The Unassailable Digital Ledger: Intuit's Core Moat

Intuit's dominance isn't just about software; it's about embedding its products into the very fabric of small business and personal finance. Platforms like QuickBooks and TurboTax create a powerful lock-in effect, making switching costs prohibitively high for its millions of users. This creates a predictable, recurring revenue stream that is the envy of the software industry.

This foundation has allowed the company to build a remarkably sticky customer ecosystem. By controlling the primary financial ledger for businesses and individuals, Intuit establishes a data-rich platform upon which it can layer new, high-margin services, effectively turning customers into long-term subscribers rather than one-time buyers.

Strategic Acquisitions: Building an Impenetrable Ecosystem

| Acquired Company | Year | Deal Value (Approx.) | Strategic Goal |

|---|---|---|---|

| Credit Karma | 2020 | $8.1B | Expand into consumer finance & data |

| Mailchimp | 2021 | $12.0B | Integrate marketing tools for SMBs |

| TSheets | 2017 | $340M | Enhance payroll & time tracking features |

| Mint.com | 2009 | $170M | Entry into personal finance management |

DIFF Insight: These acquisitions are not random bets; they represent a calculated strategy to build a comprehensive 'financial operating system'. By acquiring Credit Karma, Intuit gained access to a massive trove of consumer credit data, creating cross-selling opportunities with TurboTax and Mint. The Mailchimp purchase aims to bundle marketing automation directly into the QuickBooks ecosystem, making it indispensable for small businesses seeking growth.

Fueling Growth with Debt: A Double-Edged Sword

This aggressive expansion is not without cost. The company's financial health reveals a clear trend: while total assets are projected to grow from $27.7B in 2022 to $37.0B in 2025, the debt ratio is simultaneously climbing from 40.7% to a concerning 46.7%. This indicates that the M&A-led growth is heavily reliant on leverage, a strategy that could become a significant vulnerability in a rising interest rate environment.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for INTU

While the market has rewarded this aggressive acquisition strategy so far, investors must monitor the company's ability to generate sufficient cash flow to service this growing debt burden. The success of these large-scale integrations is now paramount to justifying the financial risks undertaken.

The Profitability Paradox: Scaling at What Cost?

"Intuit's margin expansion is impressive, but it masks the immense integration challenges ahead. The true test will be whether they can merge these disparate company cultures and tech stacks without stifling the innovation that made each acquisition valuable in the first place."

