The Consumption Conundrum: Fueling Growth at What Cost?

Snowflake's consumption-based revenue model is a double-edged sword. It brilliantly lowers the barrier to entry for enterprises, fostering rapid adoption and breaking down data silos. Yet, this same model introduces revenue volatility and complicates the journey toward consistent profitability.

Breaking Down Data Silos: The Multi-Cloud Moat

The company's core value proposition is its ability to serve as a truly platform-agnostic layer across AWS, Azure, and GCP. This strategic positioning creates a powerful, defensible moat that competitors tied to a single cloud ecosystem cannot easily replicate.

- Centralized Data Access: Enables a single source of truth for analytics, regardless of where data is stored.

- Seamless Data Sharing: Facilitates secure and governed data sharing between organizations, creating a network effect.

- Decoupled Storage & Compute: Allows customers to scale resources independently, optimizing cost and performance.

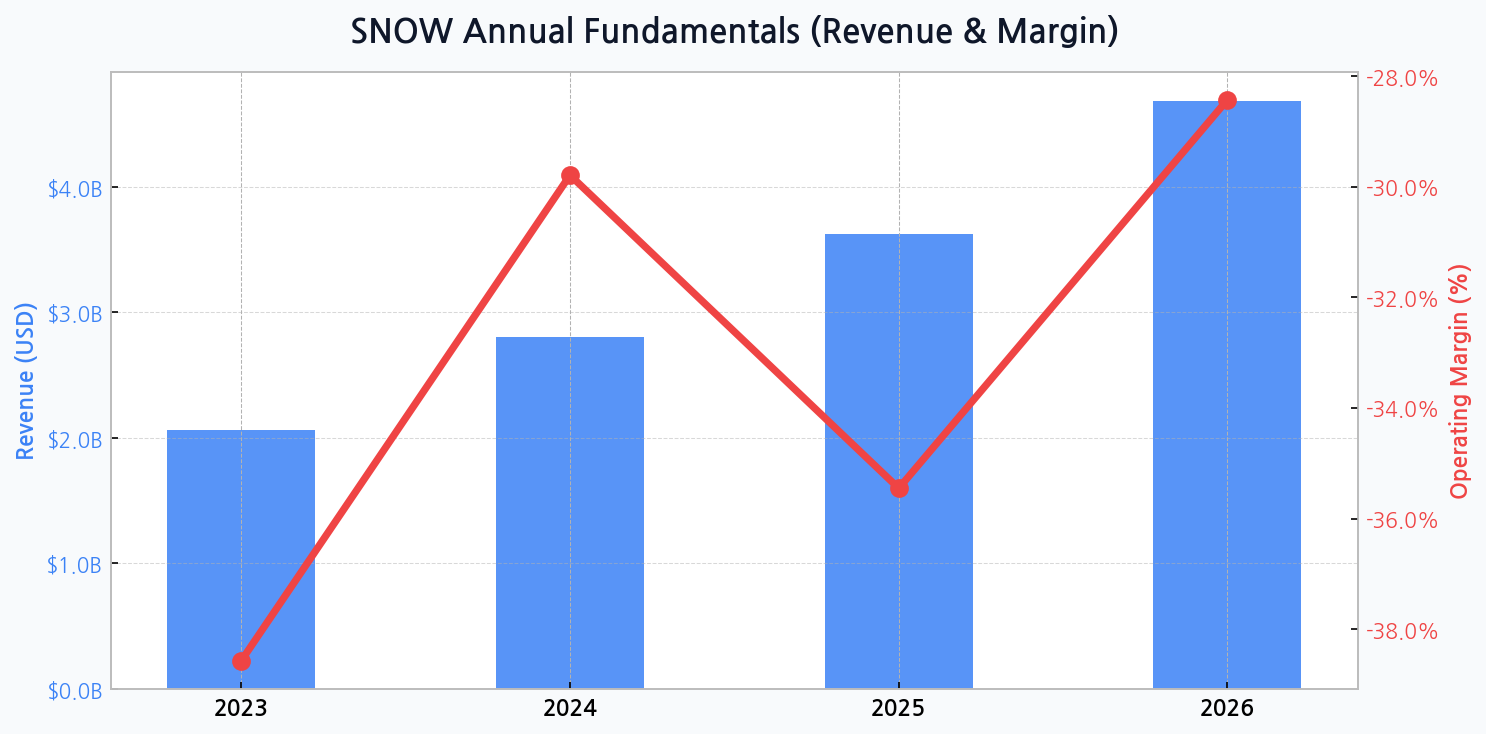

The Profitability Puzzle: A Persistent Margin Deficit

While revenue is on an impressive trajectory, projected to more than double from $2.1B in 2023 to $4.7B by 2026, operating margins remain deeply negative. After a brief improvement to -29.8% in 2024, the margin is expected to worsen again in 2025 to -35.5%, indicating a significant cash burn required to sustain growth.

[Chart] Total Assets (Bar) & Debt Ratio (Line) for SNOW

[Chart] Snowflake's Annual Revenue shows strong upward momentum, while its Operating Margin remains volatile and consistently in negative territory, highlighting the ongoing challenge of balancing growth with profitability.

Navigating the Competitive Gauntlet

The data warehousing space is fiercely competitive. Snowflake differentiates itself through its multi-cloud architecture and ease of use, but faces intense pressure from both established cloud giants and specialized rivals like Databricks, which is aggressively pushing its 'Lakehouse' paradigm.

| Feature | Snowflake | Databricks | AWS Redshift |

|---|---|---|---|

| Architecture | Cloud Data Platform | Data Lakehouse | Cloud Data Warehouse |

| Cloud Support | Multi-Cloud | Multi-Cloud | AWS Only |

| Core Focus | SQL, BI, Data Sharing | AI/ML, Data Engineering | BI & Analytics |

| Primary User | Data Analysts | Data Scientists | AWS Developers |

