The End of an Era and a Costly New Beginning

Gilead Sciences stands at a critical juncture, transitioning from a company defined by its near-monopoly in HIV and HCV treatments to a diversified biopharma player. This strategic pivot into oncology and cell therapy is not a choice but a necessity, driven by looming patent expirations and the need for new growth engines.

Deconstructing the Revenue Engine

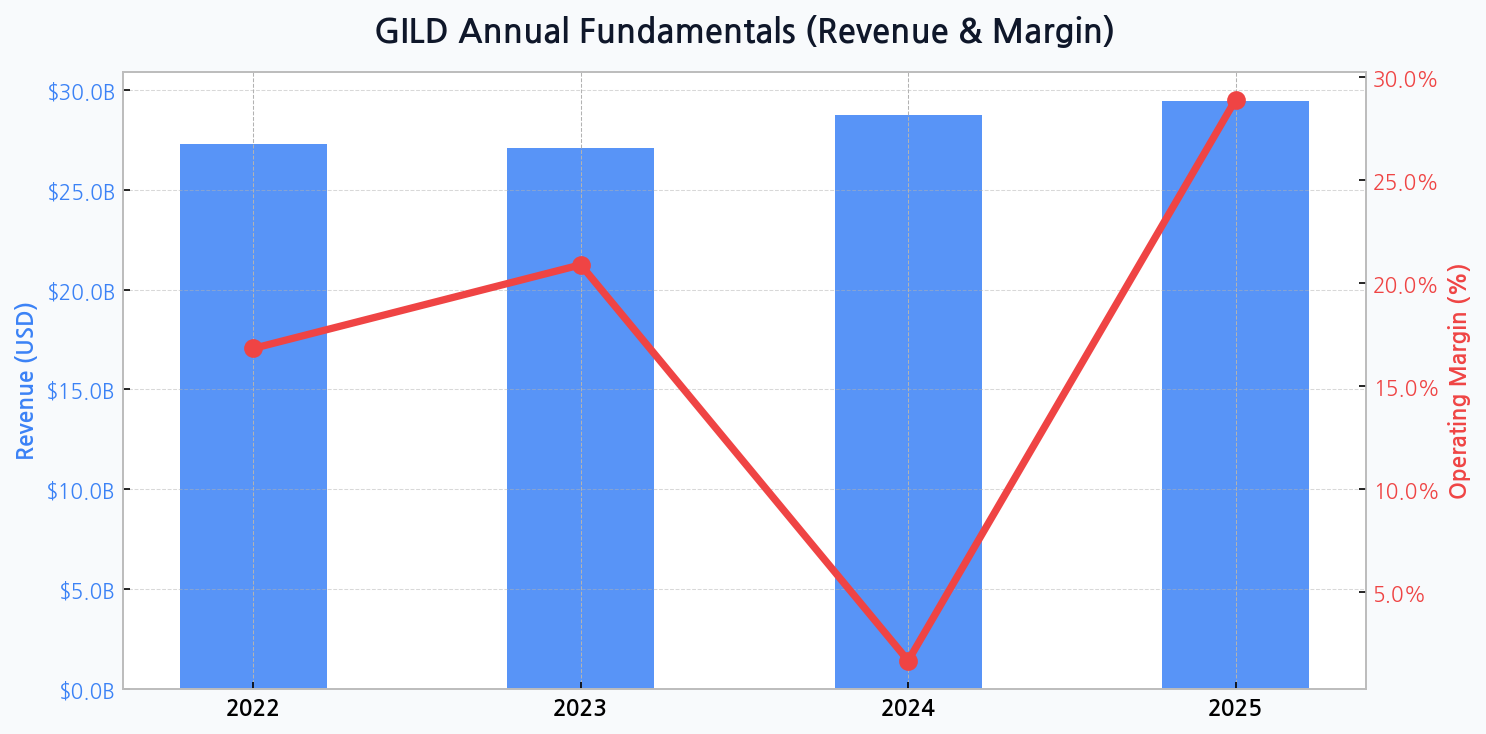

While the legacy antiviral franchise remains the financial bedrock, its growth is maturing. The company's 2022 revenue of $27.3 billion was heavily reliant on this segment. However, the recent growth in the oncology portfolio, led by key acquisitions, signals a deliberate and aggressive shift in focus.

| Business Segment | Primary Drivers | Strategic Importance | Growth Outlook |

|---|---|---|---|

| HIV Franchise | Biktarvy, Descovy | Cash Cow / Funding Engine | Stable to Moderate |

| Oncology | Trodelvy, Yescarta | Primary Growth Driver | High Growth |

| Veklury (COVID-19) | Remdesivir | Windfall Revenue | Declining |

| Liver Disease | HCV Portfolio | Legacy / Mature | Declining |

DIFF Insight: The table highlights a fundamental tension within Gilead. The stable HIV cash cow funds the high-risk, high-reward oncology venture. The rapid decline of Veklury revenue post-pandemic has amplified the pressure on the oncology pipeline to deliver tangible results sooner rather than later, making its execution a make-or-break factor for the company.

