The Legacy Giant's Reawakening

International Business Machines is navigating a monumental transformation. Shedding legacy businesses, it has sharpened its focus on the high-growth arenas of hybrid cloud and artificial intelligence. This is not merely a product refresh but a fundamental rewiring of its corporate DNA, aimed at regaining relevance in a market dominated by hyperscalers.

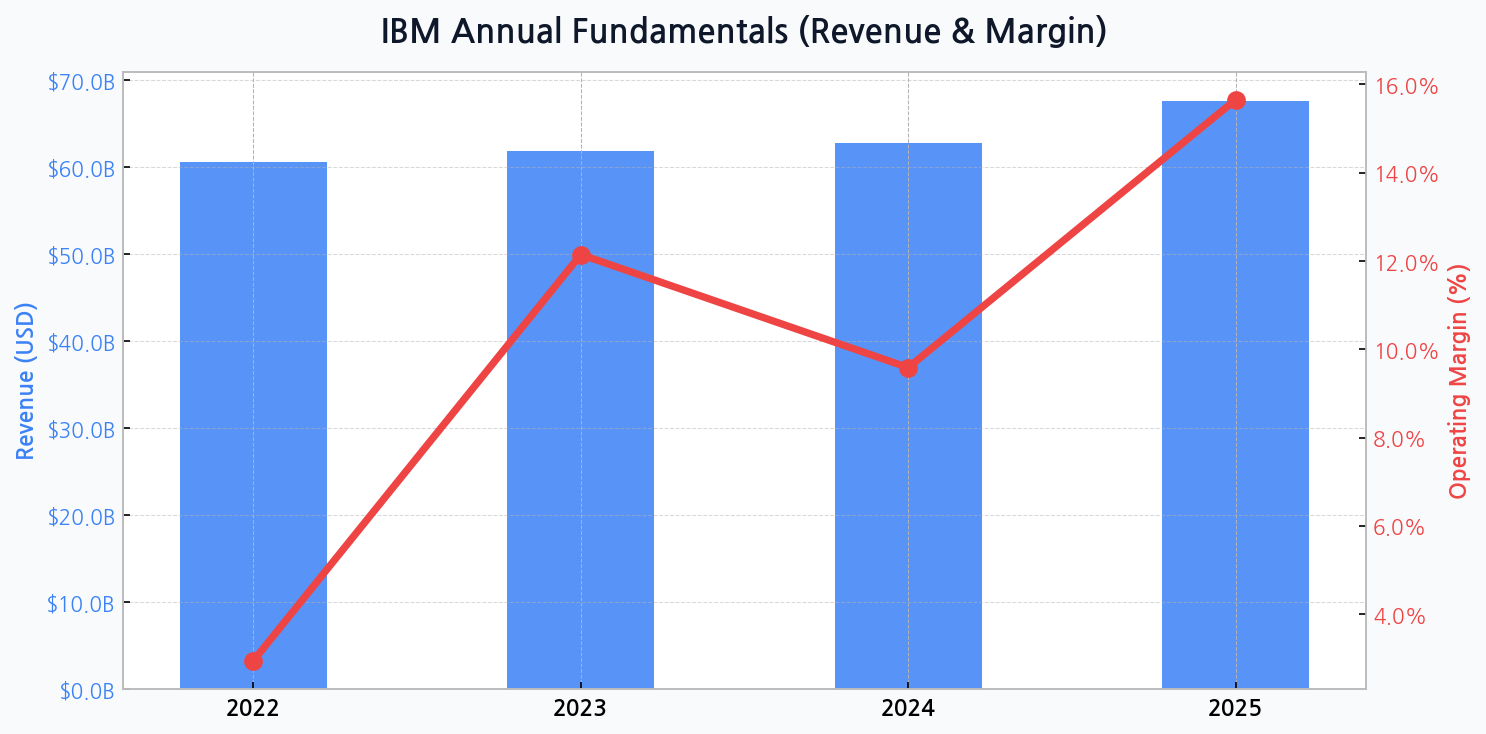

A Tale of Growth and Volatility

The company's financial trajectory reflects this transition. Revenue is on a steady upward path, growing from $60.5 billion in 2022 to a forecasted $67.5 billion by 2025. However, the operating margin tells a more complex story of investment and restructuring. After a dramatic recovery from 2.9% in 2022 to 12.1% in 2023, it dipped to 9.6% in 2024 before a projected surge to 15.7% in 2025, indicating that the costs of its strategic pivot are substantial but may soon yield significant returns.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for IBM

