeconomic conditions unexpectedly deteriorate.

Maintaining this delicate balance sheet equilibrium is paramount. The expansion of the asset base must be managed with extreme prejudice to avoid systemic shocks. The firm's ability to navigate this high-wire act will define its success in the coming cycle.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for GS

The Arena: A Battle of Wall Street Titans

Goldman Sachs does not operate in a vacuum. It faces intense competition from other universal banks that have more diversified and stable revenue streams, such as large consumer banking divisions. This structural difference impacts valuation and risk profiles across the sector.

| Metric | Goldman Sachs (GS) | Morgan Stanley (MS) | JPMorgan Chase (JPM) |

|---|---|---|---|

| Primary Focus | Investment Banking, Trading | Wealth Management, IB | Universal Banking |

| Market Sensitivity | Very High | High | Moderate |

| Revenue Stability | Low | Medium | High |

DIFF Insight: The table highlights GS's specialized, high-beta model compared to its peers. While this leads to greater volatility, it also provides superior upside during strong capital market cycles. JPMorgan's diversified model provides a resilient floor, but GS's model offers a higher ceiling, making it a more aggressive play on economic recovery.

Can Asset & Wealth Management Provide a Stable Ballast?

A key strategic priority for GS has been the expansion of its Asset & Wealth Management division. This segment offers more predictable, fee-based revenues that can cushion the blow from volatile trading and investment banking results. Growing this business is crucial for reducing the firm's overall earnings volatility and earning a higher valuation multiple from the market.

Valuation Scenarios Tied to Deal Flow

The firm's stock performance is highly correlated with the outlook for M&A and IPO activity. Investors are pricing in a recovery, but the magnitude of that recovery remains a key variable. The path of interest rates and corporate confidence will dictate whether the bull or bear scenario plays out.

| Scenario | Core Trigger | Margin Impact | Potential Outcome |

|---|---|---|---|

| Bull Case | Sustained M&A Boom | Exceeds 30% | Significant Outperformance |

| Base Case | Gradual Market Recovery | Reaches ~ 29% | Moderate Upside |

| Bear Case | Economic Stagflation | Drops Below 20% | Sharp Correction |

DIFF Insight: This scenario analysis underscores the operational leverage inherent in Goldman's business model. A relatively modest change in the macroeconomic environment, particularly in corporate deal-making sentiment, can have an outsized impact on profitability and, consequently, its stock price. This makes timing and cycle awareness critical for investors.

Strategic Imperatives for Sustained Growth

To capitalize on the coming cycle, management must focus on several key areas. The firm's fate is inextricably linked to the health of global capital markets, but proactive strategy can mitigate risks and enhance returns. Executing on these priorities is non-negotiable for long-term value creation.

- Fortify the balance sheet by optimizing risk-weighted assets.

- Aggressively gain market share in advisory and underwriting as deal flow returns.

- Continue the strategic shift towards more stable, fee-generating businesses like wealth management.

- Invest in technology to enhance trading efficiency and client platforms.

Capital Allocation: Rewarding Shareholders in an Upswing

With profitability set to surge, the focus will turn to capital return. The firm must balance shareholder-friendly actions like buybacks and dividends with the need to retain capital for growth and regulatory requirements. This strategy hinges on disciplined risk management to ensure returns are not pursued at the expense of stability.

| Priority | Action | Strategic Rationale |

|---|---|---|

| 1. Reinvestment | Fund organic growth | Capture market share in core franchises |

| 2. Dividends | Sustainable increases | Signal confidence in earnings stability |

| 3. Share Buybacks | Opportunistic execution | Enhance EPS and return excess capital |

DIFF Insight: Goldman's capital allocation strategy reflects a classic cyclical playbook: fund growth aggressively during the upswing while returning capital to shareholders as a sign of financial strength. The emphasis on 'opportunistic' buybacks suggests management will be sensitive to the stock's valuation, aiming to repurchase shares when they believe they are intrinsically undervalued, maximizing shareholder value.