The Great Pivot: From Unprofitable Growth to Sustainable Earnings

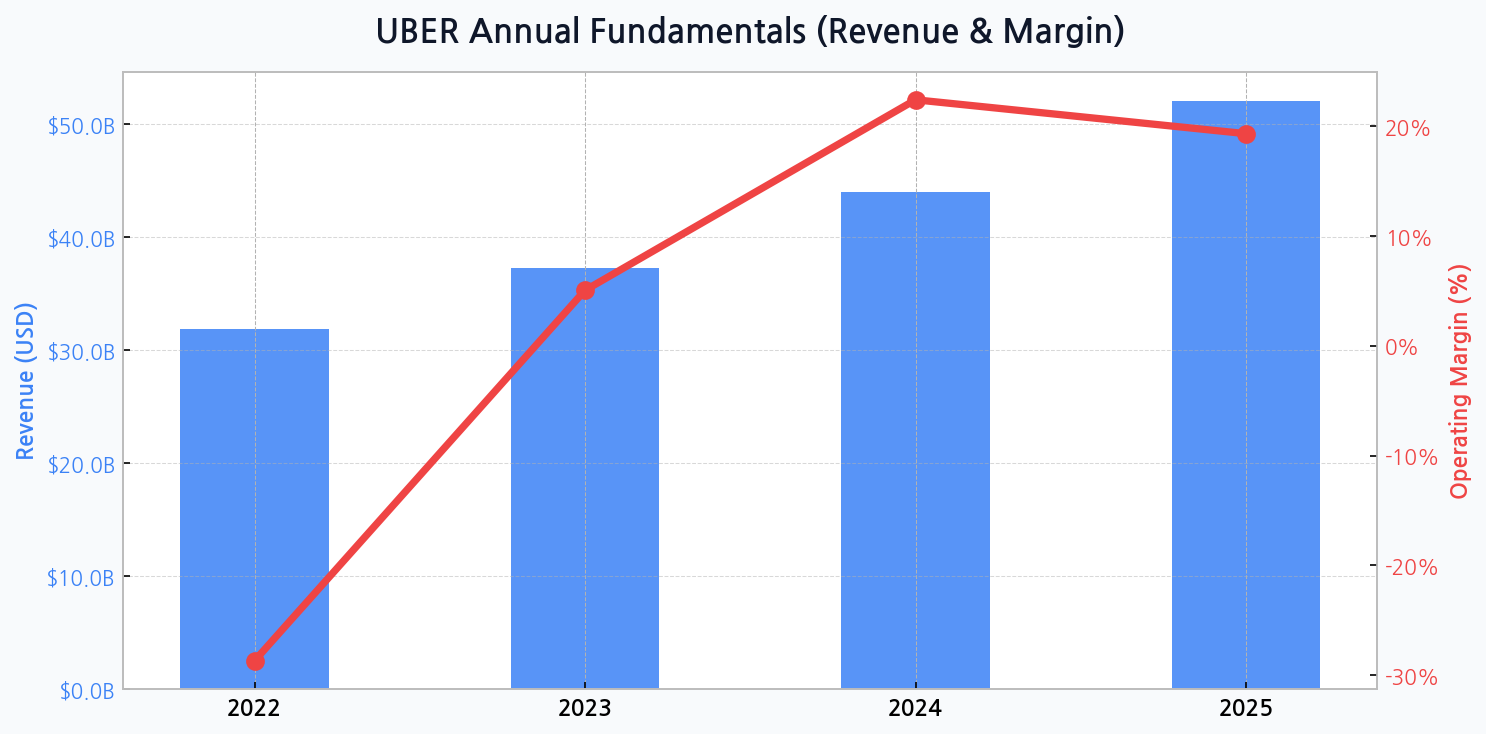

Uber's narrative has fundamentally shifted from a cash-burning startup to a disciplined global operator. The transformation is stark, with revenues climbing from $31.9 billion in 2022 to a projected $44.0 billion in 2024. More critically, the operating margin executed a stunning turnaround, flipping from a deeply negative -28.7% in 2022 to a positive 5.1% in 2023, showcasing a successful re-engineering of its cost structure.

This journey reflects a strategic maturation, prioritizing profitable trips over sheer volume. The projected margin of 22.4% for 2024 suggests this trend is not a fleeting anomaly but the new operational standard. This dramatic margin reversal is the cornerstone of the current investment thesis, proving the platform's ability to generate cash at scale.

