The DBS Engine Sputters Under Margin Pressure

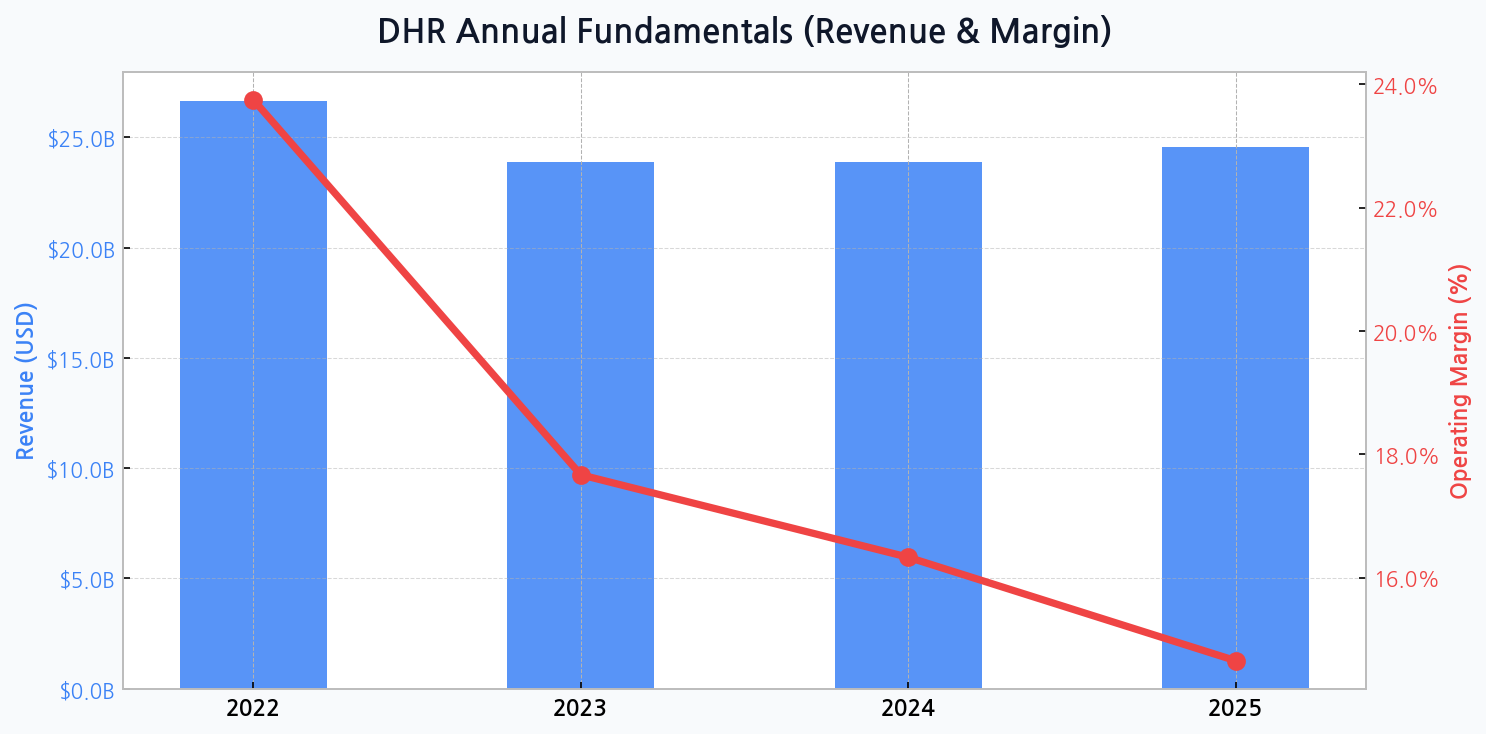

Danaher's operational prowess, long celebrated through its Danaher Business System (DBS), is facing a stark reality check. The company's revenue stream is stabilizing, moving from $26.6B in 2022 to a projected $24.6B by 2025, but this masks a more concerning trend. The operating margin is on a sharp descent, contracting from a healthy 23.8% in 2022 to a forecasted 14.7% in 2025, signaling significant cost pressures and a challenging post-pandemic normalization.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for DHR

Revisiting the M&A Playbook: A History of Value Creation

Danaher's identity is inextricably linked to its role as a serial acquirer. The DBS philosophy is designed to integrate new businesses and extract synergies efficiently. Examining past acquisitions provides a blueprint for how the company might navigate its current challenges and deploy capital for future growth.