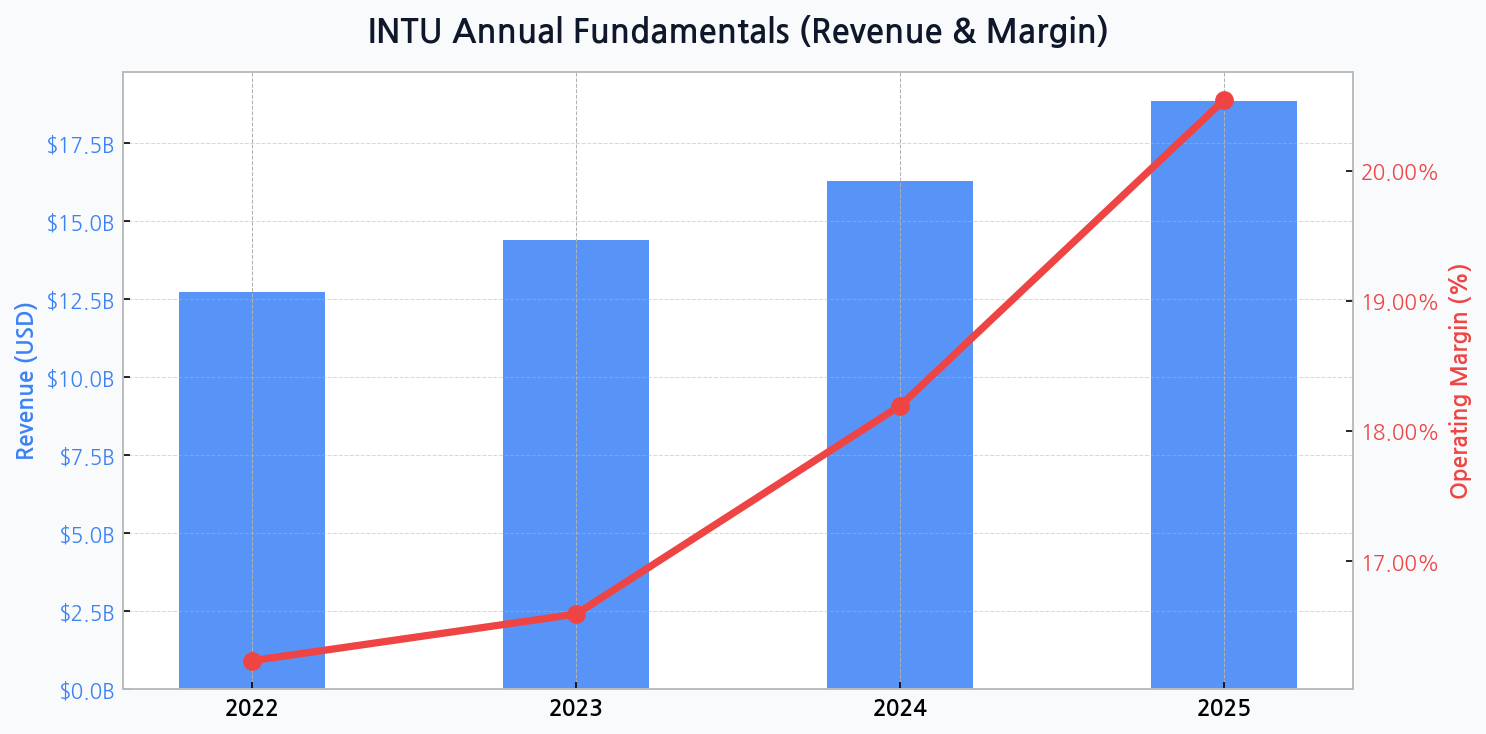

On the surface, the numbers are stellar. Revenue is on a steep upward trajectory, forecasted to hit $18.8B by 2025, up from $12.7B in 2022. Concurrently, operating margin is expected to expand from 16.2% to a robust 20.5%. This demonstrates strong pricing power and operational leverage, but the qualitative risks of managing such a sprawling empire cannot be ignored.

Mapping the Competitive Landscape

| Company | Core Product | Primary Market | Competitive Angle |

|---|---|---|---|

| Intuit (INTU) | QuickBooks / TurboTax | SMBs & Consumers (US) | Integrated Ecosystem / Brand Trust |

| Xero (XRO.AX) | Xero Accounting | SMBs (Global) | Cloud-Native / API-Friendly |

| Sage Group (SGE.L) | Sage Business Cloud | SMBs (Europe) | Strong Regional Presence |

| H&R Block (HRB) | Tax Preparation | Consumers (US) | Physical + Digital Hybrid Model |

DIFF Insight: While competitors exist, none possess Intuit's comprehensive, integrated ecosystem in the crucial US market. Xero is a formidable cloud-native competitor globally but lacks the deep entrenchment of QuickBooks in North America. H&R Block remains a key rival in tax preparation but does not offer the broader suite of small business tools, highlighting Intuit's unique and defensible market position.

Regulatory Crosshairs on a Software Behemoth

As Intuit's empire expands, so does the attention from regulators. The sheer dominance in tax software and small business accounting raises questions about fair competition and consumer choice. These looming regulatory threats could manifest in several ways:

- Antitrust investigations into past and future acquisitions.

- Mandates to open its ecosystem to third-party competitors.

- Scrutiny over its 'free file' tax programs and upselling tactics.

- Data privacy concerns related to the consolidation of financial data from multiple platforms.

Valuation Under a Microscope: Is the Premium Justified?

| Metric | Intuit (INTU) | Peer Average (SaaS) | S&P 500 Average |

|---|---|---|---|

| Forward P/E Ratio | ~ 35x | ~ 28x | ~ 19x |

| Price/Sales (P/S) Ratio | ~ 8x | ~ 6x | ~ 2.5x |

| EV/EBITDA | ~ 27x | ~ 20x | ~ 14x |

DIFF Insight: Intuit consistently trades at a significant premium to both the broader market and its software-as-a-service (SaaS) peers. This premium is justified by its powerful moat, high margins, and predictable revenue. However, it also means the stock is priced for perfection, leaving little room for error in executing its M&A integration or navigating potential economic downturns.

Final Verdict on the Ecosystem Strategy

Intuit is successfully transitioning from a provider of siloed software products to the central nervous system for its customers' financial lives. This strategy is unlocking immense value and creating a formidable competitive barrier. However, the associated financial leverage and regulatory risks are undeniable, creating a high-stakes balancing act for management.