The Brand Premium Paradox

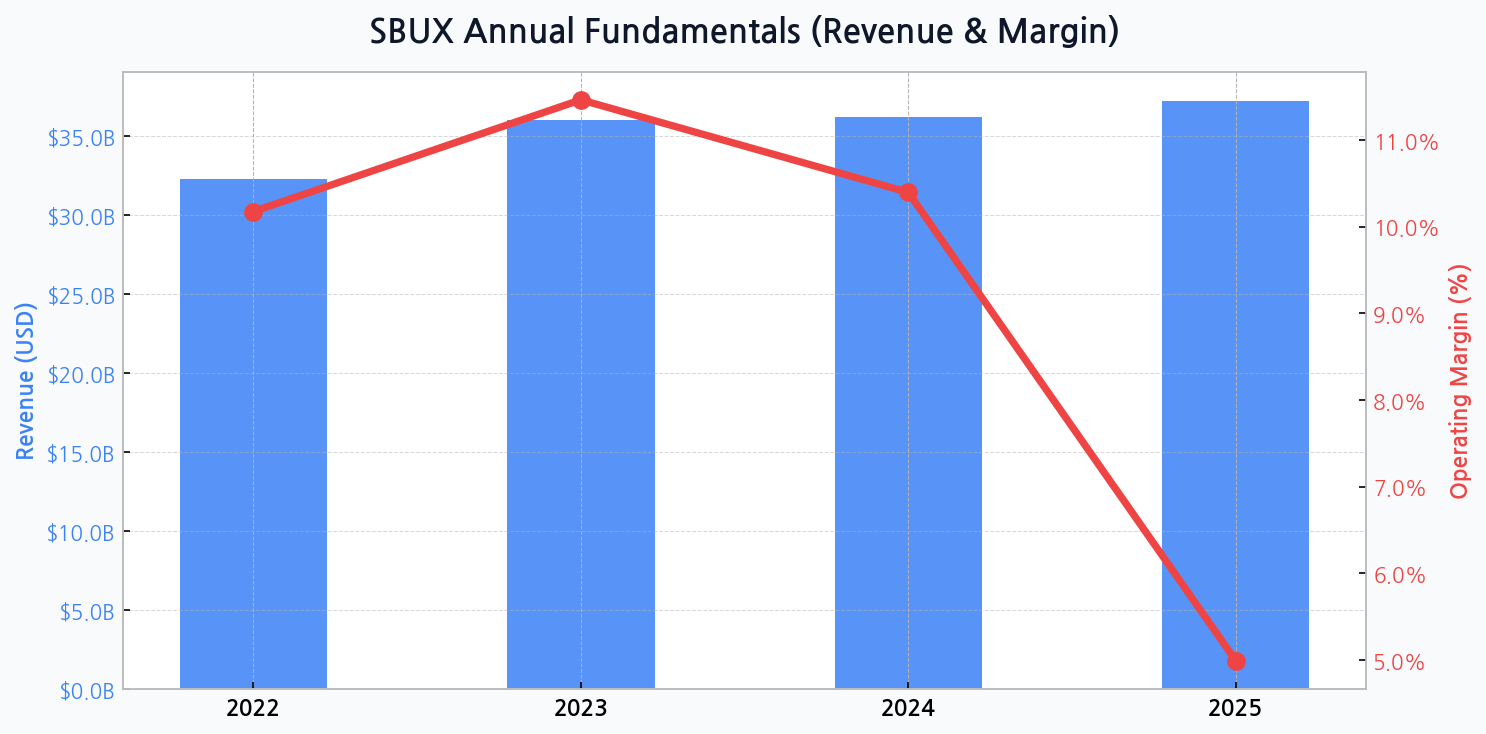

Starbucks' global brand recognition remains a formidable asset, yet it is failing to translate into bottom-line strength. While revenue is on a steady incline, climbing from $32.3B in 2022 to an anticipated $37.2B in 2025, the underlying financial narrative is one of distress. This growth is proving to be increasingly expensive and inefficient.

Is the Loyalty Moat Now a Millstone?