| Acquisition Target | Year | Value (Approx.) | Strategic Goal |

|---|---|---|---|

| Pall Corporation | 2015 | $13.8B | Expansion into Filtration & Life Sciences |

| Cepheid | 2016 | $4.0B | Strengthening Molecular Diagnostics |

| IDT | 2018 | $2.1B | Genomics Consumables Leadership |

| GE Biopharma | 2020 | $21.4B | Dominance in Bioprocessing (Cytiva) |

DIFF Insight: This track record demonstrates a clear strategy of acquiring market leaders in high-growth, high-margin sectors within life sciences and diagnostics. The success of these integrations, particularly the massive GE Biopharma deal, underpins investor confidence in Danaher's model. However, the scale of future deals required to move the needle is now substantially larger, increasing execution risk.

A Financial Fortress Built on Prudence

Despite the margin headwinds, Danaher's financial health remains a key pillar of strength. The company has skillfully managed its balance sheet, with the debt ratio improving from 40.6% in 2022 to a projected 37.0% by 2025. This disciplined capital allocation provides a substantial war chest for acquisitions without over-leveraging, a critical advantage in a volatile market.

"The core question for Danaher is not whether DBS works, but whether it can work fast enough to offset the margin dilution from both macroeconomic factors and the sheer scale of its recent integrations. The market is pricing in perfection, but the reality is far more complex."

Gauging the Headwinds: A Matrix of Threats

While the long-term strategy appears sound, several immediate risks threaten Danaher's trajectory. These challenges range from geopolitical tensions impacting supply chains to the persistent effects of inflation on its cost structure, demanding proactive mitigation from leadership.

| Risk Factor | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Sustained Margin Erosion | High | High | DBS-led cost optimization, pricing power |

| M&A Integration Failure | Medium | High | Phased integration, strong leadership |

| Geopolitical Supply Chain Risk | Medium | Medium | Supplier diversification, regionalization |

| Biotech Funding Slowdown | High | Medium | Focus on large pharma clients, diagnostics |

DIFF Insight: The most immediate and probable threat is the continued margin decline, which directly impacts profitability and valuation. While M&A integration risk is always present, the slowdown in biotech funding could dampen demand for Danaher's high-margin consumables and equipment. This highlights the company's sensitivity to the broader health of the life sciences R&D ecosystem.

Unlocking Future Value: Strategic Levers

To counteract current pressures and reignite growth, Danaher must focus on several key strategic imperatives. The company's future performance will depend on its ability to execute across these domains, leveraging its core operational excellence philosophy.

- Portfolio Optimization: Divesting slower-growth or lower-margin assets to sharpen focus on core platforms like bioprocessing and genomics.

- Innovation in Diagnostics: Capitalizing on the installed base of Cepheid systems to drive recurring revenue from high-value testing menus.

- Geographic Expansion: Deepening penetration in high-growth emerging markets, particularly in Asia-Pacific, for life sciences tools.

- Strategic Capital Deployment: Executing bolt-on acquisitions in adjacent technologies while maintaining balance sheet discipline.

Valuation Crossroads: Justifying the Premium

Danaher has historically traded at a premium to its peers, a testament to its consistent execution and the perceived strength of the DBS model. With a current PBR of 2.58, the market still bakes in high expectations for future performance and capital allocation.

| Metric | Danaher (DHR) | Peer Average (Life Sciences) | S&P 500 Average |

|---|---|---|---|

| P/E Ratio (Forward) | ~ 25x | ~ 22x | ~ 19x |

| P/B Ratio | 2.58x | ~ 3.5x | ~ 4.0x |

| EV/EBITDA | ~ 18x | ~ 16x | ~ 14x |

DIFF Insight: While Danaher's P/B ratio appears reasonable compared to the broader market, its forward P/E and EV/EBITDA multiples indicate a persistent premium over its direct competitors. This valuation is contingent on the company reversing its margin decline and proving its M&A strategy can continue to deliver superior returns. Any faltering in execution could lead to a significant multiple contraction.

The Investor's Dilemma

Investors are caught between Danaher's stellar long-term track record and the undeniable short-term pressures on its core profitability metrics. The central debate is whether the current challenges are a temporary cyclical downturn or the beginning of a structural shift that tests the limits of the DBS model itself.