The Indispensable Tollbooth of Chip Miniaturization

Lam Research operates not merely as a supplier but as a foundational pillar for the entire semiconductor industry. Its dominance in etch and deposition technology makes it a technological gatekeeper for any company seeking to produce advanced logic and memory chips. This commanding position is the source of its resilient business model, even amidst market volatility.

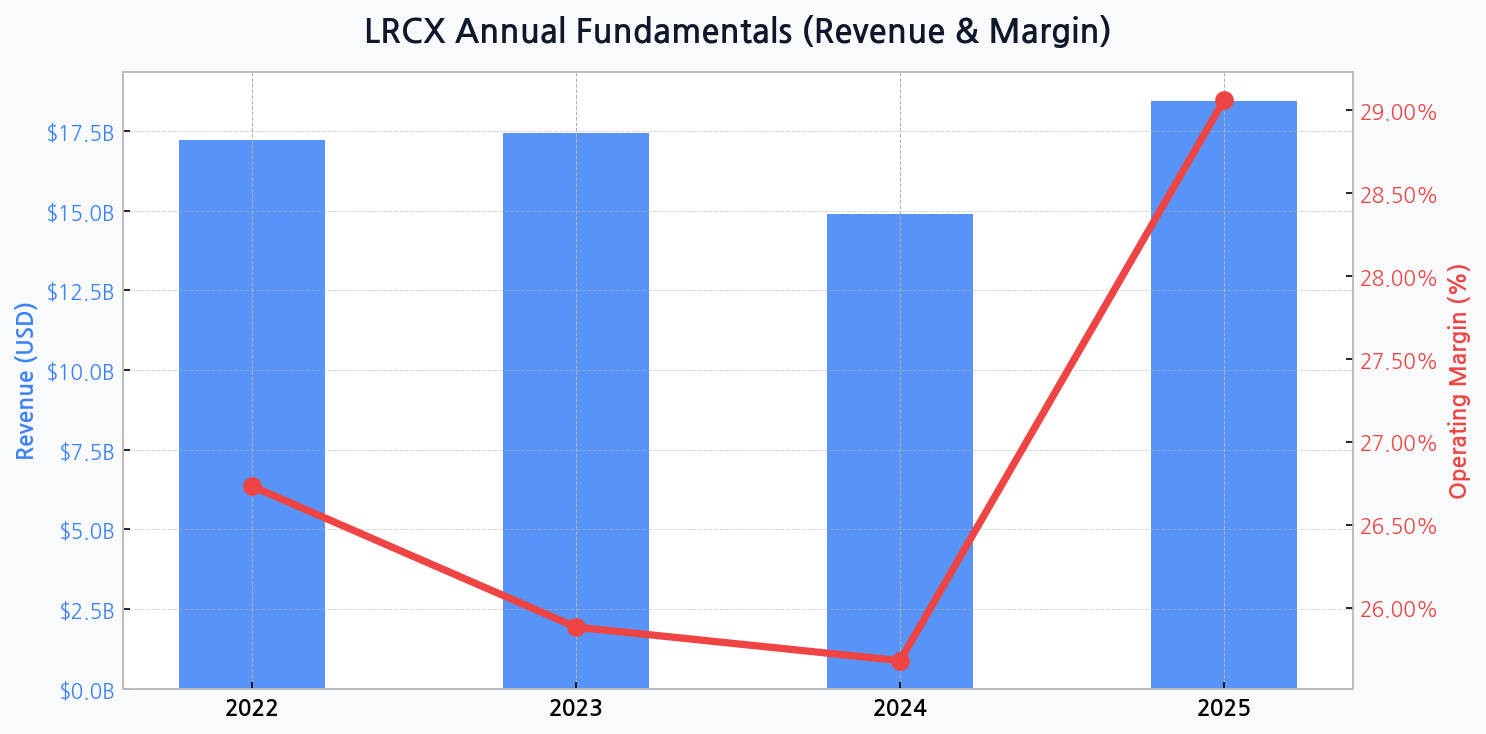

Navigating the Memory Cycle's Ebb and Flow

The company's financials reflect its deep ties to the notoriously cyclical memory market. After achieving revenues of $17.2 billion in 2022 and a slight increase to $17.4 billion in 2023, a significant industry downturn led to a projected revenue dip to $14.9 billion in 2024. However, this is expected to be a temporary trough, with a powerful recovery to $18.4 billion forecasted for 2025, signaling renewed investment from major memory producers.