The Starbucks Rewards program has long been hailed as a key competitive advantage, creating a sticky customer base. However, this powerful engine is becoming a significant drag on profitability. The escalating costs of rewards and discounts contribute directly to the brand's eroding profit structure, forcing a re-evaluation of its long-term viability as a value creator versus a cost center.

| Region | FY2023 Revenue (Approx.) | Growth Driver | Primary Challenge |

|---|---|---|---|

| North America | ~ $26.5B | Loyalty Program & Beverage Innovation | Market Saturation & Labor Costs |

| International | ~ $7.5B | China Store Expansion | Geopolitical Tensions & Competition |

| Channel Development | ~ $2.0B | Ready-to-Drink Products | Shelf Space & Distribution Costs |

DIFF Insight: The table highlights a heavy reliance on the North American market, which is mature and facing margin headwinds. While International growth, particularly in China, is the strategic focus, it remains a smaller portion of revenue and is exposed to significant macroeconomic volatility, making it an unreliable pillar for future profitability.

The Alarming Collapse in Operating Margin

The most alarming trend is the dramatic compression of operating margins. After peaking at a healthy 11.5% in 2023, projections show a catastrophic fall to just 5.0% by 2025. This isn't a minor fluctuation; it's a fundamental breakdown in the company's ability to convert sales into profit, pointing to severe operational inefficiencies or intense competitive pressure.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for SBUX

A Balance Sheet Under Pressure

While total assets are projected to grow from $29.4B in 2023 to $32.0B in 2025, this expansion is financed with significant leverage. The debt ratio remains precariously high, hovering above 120% throughout the period. This level of debt limits financial flexibility and amplifies risk, especially as profitability falters and interest rates remain a concern.

The market is no longer rewarding top-line growth at any cost. Starbucks' plunging margin forecast reveals a business struggling with its own scale, where each new dollar of revenue is less profitable than the last. This is a classic symptom of operational decay.

Navigating a Minefield of Strategic Risks

The path forward for Starbucks is fraught with peril. The company must simultaneously manage domestic labor challenges, navigate a complex recovery in China, and innovate its menu without further cannibalizing margins. The digital ecosystem's dependency on promotions is a key vulnerability that competitors are beginning to exploit.

| Risk Factor | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| China Market Slowdown | High | Severe | Diversify international presence |

| Sustained Margin Erosion | High | Severe | Operational cost-cutting, pricing strategy |

| Labor Unionization | Medium | Moderate | Improved employee compensation & benefits |

| Competitive Intensity | High | Moderate | Product innovation & brand marketing |

DIFF Insight: The matrix underscores that Starbucks' primary threats are not just competitive but deeply structural. The high probability and severe impact of both a China slowdown and continued margin erosion suggest the company's current growth strategy is fundamentally unstable and highly susceptible to external shocks, demanding a pivot toward efficiency.

The Valuation Question

Given the deteriorating fundamentals, Starbucks' valuation multiples require close scrutiny. Investors must question whether the current stock price adequately reflects the heightened risk profile associated with its declining profitability and high leverage. A failure to restore margins could trigger a significant re-rating by the market.

- Restore Operating Margin: Implement rigorous cost controls and optimize pricing.

- De-risk International Exposure: Moderate the pace of China expansion and explore other high-growth markets.

- Reinvent the Loyalty Program: Shift focus from discounts to experiential rewards to reduce margin drag.

- Strengthen the Balance Sheet: Prioritize debt reduction to improve financial resilience.

The Mandate for a Strategic Pivot

The current trajectory is unsustainable. Management faces a critical inflection point where a new level of capital allocation discipline is required. Simply chasing store count and revenue growth is no longer a viable strategy. The focus must shift decisively towards operational excellence and rebuilding the profitability that once defined the brand.

| Company | Ticker | P/E Ratio (NTM) | EV/EBITDA (NTM) |

|---|---|---|---|

| Starbucks | SBUX | 22.5x | 14.1x |

| McDonald's | MCD | 21.0x | 16.5x |

| Restaurant Brands Int'l | QSR | 17.5x | 15.2x |

| Industry Average | - | 20.8x | 15.5x |

DIFF Insight: Starbucks trades at a premium P/E multiple compared to its peers and the industry average, despite its concerning margin outlook. This suggests the market is still pricing in a significant brand premium and a potential recovery. However, its EV/EBITDA multiple is more in line, indicating that on an enterprise value basis, the disconnect is less severe but still leaves little room for error.