DIFF Insight: Snowflake's primary advantage is its simplicity and multi-cloud neutrality, appealing directly to business analysts and executives aiming to avoid vendor lock-in. However, Databricks poses a formidable threat by capturing the more technical AI/ML workload market, potentially boxing Snowflake into the traditional BI space over time. The key battle is for dominance over the entire enterprise data lifecycle.

A Balance Sheet Under Pressure

The financial health of the company presents a growing concern. The aggressive pursuit of market share has led to a dramatic increase in leverage.

The company's debt ratio is projected to surge from a manageable 29.2% in 2023 to a precarious 78.9% by 2026. This escalating reliance on debt to fuel operations is unsustainable without a clear and imminent path to profitability.

Valuation Under the Microscope

Despite its financial headwinds, Snowflake continues to trade at a premium valuation. This reflects strong investor confidence in its growth narrative and market leadership. However, this premium is fragile and highly sensitive to any deceleration in growth or failure to improve margins, creating significant downside risk for investors.

Critical Risk Matrix

Several external and internal factors could derail Snowflake's trajectory. Understanding these risks is crucial for assessing the company's long-term viability.

| Risk Category | Threat Level | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Margin Compression | High | Delayed Profitability | Optimize R&D, pricing power |

| Competitive Pressure | High | Slowing Growth | Product innovation, ecosystem |

| Macro Slowdown | Medium | Reduced Consumption | Focus on mission-critical workloads |

| Debt Overhang | Medium | Financial Instability | Improve cash flow, cost controls |

DIFF Insight: The most immediate threat is the combination of intense competition and margin pressure. If cloud providers or Databricks offer more cost-effective solutions for core workloads, Snowflake's consumption revenue could falter, making its debt burden increasingly difficult to service. The company's future depends on its ability to prove its total cost of ownership is superior.

The Path Forward: Strategic Imperatives

To justify its valuation and secure its future, management must focus on several key areas. The narrative must shift from growth-at-all-costs to demonstrating a credible path to profitability.

- Operational Efficiency: Streamline sales and marketing expenditures, which are a primary driver of the negative margins.

- Product Stickiness: Deepen the ecosystem with new features like Snowpark and the Data Marketplace to increase customer dependency.

- Enterprise Penetration: Secure larger, more stable contracts with enterprise clients to create a more predictable revenue base.