| Company | Etch M/S | Deposition M/S | Core Focus |

|---|---|---|---|

| Lam Research | ~ 55% | ~ 20% | Memory (DRAM/NAND) |

| Applied Materials | ~ 20% | ~ 50% | Diversified (Logic/Foundry) |

| Tokyo Electron | ~ 25% | ~ 25% | Coater/Developer, Etch |

DIFF Insight: Lam's overwhelming share in the etch segment, particularly for 3D NAND and DRAM, creates a deep-seated dependency from memory giants like Samsung and SK Hynix. While Applied Materials leads in deposition, Lam's specialization in etch for high-aspect-ratio structures provides a more concentrated, defensible moat. This specialization, however, also explains its heightened sensitivity to the memory sector's investment cycles compared to its more diversified peers.

A Fortress Balance Sheet Forged in Volatility

Despite revenue fluctuations, Lam's management has demonstrated exceptional capital expenditure discipline. This is evident in the steady improvement of its financial health. The company's total assets are projected to grow from $17.2 billion in 2022 to $21.3 billion by 2025, while its debt ratio is on a clear downward trajectory, declining from 63.5% to a more robust 53.8% over the same period. This strengthening financial foundation provides the stability needed to weather downturns and invest aggressively during upswings.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for LRCX

The Margin Story: From Resilience to Expansion

Profitability reveals a similar narrative of resilience and future growth. The operating margin saw a slight compression from 26.7% in 2022 to 25.7% in 2024, a testament to its pricing power during a market contraction. The most compelling figure is the projected leap in operating margin to 29.1% in 2025, suggesting that the upcoming recovery will be accompanied by significant operational leverage and enhanced profitability, likely driven by demand for higher-margin, cutting-edge equipment.

The primary risk isn't Lam's technology, which is world-class. It's geopolitics. Every restriction on technology exports to China chips away at a significant portion of the total addressable market, forcing a strategic realignment that carries both execution risk and margin pressure.

The AI Supercycle: A New Demand Catalyst

The insatiable demand for AI processing power is creating a structural tailwind. The rise of High-Bandwidth Memory (HBM) and Gate-All-Around (GAA) transistor architectures requires fundamentally new and more precise etch and deposition steps. This shift toward next-generation logic and memory-stacking technologies plays directly into Lam's core competencies, positioning it as a prime beneficiary of the massive capital investments flowing into AI infrastructure.

| Threat | Probability | Potential Impact |

|---|---|---|

| Memory Market Downturn | Medium | High |

| Geopolitical Trade Curbs | High | Medium-High |

| Competitor Innovation | Low | Medium |

| Supply Chain Disruption | Medium | Medium |

DIFF Insight: While the memory cycle is a well-understood operational risk, the most unpredictable and potent threat comes from geopolitics. U.S. export controls on advanced semiconductor equipment to China directly impact Lam's revenue potential. The company's long-term growth trajectory will depend heavily on its ability to navigate these complex regulations and pivot its sales focus toward other high-growth regions.

Core Investment Merits

- Unrivaled market leadership in the critical etch segment.

- Direct beneficiary of long-term secular growth trends in AI, 5G, and IoT.

- Consistently improving balance sheet with a declining debt profile.

- Strong projected rebound in both revenue and operating margin for 2025.

- Proven ability to return capital to shareholders through dividends and buybacks.