The Unyielding Grip of the Cystic Fibrosis Monopoly

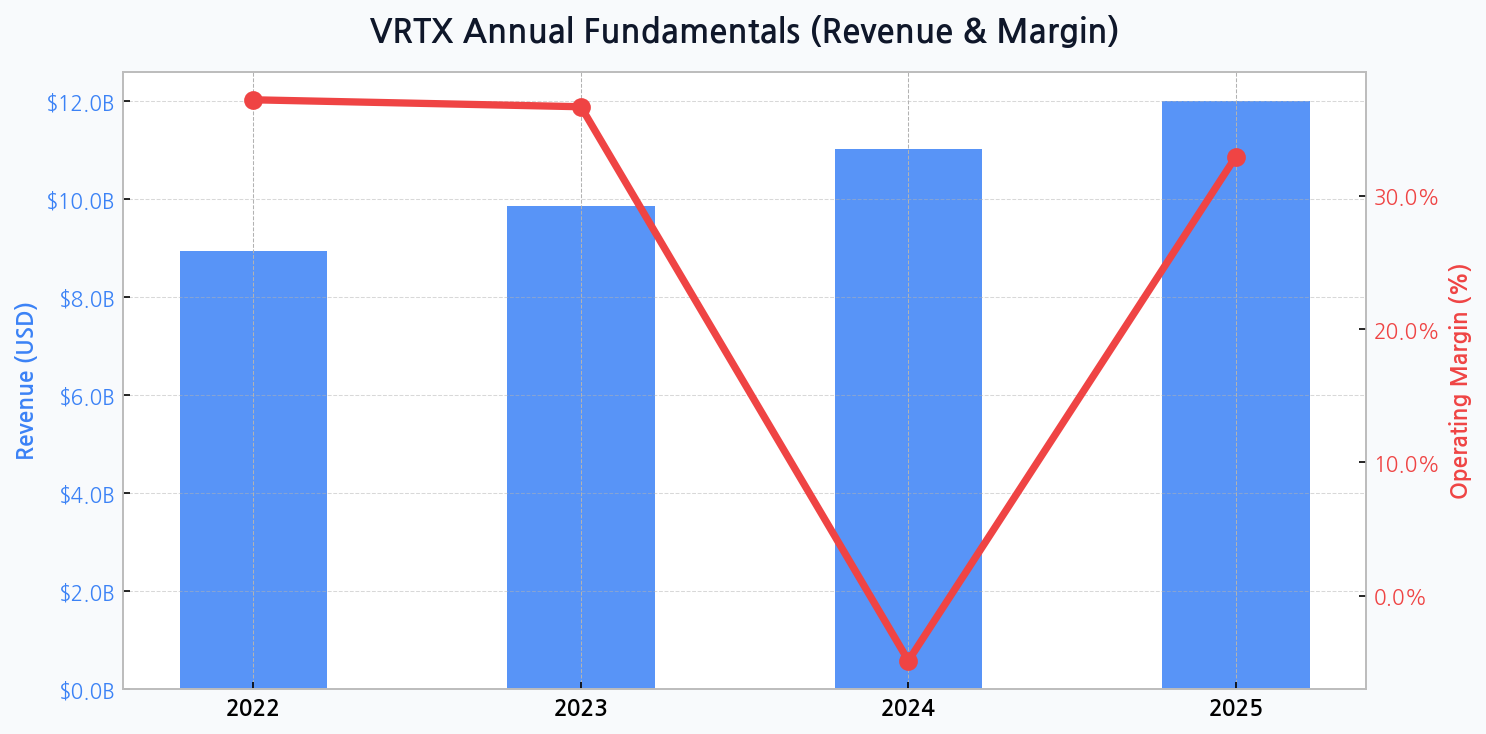

Vertex has constructed an unparalleled economic moat in the cystic fibrosis (CF) market. This dominance is not merely a market-leading position; it is a near-total capture of the patient population, translating directly into formidable financial strength. The company's revenue trajectory reflects this power, climbing steadily from $8.9 billion in 2022 to an estimated $9.9 billion in 2023, showcasing consistent growth fueled by its core franchise.

