The Enduring Reign and Looming Threat to Eylea

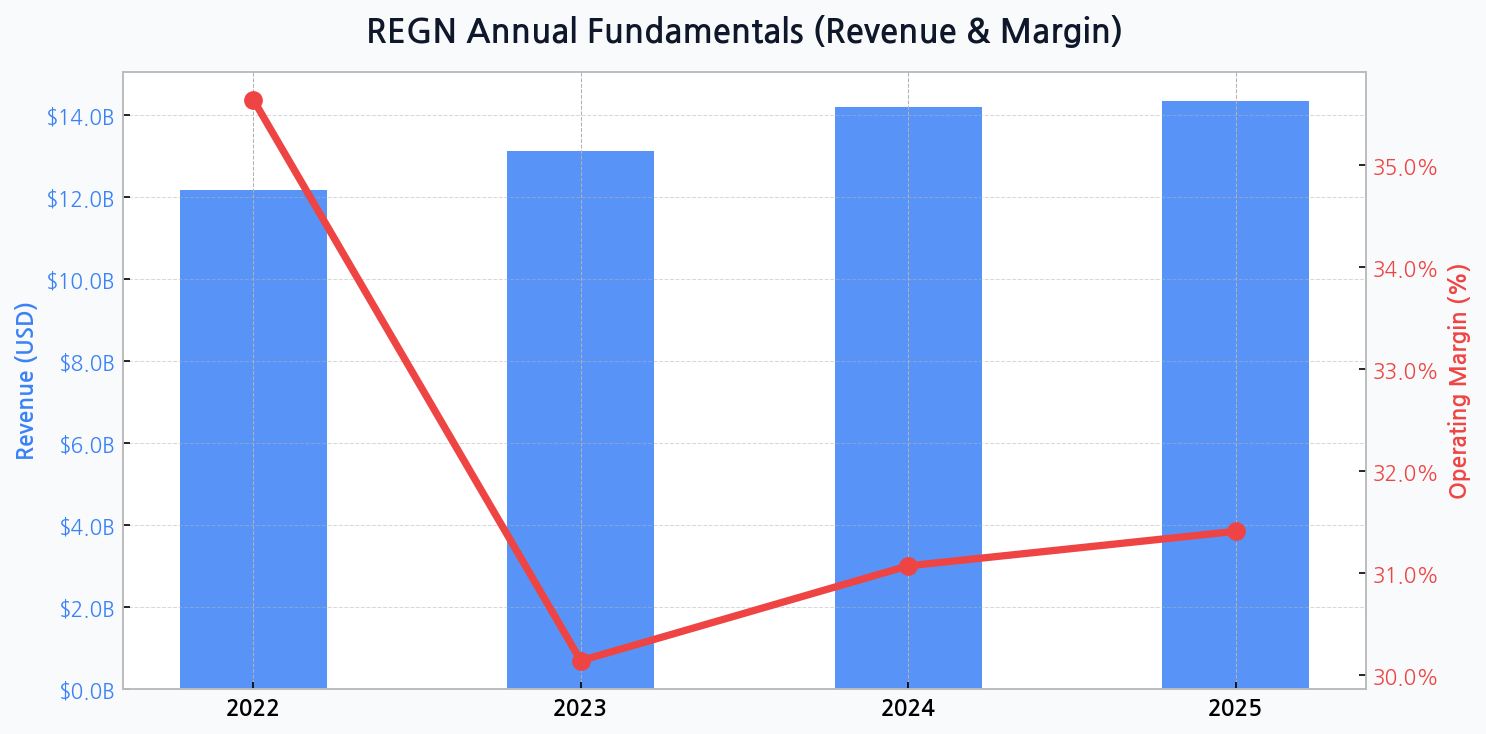

Regeneron's financial narrative has long been dominated by Eylea, its blockbuster treatment for retinal diseases. This single product has been an immense cash generator, anchoring the company's performance, as seen in its contribution to the strong $12.2B revenue in 2022. However, the approaching Eylea's patent cliff casts a long shadow, forcing a strategic pivot.

