The Razor & Blade Model Perfected in Modern Medicine

Intuitive Surgical's strategy isn't merely selling advanced surgical robots; it's about creating an entire ecosystem. The initial sale of a da Vinci system is just the beginning. The true long-term value is captured through the continuous sale of high-margin proprietary instruments, accessories, and service contracts, a classic and highly effective recurring revenue model.

An Unbreachable Competitive Moat

The company has constructed a formidable barrier to entry, locking hospitals and surgeons into its platform. This is not just about patents, but a deeply integrated network of training, data, and a massive installed base that makes switching to a competitor an expensive and disruptive proposition for any healthcare provider.

| Competitive Factor | Intuitive Surgical (ISRG) | Emerging Competitors |

|---|---|---|

| Installed Base | Dominant Global Presence | Niche or Regional Focus |

| Surgeon Training | Decades of Standardized Curricula | Building from Scratch |

| Data & Analytics | Vast Procedural Data Lake | Limited Data Sets |

| Patent Portfolio | Extensive and Layered | Targeted but Narrower |

DIFF Insight: The table highlights that ISRG's true defense lies not in a single factor, but in the synergistic effect of its entire ecosystem. Competitors can replicate individual features, but challenging the entrenched training paradigm and the vast data library is a multi-decade endeavor. This network effect significantly raises the cost and risk for hospitals considering alternative platforms.