Beyond the Ride: Diversifying Revenue Streams for Dominance

While ride-sharing remains the core, Uber's future is increasingly tied to its diversification into Delivery (Uber Eats) and Freight. These segments are crucial for capturing a larger share of consumer and enterprise logistics spending, creating a multifaceted mobility ecosystem.

| Business Segment | FY2023 Revenue Est. | Growth Driver | Market Position |

|---|---|---|---|

| Mobility (Rides) | $19.1B | Post-pandemic recovery, premium offerings | Market Leader |

| Delivery (Eats) | $12.2B | Grocery & retail expansion, subscriptions | Top Contender |

| Freight | $6.0B | Logistics tech adoption, market fragmentation | Emerging Challenger |

DIFF Insight: This table illustrates that while Mobility is the established cash cow, the Delivery segment is a powerful secondary engine with substantial room for growth in adjacent markets like grocery. Freight represents a high-potential, albeit more cyclical, venture that leverages Uber's logistics technology. The success of this trifecta is essential to de-risking the business from sole reliance on human transportation and fending off specialized competitors.

Forging an Unbreakable Network Effect Moat

Uber's primary competitive advantage is not its technology alone, but its deeply entrenched two-sided network. More drivers attract more riders, which in turn attracts more drivers, creating a virtuous cycle that is incredibly difficult and expensive for new entrants to replicate.

The scale of our network is a formidable barrier. Every new driver and every new user strengthens the platform for everyone else, reducing wait times and increasing earning potential. This is the core of our economic moat.

Deep Dive: This platform's network effect extends beyond just rides. It allows Uber to cross-promote services efficiently, converting ride-sharing users into Uber Eats customers at a much lower acquisition cost than competitors. This ecosystem synergy is a powerful, often underestimated, driver of long-term value.

Navigating the Financial Highway: A Balance Sheet in Transition

The company's financial health is visibly improving. Total assets are projected to grow robustly from $32.1 billion in 2022 to $61.8 billion by 2025. Concurrently, Uber is deleveraging its balance sheet, with the debt ratio expected to fall from a high of 73.5% to a more manageable 54.6% over the same period. This indicates a strategic shift towards building a more resilient financial foundation.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for UBER

[Chart] Uber's projected revenue growth and improving operating margin from 2022 to 2025, highlighting the company's successful pivot to profitability.

The Regulatory Gauntlet: A Perpetual Battle for Legitimacy

The most persistent threat to Uber's model is the regulatory minefield surrounding labor laws. The ongoing debate over classifying drivers as independent contractors versus employees poses a significant risk to its cost structure. A widespread shift towards employee status could fundamentally alter the unit economics of the business.

Deep Dive: Investors must price in this 'regulatory beta.' Any negative ruling in a major market like California or the EU could create a domino effect, forcing operational changes and potentially eroding margins. Proactive engagement with policymakers and the development of hybrid models will be critical for long-term stability.

Mapping the Competitive Landscape

While Uber holds a commanding position in many Western markets, the global mobility space is far from a monopoly. Regional champions and specialized delivery platforms present constant competitive pressure, forcing continuous innovation and price discipline.

| Company | Primary Market | Key Moat | Strategic Threat |

|---|---|---|---|

| Uber | Global (ex-China/SEA) | Network Scale, Brand | Regulatory Headwinds |

| Lyft | North America | Regional Focus | Lack of Diversification |

| DoorDash | North America (Delivery) | Restaurant Density | Intense Competition |

| Grab | Southeast Asia | Super-App Ecosystem | Regional Economic Swings |

DIFF Insight: The competitive analysis shows that Uber's global scale is its greatest asset but also exposes it to a wider array of risks. Unlike Lyft, its diversification into Delivery provides a hedge. However, it faces entrenched local leaders like Grab in key growth regions, meaning its 'winner-take-all' ambitions are geographically constrained and require a market-specific strategy rather than a monolithic global approach.

Deconstructing Uber's Valuation

With a market capitalization approaching $150 billion and a Price-to-Book (PBR) ratio of 5.49, the market is pricing in significant future growth and sustained profitability. This valuation is less about current earnings and more about the belief in Uber's potential to dominate the future of mobility and delivery logistics.

| Metric | Value | Interpretation |

|---|---|---|

| P/S (Forward) | ~ 3.0x | Reasonable for a tech-growth leader |

| P/E (Forward) | ~ 35x | Reflects high growth expectations |

| PBR | 5.49 | Premium for asset-light model |

DIFF Insight: The valuation hinges entirely on the successful execution of the profitability roadmap. The PBR of 5.49 is justifiable for a platform business with a strong brand and network effects, but it leaves little room for error. Any stumble in margin expansion or a significant regulatory setback could trigger a sharp re-rating of the stock, making it a high-reward but also a high-risk proposition.

The Final Destination: Scenarios for Long-Term Viability

Uber's long-term success depends on its ability to balance growth, profitability, and regulatory compliance. The path forward is not guaranteed, but the strategic direction appears sound. Key factors will determine its ultimate trajectory.

- Sustained Profitability: Continuing to optimize pricing, costs, and operational efficiency across all segments.

- Successful Diversification: Scaling Uber Eats and Freight into market-leading, profitable businesses.

- Regulatory Stability: Achieving a workable, long-term framework for driver classification in key markets.

- Technological Innovation: Maintaining a lead in logistics technology, autonomous driving partnerships, and platform features.