Margin Contraction Amidst Strategic Reinvestment

While revenue is projected to grow steadily toward $14.3B by 2025, the operating margin reveals a more complex story. The significant drop from a high of 35.6% in 2022 to an estimated 30.1% in 2023 signals increased R&D spending and marketing costs to defend its franchise and launch new products, a necessary but costly phase of its evolution.

| Product | Therapeutic Area | Strategic Importance | Growth Driver |

|---|---|---|---|

| Eylea / Eylea HD | Ophthalmology | Legacy Cash Cow | Market Share Defense |

| Dupixent | Immunology | Primary Growth Engine | Indication Expansion |

| Libtayo | Oncology | Diversification Play | Combination Therapies |

| Pipeline Assets | Various | Future Value | R&D Success |

DIFF Insight: This breakdown highlights the critical transition underway. While Eylea remains the foundation, its role is shifting from a growth driver to a source of funding for Dupixent's aggressive expansion and the broader oncology pipeline. The company's future valuation hinges on how successfully Dupixent can offset the inevitable decline of its predecessor.

The Sanofi Alliance: A Symbiotic Lifeline

The collaboration with Sanofi is the central pillar of Regeneron's growth strategy. Dupixent, a co-developed drug, has become a mega-blockbuster in its own right, treating a range of inflammatory conditions. This partnership provides not only a vital revenue stream but also shared development costs, amplifying the impact of R&D investment.

The greatest challenge for a pharmaceutical giant is not discovering a blockbuster, but successfully replacing it. Regeneron's fate is now inextricably linked to its ability to manage this succession from Eylea to its next generation of therapies.

A Balance Sheet Fortified for the Future

Regeneron's financial health provides the necessary firepower for its strategic ambitions. Total assets are projected to expand from $29.2B in 2022 to over $40.6B by 2025. Crucially, this growth is managed with impressive capital allocation discipline, as the debt ratio is expected to remain stable, hovering between 21.5% and 22.9%, ensuring flexibility for potential acquisitions or further R&D investment.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for REGN

Unlocking Value from the Pipeline

Beyond the established products, long-term success depends entirely on the R&D pipeline. These strategic diversification efforts are aimed at creating new revenue pillars in oncology, immunology, and rare diseases, reducing the company's historical over-reliance on a single therapeutic area. The market is closely watching for clinical trial data that can validate this next chapter.

| Candidate | Target Indication | Development Phase | Est. Peak Sales Potential |

|---|---|---|---|

| Fianlimab (LAG-3) | Melanoma | Phase 3 | High |

| Itepekimab (IL-33) | COPD | Phase 3 | High |

| Garetosmab (Activin A) | FOP | Filed | Moderate |

| Pozelimab (C5) | CD55 Deficiency | Approved | Niche |

DIFF Insight: The pipeline shows a clear strategy of pursuing both large market opportunities like COPD and melanoma, alongside targeted therapies for rare diseases. Success in even one of the high-potential Phase 3 trials could significantly alter the company's growth trajectory and investor sentiment. However, the risk of late-stage failure remains a constant threat to this model.

Navigating Competitive and Regulatory Headwinds

The path forward is not without peril. The introduction of biosimilars for Eylea is an inevitability, and pricing pressures from governments and insurers are intensifying across the industry. Navigating this landscape requires not just scientific innovation but also astute commercial and legal strategy.

- Monitor Eylea HD uptake as a primary defense against biosimilar erosion.

- Track Dupixent's label expansion into new indications, particularly COPD.

- Evaluate the clinical trial results for key pipeline assets like fianlimab.

- Assess capital deployment strategies, including potential bolt-on acquisitions.

| Threat | Probability | Potential Impact |

|---|---|---|

| Eylea Biosimilar Entry | High | Severe |

| Phase 3 Pipeline Failure | Medium | Severe |

| Increased Drug Price Regulation | High | Moderate |

| Dupixent Competition | Medium | High |

DIFF Insight: The matrix clearly shows that the most immediate and severe risks are directly tied to Regeneron's two main products. While regulatory risk is high, its impact is more gradual. A significant late-stage pipeline failure, however, could be a sudden, catastrophic event for the stock, highlighting the binary nature of biotech investing.