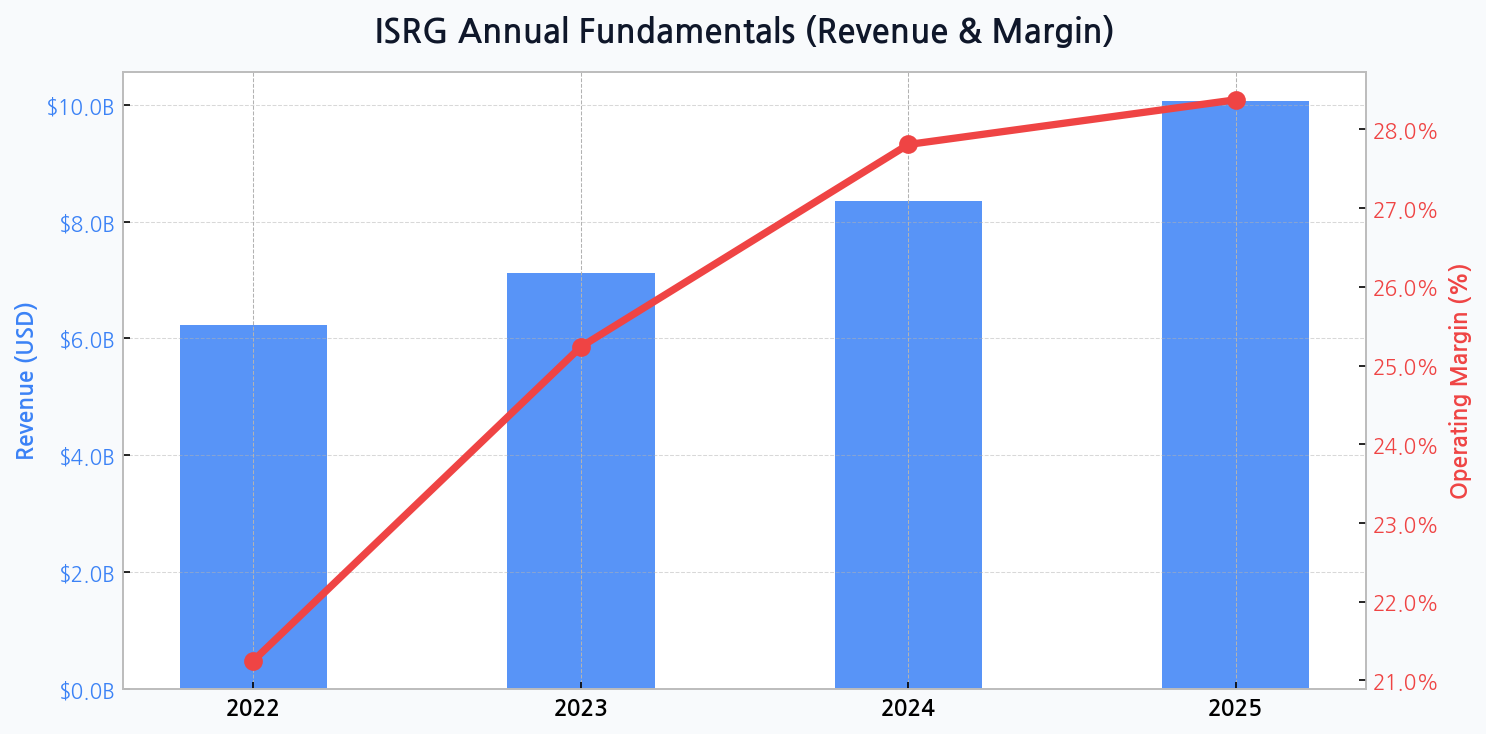

The Engine of Relentless Profitability

Financial projections underscore the power of this model. Revenue is on a powerful upward trajectory, growing from $6.2 billion in 2022 to an anticipated $10.1 billion by 2025. More impressively, this growth is increasingly profitable, with operating margins expanding from a solid 21.3% to a robust 28.4% over the same period, showcasing exceptional operating leverage.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for ISRG

This chart visualizes the powerful dual-engine growth of both top-line revenue and bottom-line profitability. The steady margin expansion demonstrates management's ability to scale operations efficiently while maintaining pricing power, a core tenet of a market leader.

A Fortress-Like Balance Sheet

This aggressive growth is not fueled by risky debt. The company's financial health is pristine, with total assets projected to swell from $13.0 billion to $20.5 billion by 2025. Simultaneously, the debt ratio remains remarkably low and controlled, declining from 14.3% in 2022 to a projected 12.3% in 2025, providing immense flexibility for future R&D investment or strategic acquisitions.

Navigating the Shadows of Competition and Regulation

Despite its dominance, ISRG is not without threats. The landscape is changing as patents expire and well-funded competitors enter the market. The primary risk is not a direct technological defeat, but a gradual erosion of pricing power as hospitals gain more leverage with viable alternatives, creating a long-term margin compression scenario.

| Risk Category | Probability | Potential Impact |

|---|---|---|

| New Competitor Pressure | High | Moderate-to-High |

| Regulatory Scrutiny | Medium | Moderate |

| Hospital Capex Cycles | Medium | High |

| Procedure Volume Slowdown | Low | High |

DIFF Insight: While competition is the most discussed risk, the true 'black swan' event would be a significant, prolonged downturn in hospital capital expenditure cycles. A recessionary environment could force healthcare systems to delay multi-million dollar system purchases, directly impacting ISRG's system placement growth, which is a leading indicator for future recurring revenue.

The Next Frontier: Data, AI, and Untapped Markets

The next decade for Intuitive won't be about just placing more robots; it will be about making each robot smarter. The real value lies in leveraging their unparalleled procedural data to create AI-driven insights that improve surgical outcomes. That's a moat that software, not just hardware, will build.

The Price of Perfection: A Stretched Valuation

The market is well aware of Intuitive's strengths, and this is reflected in its premium valuation. The company consistently trades at multiples significantly higher than the broader med-tech industry. This creates a situation where the stock is priced for perfection, leaving little room for error and making it vulnerable to sell-offs on any hint of slowing growth or eroding market share.

| Metric | ISRG (Current TTM) | Med-Tech Peer Average | ISRG 5-Year Average |

|---|---|---|---|

| Forward P/E Ratio | ~ 60x | ~ 28x | ~ 55x |

| Price / Sales Ratio | ~ 18x | ~ 6x | ~ 19x |

| EV / EBITDA | ~ 45x | ~ 20x | ~ 42x |

DIFF Insight: The data clearly shows that investors are paying a significant premium for ISRG's quality and growth. While its current valuation is roughly in line with its own historical average, it is more than double its peer group. This indicates that the market has already priced in several years of strong execution, setting a very high bar for future performance.

Final Strategic Verdict

- The recurring revenue from instruments and services remains the company's crown jewel, providing stability and high-margin cash flow.

- The deep integration into surgical training programs creates a powerful, sticky customer base that is difficult for new entrants to disrupt.

- While fundamentally sound, the stock's high valuation remains its greatest vulnerability, requiring flawless execution to justify its premium.

- Future growth catalysts will likely shift from system placements to data-driven software solutions and international market penetration.