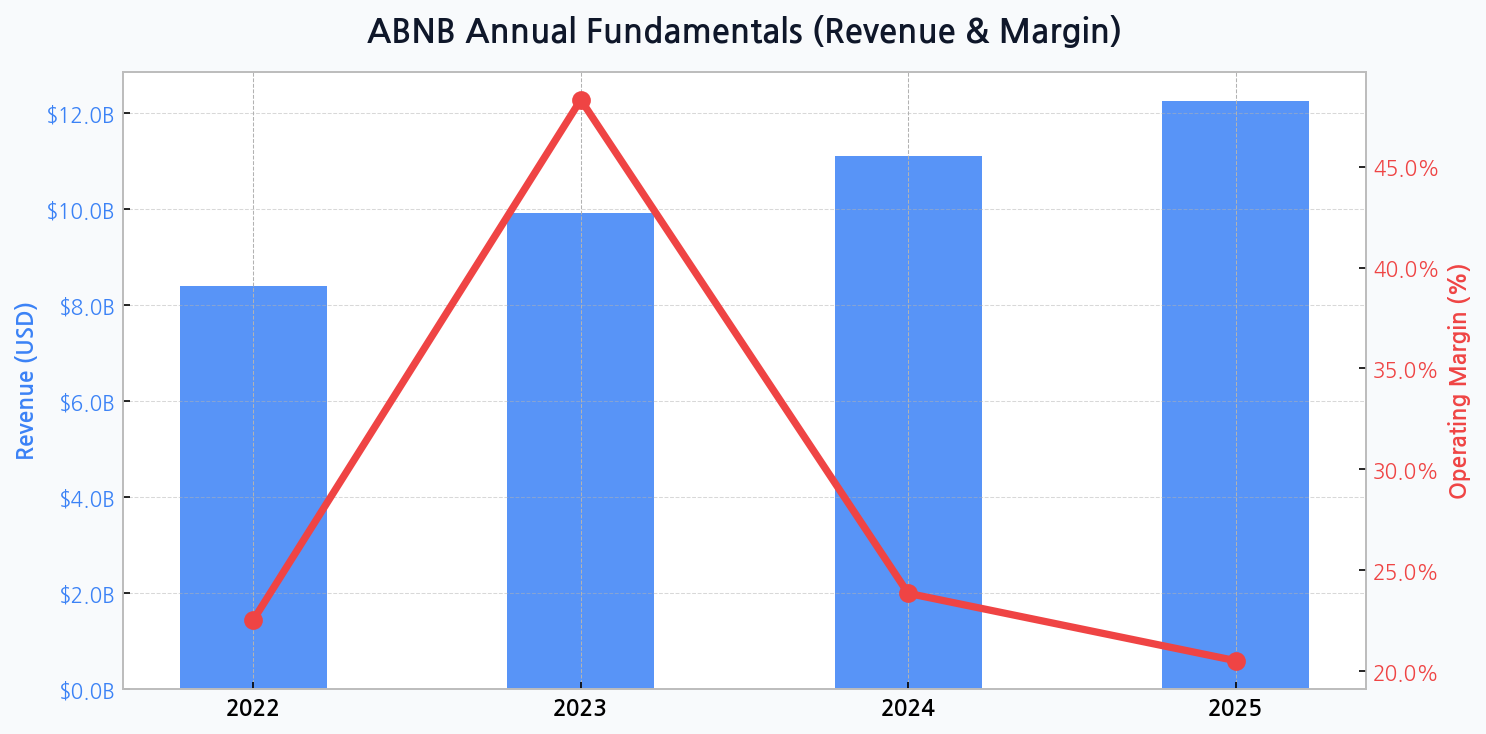

The Paradox of Growth and Shrinking Margins

Airbnb's top-line story is one of impressive expansion. The company's revenue is on a clear upward trajectory, growing from $8.4B in 2022 to an anticipated $12.2B by 2025. This signals strong global demand for its platform. Yet, this growth masks a troubling trend in profitability. Operating margins, after hitting a remarkable 48.3% in 2023, are forecasted to contract sharply to 23.9% in 2024 and further to 20.5% in 2025, indicating escalating cost pressures or significant reinvestment cycles.