Watsonx vs. The Hyperscalers

IBM's primary weapon in the AI war is Watsonx, a platform designed for enterprise-specific needs like data governance and model explainability. Unlike consumer-facing AI, IBM is targeting regulated industries where trust and compliance are paramount. This creates a defensible niche against the broader offerings of tech giants.

| Platform | Core Strength | Target Market | Key Differentiator |

|---|---|---|---|

| IBM Watsonx | Governance & Trust | Regulated Industries | Hybrid Cloud Integration |

| Microsoft Azure AI | Developer Ecosystem | Broad Enterprise | OpenAI Partnership |

| Google Cloud AI | Data & Analytics | Data-Intensive Firms | Advanced Model Research |

| AWS AI/ML | Scalability & Services | Startups to Enterprise | Breadth of Tooling |

DIFF Insight: While competitors focus on scale and developer access, IBM is carving out a high-value niche in enterprise governance. Its success hinges on convincing large corporations that Watsonx's specialized, secure approach to AI is superior for mission-critical applications, justifying a potential premium over the more generalized tools from hyperscalers. This is a battle for the most lucrative, not necessarily the largest, segment of the AI market.

'The combination of Red Hat OpenShift and IBM's AI and data platform, Watsonx, creates a powerful foundation for building and scaling AI workloads across any environment. This is the core of our value proposition.'

The Persistent Drag of Debt

A critical risk factor is IBM's balance sheet. While total assets are projected to grow from $127.2 billion to $151.9 billion between 2022 and 2025, the debt ratio remains elevated. It peaked at 83.3% in 2023 and is only slowly receding to a projected 78.4% by 2025. This high leverage could constrain its ability to fund future acquisitions or weather economic downturns, placing immense pressure on its hybrid cloud architecture to generate consistent cash flow.

Strategic Capital Allocation

IBM's management has focused on shareholder returns alongside its transformation. The company has a long history of paying dividends, a commitment it has maintained even during periods of heavy investment. This signals confidence in its long-term cash-generating ability.

| Year | Dividend Per Share | Share Buybacks | Total Return |

|---|---|---|---|

| 2022 | $6.61 | $0.4B | $6.3B |

| 2023 | $6.64 | $0.5B | $6.5B |

| 2024 (Est.) | $6.68 | $0.6B | $6.7B |

DIFF Insight: The modest but consistent increase in dividends and buybacks demonstrates a disciplined approach to capital allocation. Unlike tech peers that hoard cash or pursue mega-mergers, IBM is balancing its growth investments with direct returns to shareholders. This strategy appeals to a more conservative, income-focused investor base, providing a floor for the stock price during periods of market volatility.

The Path Forward and Potential Pitfalls

IBM's success is not guaranteed. The core challenges lie in execution and market perception. It must continue to prove that its integrated solutions offer a superior value proposition for enterprise-grade AI and hybrid cloud management.

- Competitive Intensity: The cloud and AI markets are fiercely competitive, with well-capitalized rivals innovating at a rapid pace.

- Integration Risk: Successfully weaving acquisitions like Red Hat into its core consulting and software businesses is crucial for realizing synergies.

- Macroeconomic Headwinds: A global economic slowdown could cause enterprises to delay large-scale IT transformation projects, impacting IBM's growth trajectory.

- Cultural Transformation: Shifting a century-old company's culture towards the agility required in the modern tech landscape is an ongoing battle.