Navigating the Cost of Innovation

The strategic roadmap, however, points toward a future beyond CF. This ambition carries a significant price tag, reflected in the jarring 2024 financial projections. Despite anticipated revenue growth to $11.0 billion, the operating margin is forecast to plummet to a staggering -4.9%. This isn't a sign of a failing core business but rather a testament to the colossal investment in R&D and commercial launch infrastructure for its new wave of therapies, a calculated bet on future growth engines.

| Therapy Area | Lead Candidate | Therapeutic Approach | Potential Market Impact |

|---|---|---|---|

| Sickle Cell / Beta Thalassemia | Casgevy (exa-cel) | CRISPR Gene-Editing | First-in-class curative potential |

| Acute & Neuropathic Pain | VX-548 | Selective NaV1.8 Inhibitor | Non-opioid alternative |

| Type 1 Diabetes | VX-880 / VX-264 | Stem Cell-Derived Islets | Functional cure potential |

DIFF Insight: This pipeline table illustrates a deliberate and aggressive diversification strategy. Moving into areas like pain management and diabetes represents a quantum leap from its CF comfort zone. The success of Casgevy is a critical proof-of-concept for its gene-editing platform, but the real long-term value lies in scaling these technologies to address much larger patient populations, a feat that is far from guaranteed and requires flawless execution.

The Financial Fortitude Fueling the Future

Vertex's balance sheet appears well-equipped to weather this period of heavy investment. Total assets are projected to grow from $18.2 billion in 2022 to $25.6 billion by 2025. Crucially, the company maintains a conservative leverage profile, with its debt ratio remaining manageable, hovering between 22.7% and 27.2% through this period. This financial stability provides the necessary runway to absorb the near-term margin shock and fund its ambitious, multi-billion-dollar R&D programs without jeopardizing its core operations.

The market is rewarding Vertex for its vision, not its current profitability. Investors are underwriting a multi-year transformation, but their patience will be tested by the immense execution risk tied to commercializing cell and gene therapies at scale.

A Valuation Premium Built on Future Promises

Vertex commands a premium valuation, a clear indicator that investors are pricing in the success of its pipeline. The company's narrative is less about its present-day CF dominance and more about its potential to disrupt entirely new therapeutic areas. This forward-looking sentiment justifies its high multiples but also exposes the stock to significant volatility should any of its key pipeline assets face clinical or regulatory setbacks. The monopolistic cash generation from CF provides a floor, but the ceiling is defined by speculative, high-growth assets.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for VRTX

[Chart] The chart visualizes Vertex's projected revenue growth against its highly volatile operating margin, highlighting the 2024 investment trough before a projected recovery in 2025.

The Strategic Crossroads of Growth and Risk

The company's strategy is a high-wire act. While the CF franchise provides a safety net of predictable cash flow, the leap into gene-editing and cell therapy is fraught with challenges. These are not simple pills but complex, high-cost treatments with logistical and reimbursement hurdles. The anticipated margin recovery to 32.9% in 2025 on $12.0 billion in revenue hinges entirely on the successful and efficient launch of these next-generation products, a critical test of the company's operational capabilities.

- Core Investment Thesis: Leverage the CF cash cow to fund a pivot to potentially curative therapies in new, larger markets.

- Primary Risk Factor: Execution risk in commercializing complex gene and cell therapies, alongside potential regulatory delays.

- Key Monitorable: The adoption rate and pricing of Casgevy and the clinical progress of VX-548 in pain management.

Mapping the Competitive and Regulatory Gauntlet

As Vertex expands, it enters crowded and fiercely competitive fields. Unlike the near-monopoly it enjoys in CF, the pain and diabetes markets are populated by established pharmaceutical giants. Success will require not just clinical superiority but also a sophisticated commercial strategy. This transition represents a fundamental shift in the company's competitive posture and a significant test of its pipeline execution risk.

| Risk Category | Description | Impact Level | Mitigation Strategy |

|---|---|---|---|

| Pipeline Failure | Key late-stage assets fail to meet endpoints. | High | Diversified pipeline across multiple modalities. |

| Reimbursement Hurdles | Payers balk at high upfront costs of gene therapies. | High | Outcomes-based pricing models and robust health-economic data. |

| Competitive Pressure | Larger players enter the non-opioid pain market. | Medium | Aim for best-in-class clinical profile to secure market access. |

DIFF Insight: This matrix underscores that Vertex's risks are evolving from defending a monopoly to launching products in highly contested arenas. The shift to addressing reimbursement challenges for curative therapies is particularly critical. A failure to convince payers of the long-term value of a one-time treatment like Casgevy could severely cap its long-term earnings power and serve as a negative precedent for the rest of the pipeline.