The Price of Transformation: A Margin Rollercoaster

The financial strain of this transformation is starkly visible in the company's profitability. After posting a solid 20.9% operating margin on $27.1 billion in revenue in 2023, the forecast for 2024 reveals a dramatic plunge to just 1.7% on revenue of $28.8 billion. This collapse is a direct result of massive R&D spending and acquisition-related costs for building out the oncology pipeline. The market is betting on a sharp rebound, with 2025 margins projected to recover to 28.9% on $29.4 billion in revenue, assuming pipeline success.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for GILD

A Market Divided by Hope and Skepticism

The central debate for Gilead is whether it's buying expensive lottery tickets in oncology or building a sustainable new pillar of growth. The market has yet to fully price in the potential of the cell therapy pipeline, reflecting deep-seated skepticism about the company's ability to replicate its antiviral success in a fiercely competitive new field.

The Oncology Pipeline: Gilead's High-Stakes Bet

The company's future is inextricably linked to the success of a few key oncology assets. Trodelvy (for breast cancer) and the Kite Pharma cell therapies (Yescarta, Tecartus) are the cornerstones of this new strategy. Their performance and label expansions are under intense scrutiny as indicators of the pivot's viability.

| Asset | Therapeutic Area | Status | Market Potential |

|---|---|---|---|

| Trodelvy | Metastatic Breast Cancer | Approved / Expansion Trials | Blockbuster |

| Yescarta / Tecartus | CAR T-cell Therapy | Approved / Multiple Cancers | Niche to High Growth |

| Magrolimab | Myelodysplastic Syndromes | Clinical Hold / High Risk | Uncertain |

DIFF Insight: This pipeline represents a significant departure from Gilead's traditional small-molecule expertise, moving into complex biologics and cell therapies. While Trodelvy and Yescarta show promise, setbacks like the clinical hold on Magrolimab highlight the immense execution risk. Unlike the HIV market where Gilead set the rules, in oncology, it is a challenger facing established giants.

Core Strategic Imperatives

Gilead's long-term success rests on executing a multi-pronged strategy. These pillars are designed to balance the management of its legacy business with the aggressive pursuit of new frontiers.

- Aggressive Business Development: Continuously seeking bolt-on acquisitions and partnerships to bolster the oncology and immunology pipeline.

- Maximizing the HIV Franchise: Defending market share with next-generation treatments and lifecycle management to fund future growth.

- Operational Excellence in Cell Therapy: Scaling the complex manufacturing and logistics required for CAR T-cell therapies to establish a competitive moat.

Balance Sheet Under Pressure

This ambitious strategy has strained the balance sheet. Total assets are projected to decline from $63.2 billion in 2022 to $59.0 billion by 2024. More critically, the debt ratio spiked to 67.4% in 2024, a clear indicator of the capital-intensive nature of its M&A and R&D activities. While the ratio is expected to improve to 61.7% in 2025, sustained high leverage could limit future strategic flexibility.

Is Gilead Undervalued or a Value Trap?

Compared to peers, Gilead often trades at a discount, reflecting market uncertainty. Its valuation is caught between that of a mature, slow-growth pharmaceutical company and a high-growth biotech, creating a complex investment thesis. The successful execution of its oncology pipeline execution is the primary catalyst needed for a significant valuation re-rating.

| Company | Forward P/E Ratio | Primary Growth Area | Dividend Yield |

|---|---|---|---|

| Gilead (GILD) | ~ 10x | Oncology, Cell Therapy | ~ 4.5% |

| AbbVie (ABBV) | ~ 14x | Immunology, Aesthetics | ~ 3.8% |

| Merck (MRK) | ~ 15x | Oncology (Keytruda) | ~ 2.7% |

| Vertex (VRTX) | ~ 25x | Cystic Fibrosis, Gene Editing | N/A |

DIFF Insight: Gilead's low Forward P/E and high dividend yield suggest the market is valuing it more like a legacy pharma company (e.g., AbbVie) than a growth biotech (e.g., Vertex). This implies that the potential upside from its oncology pivot is not fully priced in, but it also reflects the significant risk. A key challenge is overcoming patent cliff pressures on its established drugs while investing heavily in unproven areas.

The Final Verdict on Gilead's Gamble

Gilead's transformation is a necessary but perilous journey. The extreme margin compression in 2024 is the painful cost of admission to the exclusive oncology club. The company's future trajectory will be defined by its strategic capital allocation and its ability to deliver clinical and commercial wins from its expensive pipeline. Investors are being paid a handsome dividend to wait, but the path ahead is fraught with volatility and execution risk.