Dissecting the Platform's Unassailable Network Effect

At the core of Airbnb's dominance is a powerful, self-reinforcing ecosystem. The vast and diverse inventory of hosts attracts a global user base of travelers, which in turn incentivizes more hosts to join the platform. This classic network effect advantage creates a formidable barrier to entry that is difficult and costly for competitors to replicate, cementing its market leadership in the alternative accommodation space.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for ABNB

[Chart] A visual representation of Airbnb's revenue growth juxtaposed with its volatile operating margin, highlighting the divergence between top-line expansion and profitability pressure from 2022 to 2025.

Competitive Landscape: A Battle for Traveler Trust

| Company | Primary Moat Source | Market Focus | Strategic Threat |

|---|---|---|---|

| Airbnb (ABNB) | Network Effect & Brand | Alternative Accommodations | Regulatory Hurdles |

| Booking Holdings (BKNG) | Scale & Aggregation | Hotels & Flights | Direct Booking Push |

| Expedia Group (EXPE) | Brand Portfolio (Vrbo) | Diversified Travel | Tech Integration Lag |

DIFF Insight: While Airbnb commands the alternative lodging space, its moat is not impenetrable. Booking.com has aggressively expanded its own vacation rental inventory, leveraging its massive user base. Expedia's Vrbo remains a direct competitor, particularly in vacation home markets. Airbnb's key differentiator remains its brand identity, which is synonymous with unique, local travel experiences, a qualitative edge that is harder to quantify but crucial for retaining user loyalty.

The Weight of Rising Assets and Financial Leverage

The company's balance sheet is expanding, with total assets projected to grow from $16.0B in 2022 to $22.2B in 2025. While this reflects business growth, the accompanying debt ratio presents a mixed picture. After a healthy dip to 60.5% in 2023, the debt ratio is expected to climb back to 63.1% by 2025. This rising leverage, coupled with declining margins, could constrain financial flexibility for future strategic M&A or aggressive buyback programs.

A Wall Street Perspective on Valuation

'The market is currently pricing Airbnb for perfection in growth, but the margin compression story is a significant headwind. Investors are questioning whether the 2023 profitability peak was an anomaly or if the new, lower margin profile represents the long-term reality of a maturing, more competitive market.'

Valuation Under the Microscope

| Metric | Airbnb (ABNB) | Booking (BKNG) | Industry Average |

|---|---|---|---|

| Price/Sales (TTM) | 6.2x | 4.8x | 4.5x |

| Forward P/E | 25.1x | 18.5x | 20.0x |

| PBR | 9.17x | 7.5x | 6.0x |

DIFF Insight: Airbnb consistently trades at a premium to its peers and the industry average, as evidenced by its higher P/S, Forward P/E, and PBR ratios. This premium is justified by its superior brand equity and growth potential. However, if margin erosion continues, the market may begin to question this valuation gap, creating potential for a stock price correction unless the company can demonstrate a clear path back to higher profitability.

Navigating a Minefield of Global Risks

| Risk Factor | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Global Regulatory Crackdowns | High | High | Proactive Govt. Relations |

| Macroeconomic Slowdown | Medium | High | Focus on Budget Travel Options |

| Intensified Competition | High | Medium | Product Innovation (Experiences) |

| Cybersecurity Breach | Low | High | Investment in Security Infrastructure |

DIFF Insight: The most significant and persistent threat to Airbnb's model are regulatory crackdowns in major tourist cities. Restrictions on short-term rentals can directly erode its supply, impacting revenue. While a global recession is a threat, Airbnb's diverse price points may offer some resilience. The company's strategic imperative is to work with cities to create sustainable regulatory frameworks rather than fighting them.

Strategic Imperatives for Future Growth

- Diversification Beyond Stays: Aggressively expanding the 'Experiences' segment to create new revenue streams and deepen user engagement with the platform.

- Operational Efficiency: Implementing stricter cost controls and leveraging technology to reverse the trend of margin compression and demonstrate sustainable profitability.

- Supply Quality and Host Relations: Investing in tools and support for hosts to ensure a consistent, high-quality guest experience, which is crucial for brand reputation.

- Navigating Geopolitical Tensions: Proactively managing its presence in politically sensitive regions to mitigate risks associated with international travel disruptions.