The Unseen Engine of Biotech Innovation

Thermo Fisher Scientific operates not as a discoverer of blockbuster drugs, but as the foundational enabler for those who do. It has built an expansive economic moat by supplying everything from analytical instruments to essential lab consumables, making it an indispensable partner in the global R&D ecosystem.

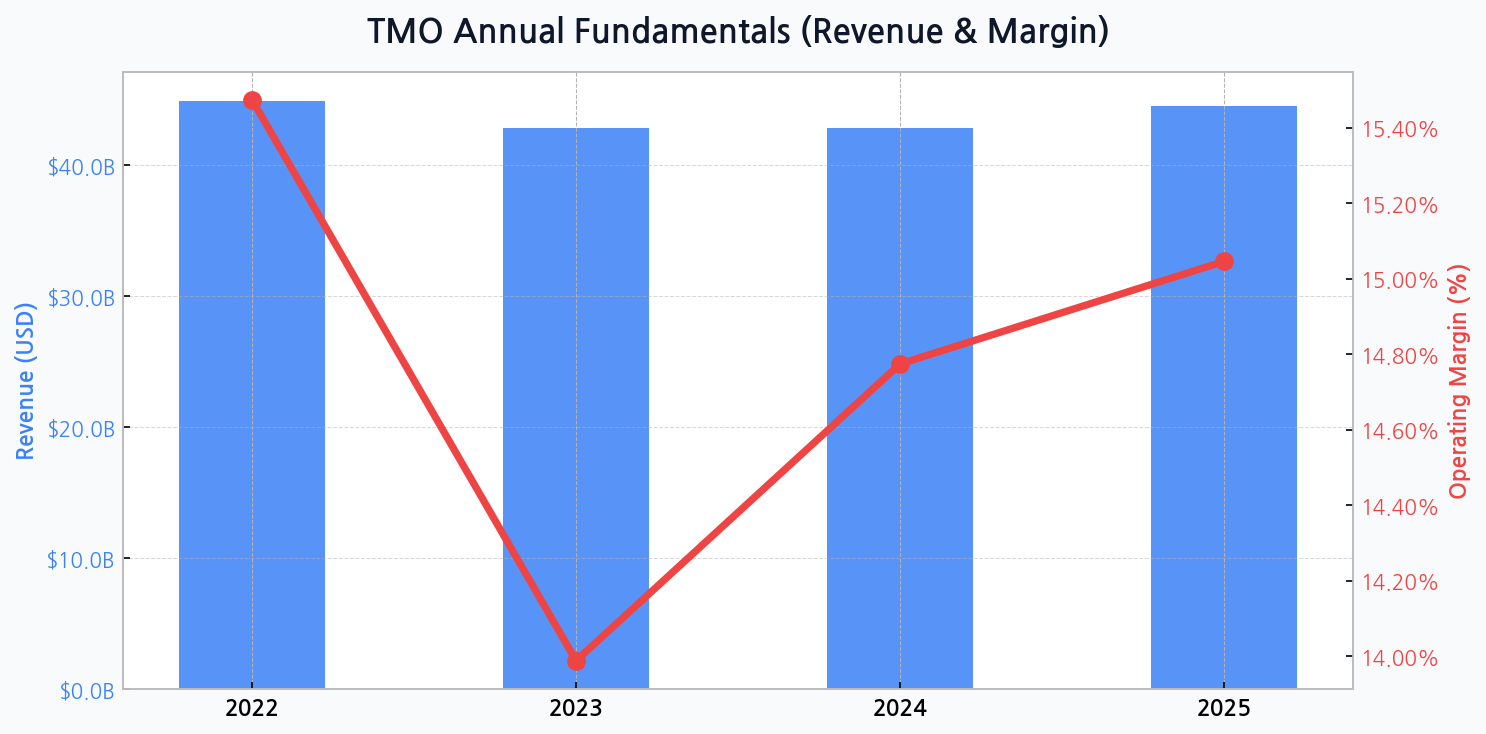

Navigating a Post-Pandemic Revenue Plateau

The company experienced a revenue peak of $44.9B in 2022, fueled by pandemic-related demand. This normalized to $42.9B in 2023, accompanied by a margin compression from 15.5% to 14.0%. Projections indicate a stabilization phase, with 2024 revenue holding steady at $42.9B before a modest recovery to $44.6B in 2025. This reflects a strategic pivot from pandemic-driven sales to core business growth.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for TMO

[Chart] Thermo Fisher's annual revenue shows a post-2022 normalization, while operating margin is projected to recover steadily after a dip in 2023.

Dissecting the Diversified Revenue Streams

The company's strength lies in its diversified portfolio, which insulates it from volatility in any single market segment. This structure ensures consistent demand from a wide range of customers, from academic labs to large pharmaceutical manufacturers, cementing its role as a foundational tool provider across the scientific landscape.

| Business Segment | Core Function | Estimated Contribution | Growth Outlook |

|---|---|---|---|

| Life Sciences Solutions | Genomic & Proteomic Research | ~ 30% | High |

| Analytical Instruments | Chemical Analysis & Measurement | ~ 25% | Moderate |

| Specialty Diagnostics | Clinical & Diagnostic Testing | ~ 20% | Stable |

| Lab Products & Biopharma Services | Consumables & CRO Services | ~ 25% | High |

DIFF Insight: The Lab Products & Biopharma Services segment, particularly Contract Research Organization (CRO) services, represents a key growth engine. As more biotech firms outsource R&D and manufacturing, this segment captures long-term, high-value contracts. The diversification across four major pillars provides exceptional resilience against sector-specific downturns.

The Balancing Act of Debt and Expansion

Thermo Fisher’s growth is heavily fueled by M&A, which necessitates careful balance sheet management. The company's debt ratio has shown prudent management, decreasing from 54.6% in 2022 to a projected 49.0% in 2024 before ticking up to 51.5% in 2025 alongside a significant asset base expansion to $110.3B. This strategy allows for aggressive expansion while keeping leverage within a manageable corridor.

"In a market where innovation cycles are shortening, consistent and reliable tools are paramount. Thermo Fisher's scale and breadth are not just a competitive advantage; they are a utility for the entire biotech sector."

The Strategic Acquisition Engine

A core pillar of the company's strategy is growth through acquisition, absorbing competitors and complementary technologies to broaden its moat. This strategic acquisition engine has been instrumental in consolidating its market leadership and expanding into high-growth service areas like clinical trials.

| Acquired Company | Year | Deal Value (Approx.) | Strategic Rationale |

|---|---|---|---|

| PPD, Inc. | 2021 | $17.4B | Expansion into CRO/clinical trial services |

| Patheon | 2017 | $7.2B | Strengthened contract development (CDMO) |

| FEI Company | 2016 | $4.2B | Dominance in electron microscopy |

| Life Technologies | 2014 | $13.6B | Leadership in genetic sequencing |

DIFF Insight: The acquisition of PPD was a game-changer, transforming Thermo Fisher from a pure-play equipment and consumables supplier into an integrated service provider. This move creates significant cross-selling synergies and locks in customers across the entire drug development lifecycle, from initial research to clinical trials and manufacturing.

Key Risks and Mitigating Factors

Despite its dominant position, Thermo Fisher is not without vulnerabilities. The primary risks involve the complexities of integrating large acquisitions and its exposure to cyclical R&D funding from governments and venture capital. A slowdown in biotech investment could directly impact demand for its products and services.

- Integration Risk: Ensuring seamless cultural and operational fusion post-M&A.

- Capital Spending Sensitivity: Performance is tied to the health of global R&D budgets.

- Supply Chain Complexity: Managing a vast and intricate global supply chain for specialized components.

- Competitive Pressures: Niche players can disrupt specific high-margin product lines.

Valuation in a Maturing Market

Thermo Fisher often trades at a premium to the broader market, justified by its strong competitive positioning and consistent cash flow. However, its valuation must be continually assessed against its growth prospects and the performance of key competitors who also vie for market share in this lucrative space.

| Company | Ticker | P/E Ratio (FWD) | P/S Ratio (TTM) |

|---|---|---|---|

| Thermo Fisher Scientific | TMO | ~ 25x | ~ 4.2x |

| Danaher Corp. | DHR | ~ 28x | ~ 5.5x |

| Agilent Technologies | A | ~ 23x | ~ 5.0x |

DIFF Insight: While its P/E ratio is comparable to peers, Thermo Fisher's Price-to-Sales (P/S) ratio is slightly lower than key rivals like Danaher. This could suggest that the market is either anticipating slower top-line growth or that the stock offers relatively better value based on its revenue-generating capabilities. The successful integration of its service-based acquisitions will be key to justifying its premium valuation.